The Musk premium remains the most expensive gravity-defying instrument on the board.

Takeaways

• did not just open for trading. It opened a new pressure chamber for markets, where scarcity, index demand, retail heat, sovereign money, and Musk mythology all collided on the same launch pad.

• The first day pop was not only about belief in rockets, Starlink, AI, or Mars. It was market plumbing doing what market plumbing does when too much money chases too little float.

• The dark market flows weather vane on perpetual derivatives pointed close to pay dirt because the speculative crowd had already pre-traded the story before the cash market got its first clean print.

• Valuation gravity has not disappeared. SpaceX still needs to turn the dream machine into cash flow, but for now the tape is rewarding narrative escape velocity over spreadsheet gravity.

• This was the cleanest message from the IPO: in a market starved for the next growth ark, SpaceX cleared the tower, the underallocated crowd chased the flame, and Wall Street was reminded that scarcity remains one of the most powerful fuels in the risk machine.

SpaceX Clears The Tower

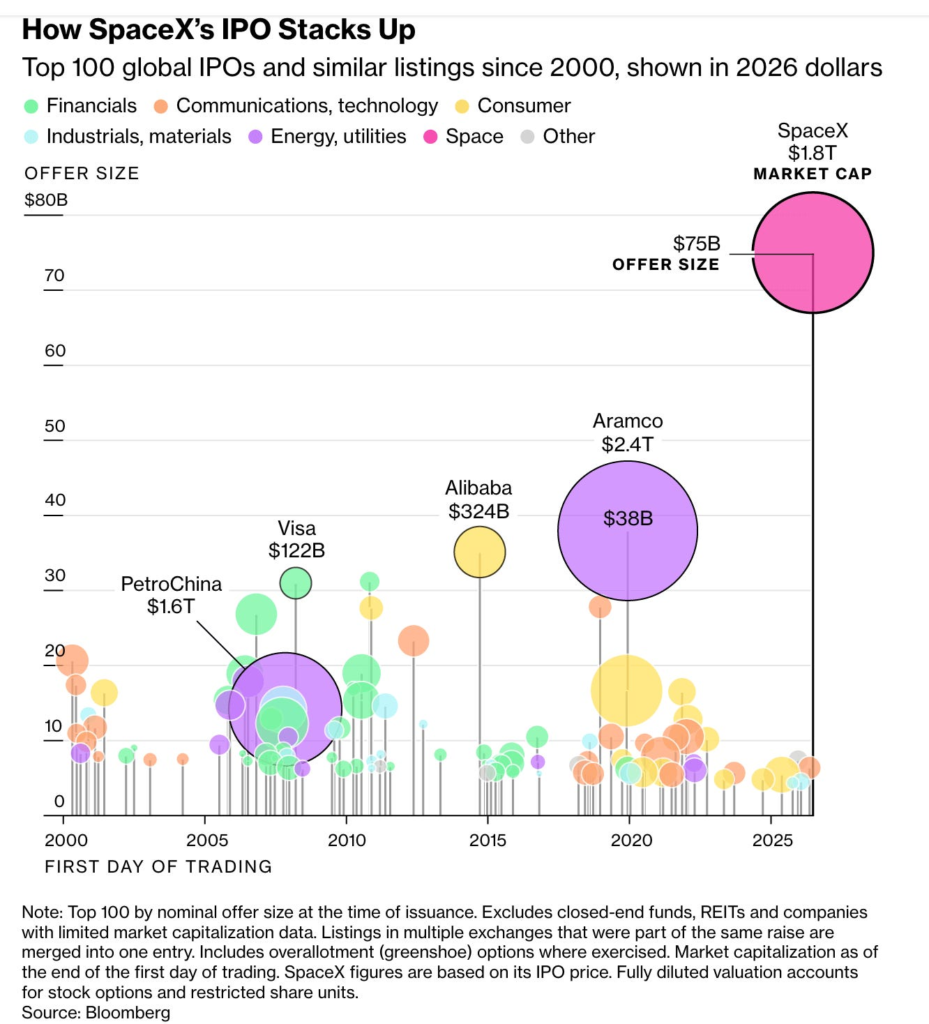

SpaceX did not trade like a normal IPO. It traded like a controlled burn in a market starved for a new growth comet. A $75 billion offering, the largest IPO ever, came out of the gate with enough thrust to send the stock as high as $176.52, roughly 31% above the $135 deal price, pushing the market value above $2 trillion and turning Elon Musk into the first trillionaire on paper. That was not simply price discovery. That was scarcity discovery, where the first buyer was not asking whether the model was clean, but whether there would be any paper left by the time the rocket cleared the tower.

