Quantum Computing Inc. (QUBT) Mid-Long Term Company Analysis

Recommendation: Sell

Detailed Recommendation: Reduce position size over a longer time horizon (e.g., several weeks) using reverse dollar-cost averaging to hedge against temporal price movements. The opportunity cost of holding QUBT appears too high relative to other potential allocations.

Company Introduction

Quantum Computing Inc (NASDAQ:QUBT) is a Delaware-incorporated company founded in 2018 and listed in 2021, which focuses on developing quantum-computing technologies based on photonics and non-linear quantum optics. They are headquartered in Hoboken, New Jersey, have a market cap of around $1.6 B, and employ around 50 people. After their 2022 merger with QPhoton Inc., QUBT’s technology platform centers around two primary areas:

- Entropy Quantum Computing: photonic quantum computing systems designed to operate at room temperatures without requiring cryogenic cooling, which most most quantum systems rely on

- RCaaS (reservoir computing-as-a-service): a non-linear computing service aimed at optimization and machine learning workloads.

The company targets applications in network optimization, modeling, and satellite imagery. With the 2025 acquisition of Luminar Semiconductor, QUBT is expanding into semiconductor components that could support their photonic systems. The company still remains in the pre-commercialization phase and record a sub $1M revenue, which remains the main hindrance when performing financial analysis using different ratios.

Main Competitors

- Closest public companies: , ,

- Capital-heavy competitors: IBM, Google (GOOG), Microsoft(MSFT)

Early-stage quantum and photonics companies are used as the primary comparison group for QUBT, because they operate under relatively similar market dynamics and capital structures as QUBT. Based on stock price behavior and financial statements, these companies tend to move in broadly similar patterns, characterized by high volatility and shifts in market enthusiasm. This makes it difficult to determine a clear directional trend for small and mid-cap companies operating in quantum computing, photonics, and quantum optics industry.

It would be less meaningful for QUBT to use much larger companies, like IBM or Google, as direct comparables because those companies have highly diversified business models and their exposure to quantum technologies is usually restricted to specific research divisions that typically aim to spearhead specific innovation initiatives rather than represent core revenue drivers for those enterprises.

Competitor Operational Overlap Analysis

While all four companies (QUBT, IONQ, RGTI, QBTS) are quantum computing oriented businesses, their underlying technologies and commercial stages differ substantially. IonQ (IONQ) uses trapped-ion technology (individual ions suspended in electromagnetic fields and manipulated with lasers), and has managed to achieve commercial deployment through agreements with cloud providers (AWS, Azure, and GCP). It is the most commercially sophisticated of the above mentioned companies, having surpassed $100M in revenue in FY2025. It also has the highest market cap by far of the four companies (over $12 B).

Through its Quantum Cloud Services platform, Rigetti Computing (RGTI) focuses on hybrid quantum-classical workloads and constructs superconducting qubit systems.

D-Wave Quantum (QBTS) takes a different approach focusing on quantum annealing, rather than gate-based computing. While this limits its applicability to certain problem types, it has allowed D-Wave to build the longest commercial track record among pure-play quantum companies with enterprise use cases already deployed in areas such as logistics and materials science.

QUBT’s photonic approach is the most differentiated of the group, but also the least commercially proven so far. Unlike ion-trap or superconducting systems, photonic architecture doesn’t require extreme cooling, which could offer a meaningful long-term cost and scalability advantage. However, the company has yet to demonstrate this benefit in commercially deployed systems that could be monetized and deliver concrete longer-term commercial value.

While all four companies’ valuations are dependent on early-stage, more speculative, investors and early-stage revenue streams (with the slight exception of IONQ, which has already developed some operating cash inflows), they all lack large-scale commercialization capabilities, which is typical of emerging technologies, such as quantum and photonics. However, of all of them, QUBT remains the easiest pre-commercialization stage, by all financial and operational measures considered in this article.

Valuation Data

The company’s revenue has shown modest growth (based on recent 10-K filings), increasing from $358k in 2023 to $373k in 2024 and approximately $615k in 2025. However, COGS has moved broadly in line with revenue, meaning profitability improvements remain infinitesimal. Pre-tax losses improved somewhat during this period, narrowing to approximately –$68,542 in 2024 and –$18,674 in 2025, though the company still operates firmly in the research-stage phase incurring steady losses.

