The issue is that the AI story has become so crowded, so capital-hungry, and so aggressively priced that even believers are starting to ask if the market has already eaten too much of tomorrow’s meal.

Takeaways

• The failed bounce was the tell. This was not just another ugly tech session. It was the market admitting that AI leadership has become crowded, expensive, and too central to index psychology.

• Equity supply is the next liquidity test. SpaceX, OpenAI, Anthropic, and the broader AI capital-raising machine may validate the innovation cycle, but they also force investors to decide what must be sold to fund the next dream.

• Korea is the warning flare. When leveraged AI ETFs, margin debt, upside volatility panic, and household speculation all converge in one market, traders should pay attention because leverage rarely rings a bell before it starts working in reverse.

When The Chips Are Down

The market came into Tuesday trying to sell investors the comforting ”Turnaround Tuesday” idea that Friday’s AI fracture was just another pothole on the road higher. By the close, that story had lost its bid. Monday’s dead cat bounce had done what dead cat bounces always do. It gave the bulls just enough daylight to reload confidence before the floorboards started creaking again. There was no clean macro grenade, no obvious single headline, and no neat level break that could explain the move. That was the real tell. When a market starts falling without a catalyst, positioning itself becomes the catalyst.

So, to answer yesterday’s question, which I assigned a 65% probability of yes, it was a dead cat with a Bloomberg Terminal.

Stocks had the kind of session that leaves traders staring at their screens longer than usual. The open looked constructive, the middle of the day turned into a trapdoor, and the final hour brought enough dip buying to drag the tape off the lows but not enough to fix the damage. The fell about 1%, the slipped 0.26%, while the rose 86 points, or 0.17%, to close at 50,872. That split was the entire message in one line. The market was not collapsing in a straight line. It was rotating, coughing, and trying to reprice leadership without admitting the old leadership had started to wobble.

Fresh Iran jitters added another layer after a US Apache helicopter was shot down, with the pilots safe, while investors digested strong trade figures from several key economies and turned toward Wednesday’s US inflation data. But the bigger macro problem is that good news is no longer simple good news. Friday brought strong jobs data and stocks fell. Monday brought bland macro and stocks bounced. Tuesday brought better housing data and stocks fell again. in May rose 3.2% from April, far above the 0.7% consensus estimate, suggesting lower mortgage rates are finally breathing some life back into a sluggish housing market. Yet in this tape, better growth does not arrive with a champagne glass. It arrives with a Fed question attached.

That is the market’s growth and rates tango. If the economy keeps holding up, move further away, the Fed stays tighter for longer, and a market trading above 20 times earnings has to justify its altitude with less oxygen. AI gave this bull market its engine, its soundtrack, and its swagger. But when one theme carries too much of the index, every stumble starts to feel structural. The market can love tech leadership and still need breadth to survive. When one pillar is holding up the whole roof, even a small crack sounds like thunder.

And this is where Wednesday’s becomes the real macro fuse. If inflation comes in hotter than expected, the market will not just be repricing the Fed path. It will also have to reconsider whether lower oil prices are enough to offset sticky services inflation, firm wages, and a still-resilient economy. A soft CPI would give equities a breathing lane and allow the bond market to lean into the idea that oil’s retreat matters. But a hot CPI would slam the door on that relief trade, harden the higher-for-longer narrative, and turn every crowded AI long into a duration asset with less oxygen.

The options market is already treating CPI as the main event, with the IPO adding a second liquidity wrinkle in the background.

Yet again, the semiconductor complex was where the thunder was loudest. Chipmakers had powered the rebound from US-Iran war-driven lows and were on track for their strongest year since 1999, exactly the kind of performance that leaves little room for doubt once valuations start to matter again. , , and were hit hard, helping push the down 1.9%. It could have been a real faceplant if not for a late-day recovery.

The Nasdaq 100 lost 1.1%. “But the AI story is not dead they say !!” That is too easy, too lazy and poor analysis. The issue is that the AI story has become so crowded, so capital-hungry, and so aggressively priced that even believers are starting to ask whether the market has already eaten too much of tomorrow’s meal.

