In a few days, the most anticipated IPO in history begins trading. Even people who have never bought a stock are talking about it. Before you join them, it is worth slowing down: what does actually do, and does it make money? What are you really paying for at a $1.77 trillion valuation? And what are the risks of buying in?

How SpaceX Actually Makes Money

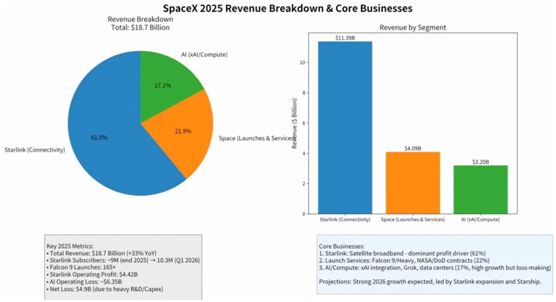

SpaceX is best understood as three distinct businesses operating at very different stages of maturity.

- Starlink is the commercial backbone. Its satellite constellation delivers broadband to locations conventional networks cannot reach economically, from maritime and aviation customers to remote regions without ground infrastructure.

Because revenue is subscription-based, it is recurring and high-margin, and it accounts for the majority of the company’s top line.

Strategically, the same technology underpins SpaceX’s longer-term ambitions: a Mars settlement would require an off-world communications layer, and a Starlink-style constellation is the logical first step.

- Launch services are the original and most visible business. Putting satellites and crew into orbit is what established SpaceX’s reputation and its lead in reusable, recoverable rockets.

- AI is the newest and most speculative addition. Through its ties to xAI and Grok, SpaceX is now linked to the broader AI cycle. It carries the largest long-term optionality and, at present, the steepest losses.

The composition matters more than the growth rate. Revenue rose 33% to $18.7 billion, but the company still posted a net loss of roughly $4.9 billion in 2025.

Launch is loss-making, AI is consuming cash quickly, and Starlink is the sole profitable segment. Even Starlink’s $4.42 billion profit is modest against a valuation measured in the trillions.

The picture, then, is of a fast-growing business that is not yet profitable on a consolidated basis, priced as though the future has already been delivered. Whether that price is justified is the question the rest of this brief examines.

Competitive Strengths

- Starlink dominance. Close to a monopoly in satellite internet, with high-margin recurring revenue and a strong growth trend.

- Launch leadership. The only independent private company with this level of U.S. government backing, well ahead of peers on reusable, recoverable rockets.

- AI and compute. xAI and Grok ride a huge market, and their eventual share could set the ceiling on SpaceX’s earnings.

- Government contracts. Extensive deals including launches, with possible defense work such as Starshield.

- Massive market. A space economy worth nearly $1.77 trillion by 2040, plus Mars transportation, where no other company is close.

Key Risks

- High cash burn. Annual burn topped $5 billion in 2025, which is the real reason for the IPO: the company needs capital.

- Valuation concerns. The most important risk is covered below.

- Technical execution risk. Launches, landings, and Mars deployment all carry deep uncertainty, and a single failure could move the stock fast.

- Key-person dependency. The stock revolves around Musk. rose over 300x since its IPO, but through repeated 70% to 90% drawdowns.

- Regulatory and geopolitical risk. Heavy government ties can cut both ways, especially outside the U.S.

- Competition. Little rivalry in launches and Starlink, but intense competition in AI, the most cash-hungry segment.

Is It Really Worth $1.77 Trillion?

At $135 per share, the valuation on day one is about $1.77 trillion, already above Tesla. However, SpaceX is still burning cash, while Tesla is now a steady cash machine that earns money every year.

One simple way to read this: price-to-revenue tells you how many dollars you pay for each dollar of sales.

SpaceX asks for 94, against Nvidia’s 36 and Tesla’s 12, while the average S&P 500 company sits near 2.7. Even Tesla in its unprofitable early years never reached a 94x multiple. On current earning power, that is a number worth weighing carefully.

Who Actually Controls SpaceX?

Musk holds about 42% of the equity, but through a dual-class structure (Class B shares carry ten votes each) he controls roughly 80%+ of the voting power, in practice close to total control.

For believers in Musk, that means fast, aligned decisions. But concentrating control in one person, given his unconventional style and political involvement, adds real risk to both SpaceX and Tesla.

IPO Structure: Tight Float, Heavy Retail

- $135 per share, around 555.6 million Class A shares, roughly $75 billion raised.

- Only about 4% of shares trade publicly at first, with 96% locked up. When very few shares are available, prices swing harder in both directions.

- Retail allocation runs as high as 30%, well above the usual sub-10%, pointing to heavy retail participation that tends to amplify moves.

How It Might Behave After Listing

Comparable high-profile IPOs tend to share one feature: high volatility early on. A tight float plus heavy retail makes a big opening surge followed by a deeper pullback a familiar pattern.

And when people who never invest start calling it “free money,” sentiment is usually running hot, which is exactly when it pays to stay clear-headed.

So whether you join in or watch from the sidelines, remember that the swings may be large and managing your mindset matters more than chasing the crowd.

So how long will the hype last? Let us follow and look at this IPO of the century together.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out above is for informational purposes only.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.