The stock itself has experienced extreme volatility since late 2024 until now with a noticable recent price uptick. From around-$1 territory through most of 2024, shares exploded higher into January 2025, briefly touching a peak before falling back sharply. The 52-week high of ~$26 was recorded in October 2025, after which the stock entered a sustained downtrend. That decline accelerated into early 2026, reaching a 52-week low of $6.18 on the 30th of March 2026. Since that, the stock has recovered driven by ephemeral sector-wide enthusiasm driven partly by Nvidia releasing the “Ising” error-correction model. In April, all pure quantum play companies (QUBT, IONQ, RGTI, QBTS ) experienced stock upticks from the previous stagnated lows, with the bulk of the move concentrated in the week of April 14th (IONQ gaining 20.1% to $35.76, QBTS up 15.8% to $16.97, RGTI up 11.5% to $16.87, and QUBT up 11.5% to $8.11 in a single session. For the month as a whole, QBTS rebounded 26.6% and RGTI gained 14.5%). The fundamentals don’t justify that level of increase, which highlighting its speculative and expectation-driven nature.

Operations & Growth Drivers

QUBT’s photonic quantum computing approach appears to be more capital intensive than its peers who have already started to gradually transition to contract- or cloud-based revenue models, for example IONQ and D-Wave have already established some enterprise clients. QUBT is still in that pre-commercial, R&D capital intensive spending phase and their value relies solely on market confidence/enthusiasm. The commercial value is simply not there yet, as opposed to more highly capitalized competitors.

Moreover, QUBT is more exposed to investor speculative enthusiasm, because unlike their peers they can’t yet diversify and anchor into any kind of government contracts, cloud partnerships or enterprise deployments – considering that their tech remains immature. Even the pure tech-oriented outlook reinforces the bearish stand, as IonQ’s trapped-ion systems are already deployed across cloud platforms and D-Wave’s annealing technology is used in optimization contracts, QUBT’s product line (centered on reservoir computing modules) have not yet generated any significant revenue levels.

Industry Sentiment

Google Trends data suggests that public interest in photonics and quantum computing technologies increased significantly beginning in late 2024, just before QUBT shares rallied toward roughly $18 in early 2025. Interest then fluctuated, more or less, alongside the stock price and appears to have peaked around September 2025, after which Google search activity began to decline sharply. This pattern mirrors the stock’s price behavior, to some extent, and suggests that investor enthusiasm for the sector may be partly driven by ephemeral waves of public attention and technological hype (especially in the form of spillover effects from mainly AI related investments), rather than sustained commercial adoption of the quantum computing sector, which remains an early-stage deep-technology industry characterized by:

- very long commercialization timelines

- heavy R&D expenditure requirements

- minimal current revenue relative to long-term expectations

Much of the recent momentum in sector stocks appears linked to AI infrastructure hype spilling into adjacent technologies, as well as announcements of research breakthroughs by major technology behemoths.

For example, in December 2024 Google announced its 105-qubit “Willow” quantum chip, claiming it could complete a benchmark computation in minutes that would take a classical supercomputer an estimated 10²⁵ years. Announcements like this, alongside broader AI-driven optimism, have contributed to speculative momentum across small-cap quantum technology stocks.

Since then, investor enthusiasm has cooled somewhat as markets reassessed the long commercialization timelines for quantum and mainstream AI investments, valuations corrected following large rallies, and the broader macro environment shifted toward lower risk tolerance for speculative technology companies, especially smaller and mid sized ones.

Other Quantitative Comparison

QUBT currently generates negative earnings, meaning some traditional valuation metrics such as P/E ratios are not applicable. As a result, this analysis focuses on alternative indicators:

- Price-to-Sales (P/S) / Market Cap-to-Revenue

- Year-over-year revenue growth

- R&D spending as a percentage of revenue

- Relative valuation compared to similar research-stage competitors

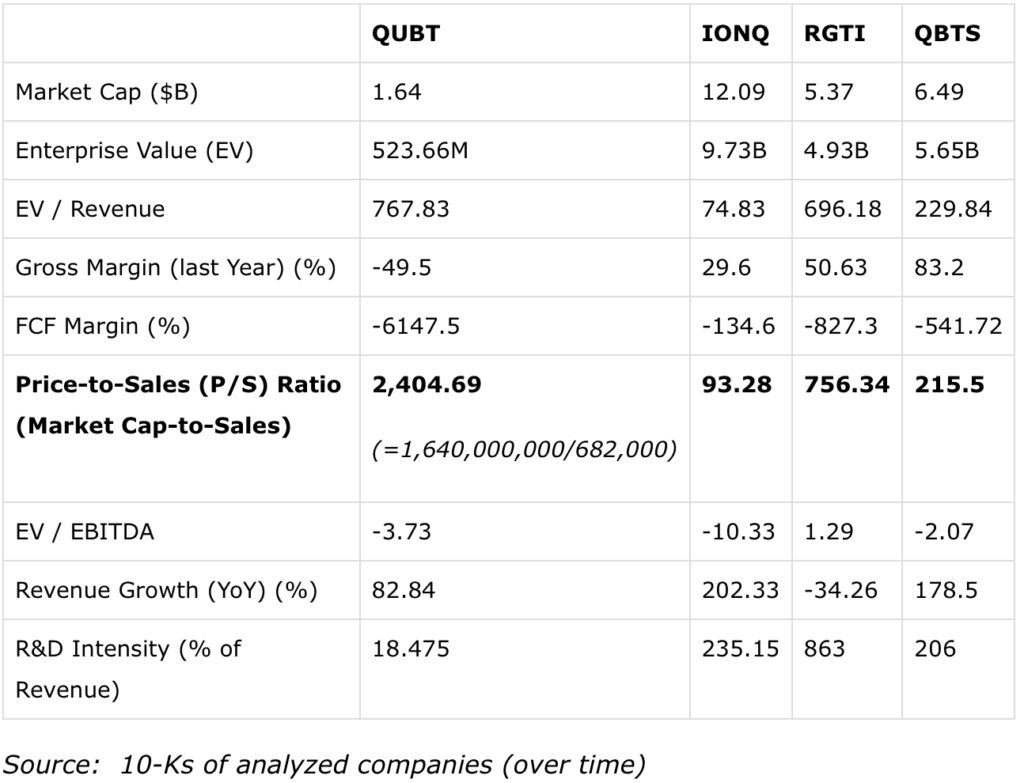

Many of these ratios remain detached from underlying fundamentals, mainly because revenues are extremely small relative to market capitalizations. As a result, these metrics fluctuate quite signifficnatly over time and vary widely across companies. For example, the market capitalization-to-sales ratio currently stands at approximately:

- QUBT: ~2404

- IONQ: ~93

- RGTI: ~756

Even though that kind of elevated ratios are common among early-stage, high tech sector companies, where valuations are mostly driven by future expectations, that exaggeration for QUBT is particularly apparent. When combined with uncertain commercialization timelines, and constantly evolving technological standards (especially coming from the big players), this creates a level of valuation uncertainty that is unusually high – even relative to other emerging technology sectors.

Cash Runway and Burn Rate

QUBT’s balance sheet might appear solid at first glance. In 2025 the balance sheet recorded ~$738M in cash, and with ~$19.3M in operating burn over the first nine months, the implied runway stretches several years at least with the current burn rates.

This liquidity, however, is entirely externally funded. In 2025, the company raised over $1.5B through two equity placements ($500M in Q3, followed by $750M in Q4) substantially diluting existing shareholders. Against ~$682,000 in revenue and a ~$51.1M operating loss, the business remains pre-commercial, with capital effectively sitting idle relative to output.

Meanwhile, operating expenses ( around $10.5M per quarter) have stepped up meaningfully, as both Research&Development and General&Admin. expenses roughly doubled (without a corresponding revenue growth), which appears to be a constant missing elements in this multifaceted analysis: the lack of foreseeable revenue or concrete commercial value generating ability paralyzes every metric we look at.

By contrast, IonQ generates over $130M in revenue and D-Wave has other contract-based recurring income stream. Even though QUBT’s cash reserves and liquidity are considerable (considering the scale of their operations), they are entirely artificial and disconnected from the company’s underlying operational capabilities.

News & Catalysts

The company’s $110M all-cash acquisition of Luminar Semiconductor (semiconductor components manufacturer) in Dec. 2025 appears exorbitant compared to QUBT’s current scale and revenue base, which remains below $1M annually. For a company still in the research and early commercialization stage, the transaction introduces additional financing and liquidity risk, particularly if the acquisition does not lead to meaningful near-term revenue. The market reaction reflected these concerns, with the stock experiencing increased volatility the following months after the announcement.

Some investors might expect that this vertical integration will provide longer-term growth and allow QUBT for differentiation opportunities, due to Luminar’s capabilities to manufacture semiconductor components, which are necessary for building quantum and photonics systems. However, that assumption is fallacious due to the following reasons:

- QUBT has failed to prove any kind of commercial or deployment success with their quantum- or photonics- based products and making vertical integration at such an early stage is premature and won’t turn the tables for this company

- A $110 M all-cash acquisition is approximately 180 times the current revenue levels of QUBT and thus implies an extremely high bar for this acquisition to be value-creative, which is long shot, as mentioned in the first bullet point. That, combined with the fact that such an acquisition entails operational and managerial complexity, difficult to be handled smoothly by a 50-employee enterprise, makes it a distraction from the main objective QUBT should be focusing on right now: expanding its revenue base and establishing key partnerships to enable medium-term commercialization of their technology, just like other players in the field – at least to some measurable extent.