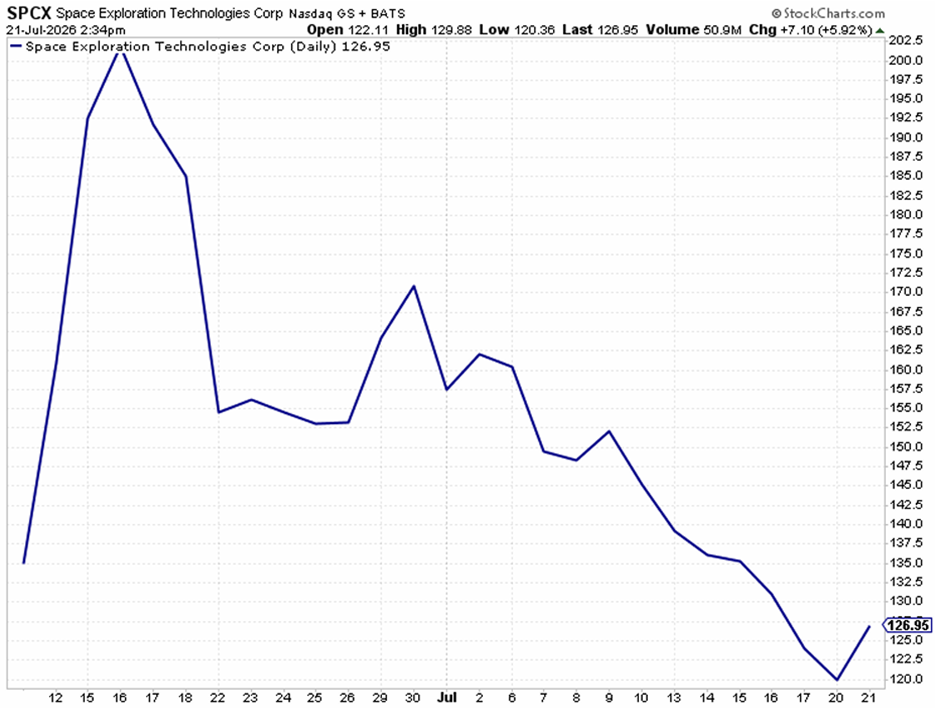

That question becomes more uncomfortable with the IPO machine warming up. SpaceX is the marquee event, and Morningstar’s valuation work has thrown a wrench into the party lights, putting fair value at $63 per share, a 53% discount to the expected IPO offer price. In its moonshot scenario, SpaceX is worth $1.97 trillion, or $154 per share, which would be 14% above the IPO price, but Morningstar assigns only a 7% probability to that outcome. At the same time, demand is reportedly nearly four times oversubscribed ahead of Friday’s debut. That is fascinating, no doubt. But it also drags the oldest market question back onto the desk. Where does the money come from?

Some of it comes from cash. Some comes from retail appetite. But for institutions, a deal of that size can mean trimming the very winners that carried the year. That is how a bull market begins feeding on its own muscle. A megacap IPO can be adrenaline for a mature rally, but adrenaline is not nutrition. At first, these deals confirm innovation, confidence, and depth of demand. Later, they become a test of whether the market can digest the feast without choking. True euphoria is not one giant deal. True euphoria is when every banker in town is rushing half-built stories to market, and every investor believes flipping the next wonder child is a retirement plan. We may not be there yet, but the road signs are starting to look familiar.

OpenAI filing for its IPO late Monday only adds to that capital gravity. Alongside SpaceX and Anthropic, the AI issuance pipeline is becoming a second market inside the market. And equity supply is never just a funding detail. It is a valuation signal. When companies rush to sell stock into rich multiples, they are ringing the dinner bell for capital. The problem for existing holders is that the buffet gets crowded, and the check always lands somewhere.

This is why the bear market signposts deserve respect, even if they are not yet screaming. A surge in equity issuance, tighter monetary policy, and the possibility of a growth slowdown are not fatal on their own. But together, they form the kind of triangle traders do not ignore. Equity supply drains liquidity from existing winners. Higher rates make long duration growth harder to justify. Slower growth leaves less room for earnings to catch up with valuation. That is not a crash script. It is a fragility script. And in a market this crowded, fragility can be enough.

The dispersion signal within the technology setor is flashing particularly brightly. The spread between the best- and worst-performing quintiles in the sector now exceeds 120 percentage points, the widest since February 2000, just before the Dot Com peak in March of that year.

The comparison is not perfect, and it should not be treated like a cheap ghost story. Back then, even the bottom quintile was up about 10%, which showed a broad market intoxication. Today, the bottom quintile is down roughly 8%, which means the exuberance is narrower and more surgical. But narrow excess can still break things, especially when it sits inside the most important sector in the index.

The fundamentals are still much healthier than the old bubble, but the direction of travel has deteriorated. Cash flow conversion has flatlined. Investment-grade and equity supply have increased. Buybacks as a share of market cap have slowed. Hyperscaler capex as a share of operating cash flow is expected to reach nearly 100% by year-end, up from 40% in 2023. That is the AI machine turning from asset-light dream into capital-intensive furnace. The market still loves the story, but the story now needs a lot more fuel.

Oil should have offered relief, but it did not deliver much. Crude traded lower after President Donald Trump sounded more upbeat about ending the Iran conflict, saying negotiations were in the final throes of what he called a very good deal. dropped below $90, and Treasury yields eased with the hovering around 4.54%. Then around 12:20 New York time, President Donald Trump warned that the US must respond to Iran’s attack on the Apache helicopter, and crude jerked higher. Around 14:00, Iran’s Aragchi warned that foreign forces near Iran were at risk, extending the rebound.