The stock did not lift because investors suddenly solved the valuation riddle on launch morning. It lifted because the float was too thin, the demand stack was too tall, and the underallocated crowd was forced to chase the exhaust plume. More than $350 billion of demand came through the book from institutions and retail, while only a small tradable slice was made available. About 70% of the institutional allocation went to long-only investors and sovereign wealth funds, which means the stock was placed into stickier hands rather than sprayed into fast money accounts looking to flip the first print. That matters because the float did not just start tight. It started tight with a large chunk of the available stock already sitting in accounts less likely to sell into the first upside break.

The order book told the real story. Large asset managers wanted size. Sovereign capital wanted size. Gulf money wanted size. Kuwait wanted size. Some orders were measured in billions, yet close to one-third of firms that asked for stock received nothing. That is how you build a launch day squeeze without needing a classic short squeeze. You simply create an allocation drought, leave serious money under filled, and let every portfolio manager stare at a screen wondering whether the rocket is leaving the pad without them. The market was not buying only SpaceX. It was buying access.

Retail brought the second booster. More than $100 billion of demand came from the public crowd, but only around $15 billion of stock was allocated to that cohort. That left a vast army of would-be buyers outside the gate, cash in hand, adrenaline running hot, and no desire to explain why they missed the most hyped IPO in market history. The early Robinhood issues, with roughly 5,000 reported outages around the pressure point, were the perfect metaphor. The crowd wanted in so badly the pipes started to groan. Yet the remarkable part was not the glitch. The remarkable part was that the broader debut held together. A transaction this large could have turned into a market plumbing circus. Instead, it was orderly enough to give Wall Street the one thing it needed most: confidence that the machine could absorb a mega listing without coughing smoke.

That is why this IPO landed as more than a company event. It was a referendum on the entire growth complex. SpaceX already carried the premium of rockets, Starlink, launch dominance, defense optionality, orbit, Mars, and the Musk halo. But with xAI folded into the story, the listing became a public-market checkpoint on whether investors still have the appetite to fund giant AI dreams at giant multiples. In that sense, SpaceX was not just a stock. It was a weather balloon for OpenAI, Anthropic, and every private-market unicorn waiting on the runway, with a banker, a pitch book, and a valuation that needs public markets to keep believing.

Some traders will view this as the pivot point from a software-dominated market to a hardware-dominated market. For years, the public tape rewarded code, networks, platforms, and margin structures that scaled without much physical drag. SpaceX is a different beast entirely. It is rockets, satellites, launch pads, spectrum, data centers, chips, defence contracts, AI, and orbital infrastructure welded into one machine. This is the hardware comeback wearing a software multiple. That is the beauty and danger of the trade. When hardware gets priced like pure software, every missed milestone carries more weight because the market is not paying for yesterday’s income statement. It is paying for tomorrow’s orbit, next decade’s AI stack, and the possibility that the Musk premium remains the most expensive gravity-defying instrument on the board.

The bull case is easy to understand because the market can see the shape of the dream. Starlink offers the recurring revenue spine. Launch dominance provides the orbital toll booth. AI gives the company a new language for valuation. Defense and sovereign demand add strategic scarcity. Mars gives the story its mythology. Musk gives it the impossible premium that has turned betting against his ecosystem into a widow-maker trade for years. Expensive has never been the catalyst with Musk. Expensive is the weather condition. The mistake bears keep making is treating valuation as a timing tool when, in Musk’s world, valuation is often just the altitude gauge.

