Private market investments have seen a significant increase in allocations across institutional portfolios and, increasingly, private wealth strategies over the past decade.

The traditional rationale is well known to be that investors earn an illiquidity premium in exchange for locking up capital in assets that cannot be readily traded. This is a bug that investors can exploit to earn a higher return on their capital.

However, this may not be the whole story anymore. What if illiquidity and the lack of frequent market pricing is not simply a cost to be compensated for, but also a feature investors actively value? In other words, what if part of the appeal of private markets is not just higher expected return, but a smoother and psychologically easier experience of investing? Instead of being the illiquidity premium it’s now closer to an illiquidity discount.

In that case, investors may not only be compensated for illiquidity. They may also, at least implicitly, be paying for reduced visible volatility.

Private markets do not remove risk. The underlying assets are still exposed to the same economic factors as their public market equivalents. The smooth returns are an artifact of stale pricing rather than superior stock selection or company management. What differs is the mechanism and frequency of price discovery. Because valuations of private assets rely on appraisal-based or modelled inputs rather than liquid market pricing, reported returns tend to appear significantly smoother than those of public equities.

This creates an important distinction: smoother reported returns are not the same as lower economic risk or uncorrelated returns.

Investors often behave differently in environments where volatility is highly visible. Daily price movements can encourage tilted behaviour such as overtrading, emotional reactions, and poorly timed decisions, particularly during periods of stress or exuberance. By contrast, less frequent pricing can reduce the tendency to react to short-term noise rather than underlying fundamentals.

This helps explain why fee levels in private markets can remain elevated despite growing scale (more liquidity!) and competition. Investors may not simply be paying for illiquidity as a constraint, but also for a return profile that appears more stable and less volatile over time.

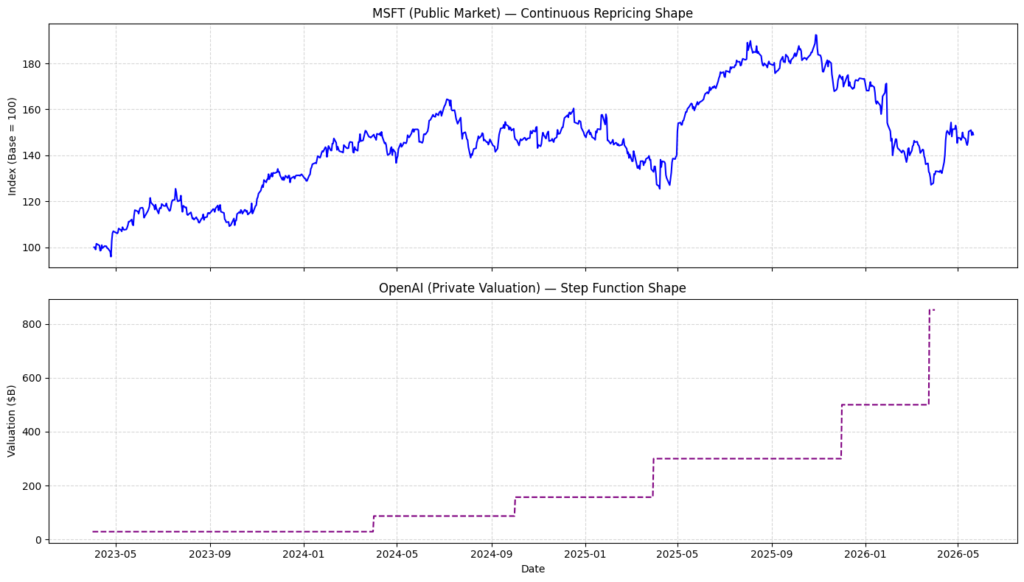

A useful comparison can be drawn with public market companies such as or , where price discovery is continuous and highly reactive. By contrast, private companies such as OpenAI or Anthropic—where valuations are updated far less frequently—may appear to follow a smoother trajectory, even though the underlying business risks and value creation processes remain highly dynamic.

— OpenAI (Private Valuation)")

Source: MSFT daily prices from Yahoo Finance (via yfinance). OpenAI valuation points compiled from publicly reported funding rounds and secondary share sale estimates (2023–2026).

Ultimately, private markets may not simply represent compensation for illiquidity. They may also represent a trade-off: investors exchange liquidity and transparency for a smoother return experience and a more psychologically tolerable path through risk.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.