Other Acquisitions in the Field

By comparison, consolidation in the sector has largely been driven by better-capitalized players. For example, IonQ acquired Entangled Networks in 2023 to expand its networking capabilities and Rigetti Computing focused more on government-funded research initiatives. QUBT’s acquisition stands out as relatively aggressive given their size, while broader investor sentiment toward small-cap quantum companies has recently become more cautious as markets reassess monetization capabilities on quantum technologies, which are largely dependent on the success of mainstream AI-related initiatives.

Options Chain Analysis

Based on the options chain data from OptionCharts, QUBT’s derivatives market currently displays several signs of limited liquidity and uneven pricing. Implied volatility across strike prices for call options appears irregular and in some cases unusually elevated. This may partly reflect the stock’s historically large price swings and the difficulty of accurately pricing short-dated options.

Open interest is relatively concentrated in a few strike prices, while remaining thin across much of the options chain, which generally indicates limited participation from larger institutional options investors.

Some call options also exhibit delta values that appear inconsistent with their implied volatility levels, suggesting potential micro mispricings. This behavior is typical for thinly traded options markets where market makers adjust prices conservatively to compensate for limited order flow. Short-dated implied volatility levels near 80–100% around the $7–$9 strikes further reflect the market’s expectation of continued large price swings.

Alternative Data Sources Analysis: Employee Headcount over time:

Employee headcount trends further highlight QUBT’s relatively small operational scale compared with its competitors. While other companies have expanded their workforce substantially in recent years, QUBT’s growth has remained modest. IONQ increased its headcount from 202 employees in 2022 to 1132 in 2025, reflecting scaling of research and organic growth. QBTS also expanded meaningfully, growing from 215 employees in 2022 to 388 in 2025, while RGTI shows slower but still positive growth, rising from 144 to 164 employees over the same time period. In contrast, QUBT’s workforce increased only marginally from 44 employees in 2022 to 50 in 2024, suggesting a significantly smaller operational workforce relative to other publicly traded optics & quantum computing companies in the industry.

Risks

The primary risk to a sell recommendation is the possibility of renewed speculative momentum in the quantum computing sector. The industry remains closely tied to broader AI-driven technology narratives, and investor enthusiasm could spike again if major technological announcements occur, spurring investor hype once more.

Another risk are spillover effects from large tech companies increasing investment in quantum research. Breakthrough announcements from companies, such as IBM or Google, could temporarily re-galvanize speculative interest across mid-cap public quantum companies.

However, current market sentiment appears more skeptical following broader discussions around AI-fueled valuation bubbles and the market’s increasingly impulsive reaction to technology earnings surprises. Even established technology firms have recently experienced disproportionate price reactions to earnings reports (like the Q4 2025 Oracle earnings report, when the stock fell sharply despite beating analysts’ earnings expectations), illustrating the current fragility of sentiment in overvalued technology sectors.

Opportunity Cost of Owning QUBT Stock

The main opportunity cost of owning QUBT is not only accepting extremely bloviated and unpredictable financial ratios, such as the ridiculous P/S of over 2,400, but also foregoing the opportunity of owning stocks in the sector with better risk/reward profiles that are better capitalized and more predictable mid term. For example, QUBT is trading at EV/Revenue of around ~768x and records a sub $1M revenue levels, while EV/Rev for IONQ is ~75x and they’re the first pure-play quantum company that crossed $130M in revenue There is no specific identifiable business moat or tech edge for QUBT that would justify holding that kind of risk right now, especially considering the volatility and other risks involved.

Conclusion:

While the quantum computing sector continues to attract attention and long-term technological optimism at irregular intervals and with varying levels of intensity, QUBT currently lags behind their closest peers in terms of scale, commercialization progress, and financial traction. Given this positioning and the sector’s volatility, the recommendation is to gradually reduce exposure using reverse dollar-cost averaging rather than exiting all at once, as there are no imminent dangers short-term that threaten the business fundamentals or the stock market attached valuation. That is also why the stock is not recommended as a short candidate (or purchasing a long term put option); instead, investors should consider rebalancing capital toward stronger competitors within the sector or focusing only on shorter term plays that leverage factors other than looking at business fundamentals and commercial value generating ability.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.