But gravity has not been repealed. It has merely been postponed. SpaceX posted a $4.28 billion net loss in the first quarter of 2026, and that number matters even if the market chose not to care on day one. A colder sum-of-parts view can put the company much closer to $600 billion, roughly one-third of where the market is now, marking it. That is not a rounding error. That is the distance between spreadsheet gravity and narrative escape velocity. Right now, narrative is winning. But gravity always keeps a seat in the cockpit.

The float is the fulcrum. Only about 4.2% of outstanding shares were available to trade on day one, which means the first session was never a clean referendum on long-term value. It was a controlled experiment in scarcity. When a mega-cap IPO releases a tiny amount of tradable paper into a market already hungry for AI, growth, sovereign scale, and Musk exposure, price can lift because there simply isn’t enough supply for the wave coming through the door. That is not some mystery. That is mechanics. A thin float plus giant unmet demand equals a beach ball held underwater. Once released, it pops.

This is where the dark market flows weather vane around perpetual derivatives came close to pay dirt. The synthetic market had already been whispering that demand was not polite, sleepy, or confined to the long-only world. It was leveraged, emotional, impatient, and global. Perpetual derivative appetite does not guarantee direction, but it can show where speculative oxygen is building before the cash market gets its first clean breath. By the time Nasdaq opened the door, the crowd had already pre-traded the story in its head. The stock became public, but the narrative had already been circulating through the risk machine.

There is another tailwind waiting in the wings, and it is not based on opinion. It is index plumbing. If SpaceX gets fast-track inclusion into major benchmarks, passive funds could be forced to buy as much as $6 billion of stock. Index buyers do not care whether Mars is profitable in the 2030s or whether AI deserves the current multiple. They buy because the rule book tells them to buy. In a tight float, that mechanical bid can keep the stock sticky, especially when active managers who received too little stock are still debating whether to chase now or explain later.

Still, day one glory is not the same as long-term durability. The market has seen this movie before. Figma surged 250% in its 2025 debut, only to surrender the magic and trade about 45% below its IPO price later. That is the warning label on every hot listing. The opening pop is a celebration of scarcity, not proof of permanent value. Companies with negative net income have also tended to lag profitable peers by more than 10% over the first 18 months after listing. Public markets can worship a dream at the opening bell, but they eventually ask for receipts.

That is the next test for SpaceX. The market has granted it a valuation passport into the most elite club on earth, but the visa has conditions. Investors will want proof that Starlink can scale, that AI can become more than valuation solvent, that launch dominance can turn into durable cash flow, that defense demand can compound, that governance risk does not become a discount, and that Musk control remains a feature rather than a pressure point. Public markets are patient with dreams only when the revenue bridge keeps extending.

The banking machine came in full formation, with the largest Wall Street houses leading the transaction and a deep bench of banks attached behind them. Price targets are already reaching as high as $190, which tells you the sell side race has begun. Once a stock this large enters the public arena, the debate changes. It is no longer about whether the dream is beautiful. It is about whether the next buyer has enough fuel to pay more for it.

My read is simple. SpaceX was priced for perfection, traded like scarcity, and landed like a macro event. The first day was not a blind mania melt-up. It was a clean burn through a rationed float, supported by institutional anchoring, retail heat, sovereign demand, derivative oxygen, and future index plumbing. But from here, the trade becomes more dangerous because the easiest money was the allocation mismatch. The next leg needs earnings validation, Starlink execution, AI traction, and enough market liquidity to absorb future supply without cracking the halo.

This is the new IPO playbook in one frame. The company sells only a sliver, the demand stack towers over the float, the underfilled crowd chases the break, derivatives sniff the heat, passive funds wait in the wings, and the narrative does the heavy lifting before fundamentals even reach the podium. SpaceX has become the market’s newest gravity-defying instrument, but gravity has not vanished. It has only been delayed. For now, the rocket cleared the tower, the tape applauded, and the dark flow weather vane pointed in the right direction. Close enough to pay dirt, but from here the market will want more than smoke, fire, and a perfect launch photo. It will want cash flow in orbit.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.