The 30% correction in Micron stock over the past month is not likely to change the main thesis regarding the ongoing shortage in the memory market. My initial estimates suggested that the imbalance between DRAM/NAND supply and demand could persist until the end of 2027, but after analyzing the potential impact of robotics on memory chip order trends, my expectations have improved, at least through the end of 2028. The record-high business margins, which were confirmed by the latest financial results, have been accompanied by exponential revenue growth. Of course, we should not overlook the risks associated with the macroeconomic environment, in which uncertainty surrounding the Fed’s interest rate changes through 2027 heightens the risk of profit-taking by investors. This article explores the potential impact of ’s listing on the Nasdaq on Micron’s stock, which may gain three additional drivers for its ongoing record-breaking growth.

Micron’s Competitive Moat Remains Intact

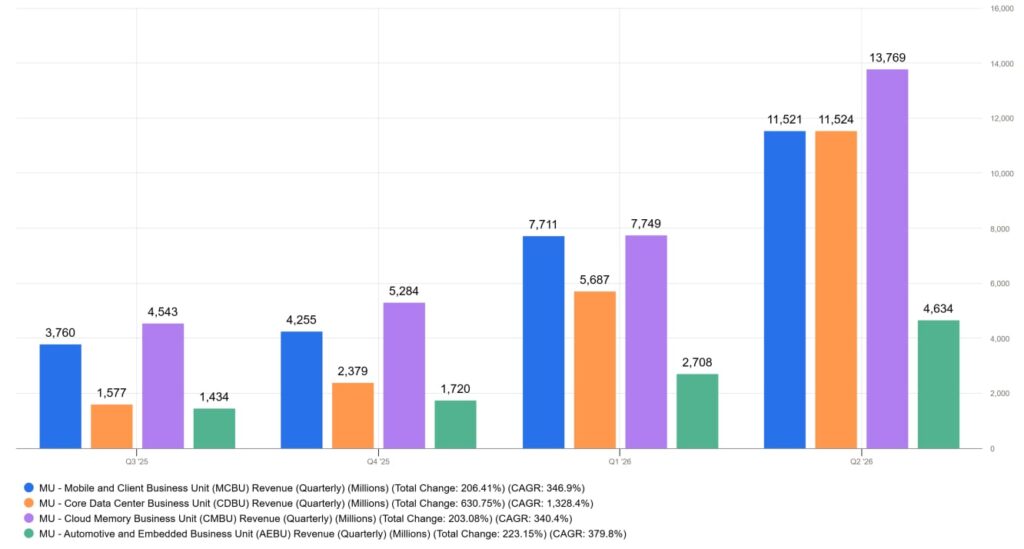

Persistent memory shortages, increased CapEx forecasts from hyperscalers, and even improved valuations for South Korean competitors are supporting Micron’s competitive moat. The company’s diversified portfolio, which offers memory chips across all segments, ensures that it can serve a wide range of customers. This includes not only hyperscalers and data center providers, as well as manufacturers of computers, mobile devices, and automakers. At the same time, at the end of Q2 2026, growth in revenue was observed across all segments. At the same time, analyzing Micron’s sales structure, we should note that HBM3 and HBM4 chips play a leading role. They are essential for building AI infrastructure, and their importance has been confirmed by the major players in the AI supercycle. The largest share of sales comes from chips in the DRAM segment. In Q2 2026, sales amounted to $31.3 billion, which is 343% more than a year earlier. At the same time, NAND chip sales also grew by an impressive 361%.

At the same time, analyzing Micron’s sales structure, we should note that HBM3 and HBM4 chips play a leading role. They are essential for building AI infrastructure, and their importance has been confirmed by the major players in the AI supercycle. The largest share of sales comes from chips in the DRAM segment. In Q2 2026, sales amounted to $31.3 billion, which is 343% more than a year earlier. At the same time, NAND chip sales also grew by an impressive 361%.

The Effects of SK Hynix’s Nasdaq Listing on Micron’s Stock Growth

In my view, Micron has a competitive advantage stemming from its national significance to the U.S. economy and industry. This is the largest memory chip manufacturer, implementing major projects to scale up production capacity within the United States. Given that, under current circumstances, the technological race and geopolitical tensions remain very much alive, ’s stable production and supply capabilities may play an even more important role in the future.

But that doesn’t mean the setbacks faced by Micron’s main South Korean competitors are a good thing. In fact, their progress, including better forecasts and actual performance, only helps Micron’s market valuation. So, what’s the significance of SK Hynix’s historic ADR listing on the Nasdaq, which will raise $28 billion for this South Korean competitor? It may seem at first glance that this event will put competitive pressure on Micron. But in fact, it is a major tectonic shift for the entire memory industry, which could trigger a series of factors leading to a large-scale revaluation of MU shares in an upward direction.

Firstly, SK Hynix’s “Korean discount” will be eliminated, contributing to a revaluation of Micron as well. As the South Korean giant was inaccessible to U.S. investors in the domestic market, its multiples were undervalued. The issue, though, will boost these multiples, which will make Micron’s multiples more fair as well (for example, SK Hynix’s current P/E ratio is 18.3x, compared to Micron’s 22.0x). The bottom line is that the valuation ceiling for memory players will shift to higher levels.

Secondly, an additional driver for the inflow of global institutional capital will emerge. Many investors face administrative barriers to purchasing shares on the Korean KOSPI exchange. Since SK Hynix’s listing on Nasdaq will draw additional investor attention to memory market assets, this may increase liquidity from general-purpose funds as well. Since Micron serves as a national benchmark in the U.S., this may further boost demand for its shares.

Finally, the listing of SK Hynix on the Nasdaq will highlight Micron’s key advantage as the leading U.S. manufacturer. The trading of both stocks on the same exchange will make it easier to conduct a comparative analysis of them. In this context, the unique value proposition of Micron becomes more noticeable and evident, resulting in a more sustainable geopolitical premium being factored into its valuation.

Conclusion

This fundamental investment thesis, with a “Buy” recommendation for Micron, is unchanged, because the structural shortage in the memory market, which is being driven not only by the AI supercycle but also by orders from automakers, will definitely continue the bullish trend at least through 2028. The balanced exponential revenue growth across all segments clearly demonstrates not only the preservation of the company’s “moat,” as well as its strengthening. However, most investors overlook the potential upside from SK Hynix’s listing on the Nasdaq, as it could trigger an upward revaluation of Micron’s stock. Thanks to the two industry leaders trading on the same exchange, three key drivers will be set in motion: elimination of the “Korean discount,” an influx of global capital, and a strengthening of the geopolitical premium.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.