By the close, front-month WTI still finished down more than 3%, holding below $90 and testing levels near the early May lows. But the more important point is that lower oil did not produce a clean rally in stocks or bonds. When crude falls, yields ease, the dollar behaves, and equities still cannot breathe properly, mission control has a problem. It tells you the equity wobble is not just oil, not just geopolitics, and not just rates. It is positioning, valuation, supply, and the market’s growing discomfort with how much money has been squeezed into one narrow AI corridor.

For crude, this still feels less like a clean peace premium and more like a market sitting in the eye of a sandstorm, pretending visibility has improved because the wind has paused for five minutes. The physical barrel has stayed heavier than the headline tape would suggest, which tells me the market is still finding supply paths, demand in Asia is not exactly screaming for barrels, and reserve releases may be doing just enough to keep the machinery from seizing up. But that is a very different thing from saying the risk has cleared.

The uneasy part is that both Tehran and Washington seem to believe time is their friend. Each side thinks the other has more to lose, and that is usually how stalemates stretch longer than traders want to admit. So while paper crude keeps fading the geopolitical premium, the physical market is quietly being asked to perform a magic trick: keep barrels moving across a restricted regional chessboard without freight, insurance, inventories, or prompt availability, or prompt availability, eventually calling foul. Maybe the market can keep threading that needle for a little longer, but I would not build a long-term oil view on the assumption that gravity has been repealed.

The key risk is not today’s headline. It is the slow tightening underneath the surface. If cargo flows become patchier, if freight costs start to lift, or if inventories stop cushioning the tape, crude can quickly move from background noise back to front page risk. For now, oil is trading as if the geopolitical fuse is wet. My concern is that the fuse may simply be longer than usual.

Bonds were the calmest room in the building, which almost made them more interesting. Treasury yields drifted modestly lower through most of the day, led slightly by the short end. But under the surface, the funding plumbing deserves a look. The US Treasury is issuing more than $500 billion of T bills per week on average. For now, that is not an immediate problem because the market for cash like instruments is enormous. T bills are the grease in the overnight funding machine, the collateral brickwork behind liquidity management, and a core holding for money market portfolios. With money market fund balances near $8 trillion and the Fed also buying bills for liquidity management, there is still capacity to absorb the supply.

But even the deepest pools have edges. The Trump administration is leaning more heavily on the short end because persistent deficits and elevated inflation have lifted the term premium, making long term borrowing more expensive. Inflation has been running above the Fed’s 2% target for five years and counting, and that changes the fiscal arithmetic. Rolling $500 billion of bills every week is fine until the market starts asking for a bigger toll. If borrowing costs rise further, or if money market rates jump because supply overwhelms demand, the harmless looking bill strategy could become another pressure valve in a macro system already running hot.

Then there is Korea, which still looks like AI mania ground zero. South Korea has become one of the purest expressions of the global AI trade because it mixes leverage, speculation, retail participation, and semiconductor exposure into one combustible cocktail. Daily index moves now look like single stock moves. That alone should make traders uncomfortable. When the AI trade sneezes in Korea, the rest of the world should stop pretending it is local weather.

EWY just printed a massive downside reversal candle despite the surging overnight. It is now below the 21-day moving average and flirting with a steep trend line, while the 50-day remains far below. You can debate whether 5% to 10% daily index swings belong in a serious market, but ignoring Korea would be a mistake. This is the global AI trade running on maximum leverage, and the spillover risk is no longer theoretical.

Retail investors have rushed into leveraged South Korean AI ETFs in search of quick money, often without fully understanding the products they own. Leveraged ETFs are trading tools, not long-term savings accounts. After a violent drawdown, many holders learn that break-even is not a fixed price. It is a moving target that can disappear over the horizon. , the 3x product, now needs to double just to return to levels traded only a few days ago. That is how leverage turns a drawdown into a broken escalator.

The KOSPI volatility gauge also exploded higher overnight as traders chased upside exposure into an 8% index rally. Upside volatility panic is rare. It is the sort of behavior seen in the final innings of the Dot Com bubble, when demand for upside optionality became so extreme that dealers struggled to supply it. That is not usually what the beginning of a move looks like. At current volatility levels, Korea is pricing roughly 5.6% daily moves. That is not a market behaving like a market. That is a casino wearing an index badge.

The speculation is no longer confined to young retail punters either. Koreans in their 50s and 60s, a generation traditionally linked to fixed deposits and real estate, are now embracing leveraged equity speculation funded with debt. Investors aged 50 and older accounted for more than 60% of the 27.2 trillion won, or $18.5 billion, margin loan balance at Korea’s top 10 brokerages during the first quarter, more than double last year’s level. That is not just FOMO. That is household balance sheet risk walking into the AI furnace.

