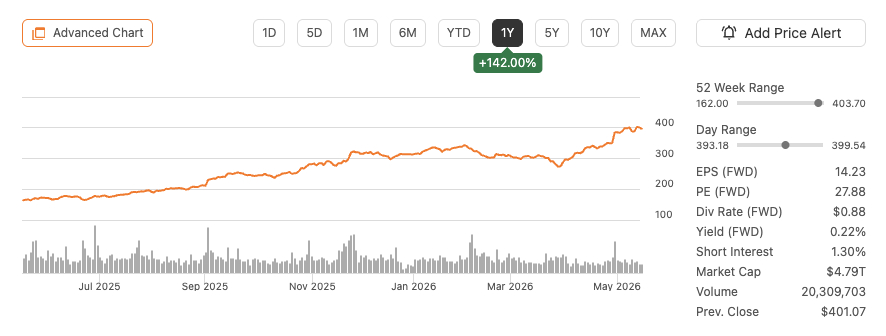

Google () stock is up +142.00% over the last year (as of 05/17/2026).

The reason isn’t that investors just happened to discover Google Search over the last year.

Investors always knew about Google Search—just like they always knew about YouTube, Android, Chrome, Gmail, Google Maps, Google Cloud, Google Ads, and the astonishing amount of data powering this business empire.

What changed in the last year is how the market priced the value of control. Ask a hundred people on the street what Google’s business is and you’ll probably get half a dozen different answers.

While all the answers you’ll get may have some truth to them, they’ll all miss Google’s fundamental business model. Google’s business is controlling the default behavior of the internet. You’ll often need to pass through a Google-owned gate—whether you want to buy something, drive somewhere, watch a video, send an email, or just browse the web. Search captures intent. YouTube captures attention. Android captures mobile distribution. Chrome captures browser behavior—and Gemini?

It’s just another avenue to control the landscape of the World Wide Web.

The Market Is Not Just Paying For Software Margins

You’ll often hear that premium valuations are a trait of software companies because these software companies have scalable business models that generate high margins while accruing low incremental costs.

However, if valuations were only about scalability, margins, and costs, neither Costco ($) nor Walmart ($) would command valuations at 52x and 47x earnings, respectively.

Unlike Google with its 38% net margin, both Costco and Walmart’s net margins hover at around the 3% mark. That’s because investors don’t just reward high margins and growth figures, but, in the case of Costco and Walmart, also consider other metrics that measure a business’ control over its industry and sector and the difficulty any company might face in recreating this level of control. The common denominator isn’t tech. It’s control.

Costco controls a membership relationship and a consumer habit built around trust, while Walmart controls physical distribution, supplier relationships, and logistics at scale.

They might operate in an entirely different sector, but Costco and Walmart are really no different from Google.

I’m no huge fan of value investing. A low valuation is never a bargain.

It’s the market doing what it does best and punishing companies (both good and bad) for their lack of control.

Airlines are a good example to take. These last few months have seen airline stocks get hammered as investors realize how little control airlines have. Airline stocks are a bad investment because their business (regardless of how great this business is) is at the mercy of fuel costs, labor negotiations, airport constraints, and price competition. It’s really no surprise that an airline like Delta () has never seen its stock rise above a P/E of ~12 in the last 15 years.

The stock market doesn’t reward this kind of business and investors are unlikely to see their investments provide the great returns they anticipate. Very few stocks are cheap because investors are wrong. Most low valuations are deserved.

Control May Be The Real Investing Factor

What if “control” was the real investing factor investors should look for? What if “control” affords certain companies an insurmountable advantage that makes them nearly impossible to beat?

What if it’s not about which LLM is smarter, but about which provider has the most control over its industry? I say this because a lot of the analysts comparing LLMs don’t seem to realize that Gemini doesn’t need to be the best LLM to triumph over OpenAI’s ChatGPT and Anthropic’s Claude… because Google controls distribution. It can place Gemini inside any one of its one hundred products in front of billions of existing users. It can fund AI infrastructure from the enormous cash flow its other businesses generate and, when it comes to running these models, Google doesn’t need to use NVIDIA chips. It can use its own custom TPU chips. In fact, it’s these custom TPUs that have made Google the definitive leader in AI compute.

All in all, this creates a situation where, unlike the leading providers of frontier LLMs, Google doesn’t need to grovel for compute power. This is what monopoly power and industry control looks like.

Who needs the best product when you’ve got the free cash flow, distribution, infrastructure, and default placement to ensure your product’s success becomes an unavoidable reality?

Why Invest In —When You Can Invest In SPY’s Best Companies Through MPLY ETF?

This is precisely what makes the Strategy Shares Monopoly ETF () such a compelling investment. Instead of investing in $VOO, $IVV, or $SPY (all indiscriminate index funds), MPLY’s thesis centers around investing in companies with monopolistic attributes—the companies that control their industries rather than the other way round. The advantages? Well, you get to skip on duds like airline stocks, while focusing on companies with tangible and durable moats in all industries.

MPLY ETF, for example, is comprised of 9.77% GOOG, 2.81% WMT, and 1.25% COST—alongside a diversified portfolio of another 96 holdings.

However, rather than focus exclusively on companies with monopolistic attributes, MPLY also screens its holdings for attractive financial metrics.

This is more important than most people realize.

There are several quasi-monopoly ETFs that occupy the same niche as MPLY. Neither VanEck’s nor Tema’s screens on the basis of attractive financials.

TOLL is held back with its exposure to utility stocks and other government-granted regulatory monopolies with mediocre balance sheets and limited growth potential.

MOAT is, arguably, worse, as it tries (and fails) to combine a wide moat strategy with a value-driven approach, which sets it up to invest in companies with declining monopoly power. The returns gap proves the flaws in these strategies. MOAT managed 1-year total returns of just +8.83% (as of 05/17/2026), which is pretty ridiculous when you realize that the S&P 500 pulled in +24.23% over the same period. TOLL did slightly better with 1-year returns of +11.80%. On the other hand, MPLY ETF comfortably beat the S&P 500 with 1-year total returns of +29.95%, proving that MPLY offers investors a cleaner, more focused, and more financially disciplined way to capture the companies that actually control the modern economy.

Final Thoughts

In today’s market, the strongest monopolies often do not look cheap. They look expensive because the market understands what they are. Waiting for them to trade like average companies may simply mean never owning them at all.

That’s what makes MPLY such a compelling prospect.

The fund is attacking a very real problem.

The market’s biggest winners are often the companies that control something other companies need, something customers cannot easily leave, or something competitors cannot cheaply replicate. That is the MPLY thesis. The companies that create the most enduring shareholder value are often not the ones that fight hardest in competitive markets.

They are the ones that gradually gain control over the market structure itself. And it is why many cheap stocks remain cheap. The market may simply understand that they compete in industries where even the best operators have limited control.

The best companies do not compete.

They control.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.