The hidden convexity risk sits in the structure. Korea has one of the most reflexive volatility ecosystems in global equities. Massive retail participation, leverage, and structured products leave the market vulnerable to nonlinear downside once momentum reverses. ELS products, widely held by Korean households, effectively embed short downside optionality in the system and force dealers to dynamically hedge during sell-offs. In plain trader English, the same structure that can help levitate the market on the way up can turn into mechanical selling pressure on the way down. The rocket booster can become the gravity well.

Leverage mania is now embedded across cash equities, ETFs, and single stock products. SK Hynix has become the largest single-stock ETF exposure in the world, tied to a company that many global investors had barely on their radar a few months ago. The key point is brutally simple. Leverage works both ways. On the way up, it amplifies gains through forced buying. On the way down, it can accelerate selling with the same cold machinery. Korea remains the purest expression of the AI trade. If leverage, volatility, and speculation are reaching extremes there, the rest of the market should not treat it as background noise.

So this is where the tape stands. Tech is wobbling. Chips are cracking. IPO supply is pulling at the liquidity blanket. Strong macro is being treated as a rates problem. Oil is lower but not low enough to heal sentiment. Treasury bills are manageable but worth monitoring. Korea is flashing the kind of leverage signal traders usually regret ignoring. The market is not broken, but it is no longer floating on clean air. It is flying through a narrowing canyon with too much speed, too much cargo, and too many passengers leaning to the same side of the plane.

Get the helmets out.

Korea’s Trading Café Circus Is Not A Normal Market

Korea just reminded everyone this is not a normal market. It is a leveraged semiconductor circus trading with a loose wire hanging out of the dashboard.

The KOSPI’s violent rebound after the previous session’s collapse was not clean price discovery. It was positioning violence. It was the market checking who survived the margin call, who bought the dip with both hands, who sold the rebound to pay for yesterday’s bravery, and who got dragged through the gears of the AI beta machine.

This is where the Korea tape has become its own beast. Retail investors started the day as dip buyers and quickly turned into intraday profit-takers. Foreigners kept selling, especially in tech. Local institutions were left as the stabilizing bid, with buying concentrated in the same semiconductor names that now control the entire index pulse. It was less a market session and more a Korean retail trading café meet-up group discovering in real time that leverage works both ways.

SK Hynix ripping nearly 16% and Samsung Electronics jumping 9% tells you exactly what Korea has become. It still wears the costume of a national benchmark, but under the hood it is increasingly a leveraged semiconductor volatility product. When those 2 names move, the index does not need a macro thesis. It already has its marching orders.

That is the uncomfortable part. Korea may still be one of Asia’s cleanest expressions of the AI cycle, but it is also becoming one of the dirtiest expressions of AI positioning stress. The fundamentals may be strong, the memory cycle may have real legs, and Samsung and SK Hynix may still be world-class companies. But when great companies become the chosen battlefield for retail leverage, foreign liquidation, ETF plumbing, and institutional repair flows, they stop trading only on earnings and start trading on oxygen levels in the room.

The split inside the AI complex made the message even clearer. The core chip giants caught the panic bid, while the Nvidia-adjacent names that had rallied on collaboration dreams were left behind. That is not a broad AI resurrection. That is traders stampeding back into the core memory trade while leaving the second-ring tourists on the roadside with their hazard lights blinking.

This is why Korea is so difficult for institutions to trade right now. You cannot look at daily 8% to 10% index swings and pretend there is a clean signal sitting there with a bow on it. These are not ordinary benchmark moves. They are flow accidents dressed up as conviction. Retail flips from dip-buying to profit-taking. Foreigners keep selling into liquidity. Local institutions step in to stabilize the tape. The semiconductor giants do the heavy lifting. Then everyone pretends the index has spoken.

It has spoken, but not in the language of normal markets.

The message is that Korea is no longer trading like a calm national benchmark. It is trading like a high-voltage AI momentum barometer, where the entire market can be dragged higher or lower by a handful of chip names and a retail crowd that treats volatility like a national sport.

My trader view is simple. Do not dismiss the AI cycle just because Korea looks insane, but do not mistake a violent rebound for a cleared runway either. This is a tape for position sizing, not chest-thumping. It is a tape for respecting flow, liquidity, leverage, and the reality that when the ownership structure becomes unstable, even the best companies can become dangerous trading vehicles.

Korea is still investable. It is still important. It may still be one of the biggest winners of the AI capital cycle.

But right now, it is not trading like a market.

It is trading like a Korean retail café circus with Samsung and SK Hynix strapped to the front of the roller coaster.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.