The harder part begins from here.

Takeaways

-

The collapse in Brent has removed much of the immediate inflation fear, but the Fed is still treating the earlier shock as something that may leave a mark. The market is no longer trading a simple oil-relief story; it is now trying to balance cheaper energy against firmer rates, a supported dollar and a more cautious Fed.

-

Technology remains the strongest source of market momentum, but the AI trade is becoming more selective as investors demand evidence that enormous capital expenditure can produce durable earnings.

-

The next AI winners may extend well beyond software and chips into power, logistics, industrial capacity and the real-world framework required to sustain the buildout.

-

The reversion trade has largely done its work. From here, the market is likely to reward discipline, earnings delivery and companies that can make capital work harder.

A More Demanding Fed

US equities finished the week higher, with the gaining almost 1%, but the better way to read the move is not as a clean all-clear signal. It was a market trying to absorb one very large relief valve opening in oil just as another source of uncertainty began tightening the screws around rates.

Only a month ago, the market was still staring at the Strait of Hormuz as though it might become the economic equivalent of a blocked artery. Every headline about shipping, flows and physical barrels carried the potential to reprice inflation, complicate the global growth outlook and force central banks into an even more defensive posture. was being discussed in the familiar language of crisis, with $100 the first milestone and much higher levels sitting just beyond it should physical disruption take hold.

That whole narrative has now shifted with remarkable speed.

The reopening of Hormuz has helped pull front-month Brent back below $80 per barrel, down roughly 30% from where it stood only a month ago. The market has effectively removed a large part of the war premium before the macro data has even had time to catch up. Cheaper oil does not solve every problem, but it does reduce the pressure building through transport, freight, consumer budgets and headline inflation. It changes the weather, even if it does not guarantee blue skies.

For equities, that should have been a straightforward tailwind. Lower energy prices usually offer some breathing room to consumers, reduce margin pressure for energy-sensitive businesses and take one of the uglier inflation risks off the table. Industrials responded accordingly and finished the week among the stronger sectors, which makes sense in a world where the cost of keeping the global machine running has suddenly become less burdensome.

But the week was never only about oil.

Just as the market began to relax around the energy story, the first FOMC meeting under Chair Warsh reminded investors that the Fed is not yet prepared to take the same leap of faith. The immediate move in the after the meeting was sharp, and while some of that reaction softened into Friday, rates remain meaningfully above their pre-war levels.

That is the tension now sitting underneath the market.

Oil is saying the shock may be fading. The Fed says it is not yet ready to conclude that the damage has passed. The difference matters because markets can live with lower oil prices and slightly higher yields for a while, but the balance becomes more fragile if investors begin to believe that energy relief will not be enough to stop a firmer dollar, a sticky front end, and a central bank increasingly focused on defending its credibility.

The equity market handled that tension well this week, but not with the carefree exuberance of a broad risk-on surge. Investors bought the relief, but they did so selectively. The easy first trade was to fade the most stretched war-premium expressions, lean into relief in risk assets, and step away from the assumption that every barrel trapped in the Gulf would remain there forever. Much of that reversion has now happened.

The harder part begins from here.

Technology once again led the market, which is revealing because tech was not rallying simply because oil fell. It was rallying because the AI capital expenditure story remains the central current pulling capital through the equity market. Memory, storage and semiconductor capital equipment names were particularly strong as investors continued to focus on the infrastructure required to support the AI buildout rather than merely the more speculative edges of the application story.

The large technology complex also had a good week, although the broader message is becoming more nuanced. The market still wants to own the AI theme, but it is beginning to ask more difficult questions about where the spending is going, what it will earn and whether the extraordinary capital intensity now building across the sector can eventually be turned into durable returns.

That is the shift worth watching.

For much of the post-GFC period, companies were rewarded for being capital-light, buying back shares, keeping balance sheets neat and allowing low rates to do much of the valuation work. The new cycle is likely to demand something more tangible. Companies are being pushed to invest in data infrastructure, energy capacity, supply chains, compute, logistics and physical resilience. The winners will not simply be those spending the most. They will be the ones capable of turning that spending into revenue growth, lower costs, stronger margins and returns that can survive a less forgiving rates backdrop.

The AI story is therefore becoming less detached from the real economy than many investors first imagined.

AI may begin with code, models and chips, but it eventually arrives at power grids, cooling systems, , industrial capacity, logistics networks and the cost of financing all of it. The digital economy is no longer floating above the physical one. It is increasingly directly tied to it, which is why the market’s next leaders may not look exactly like the winners of the last decade.

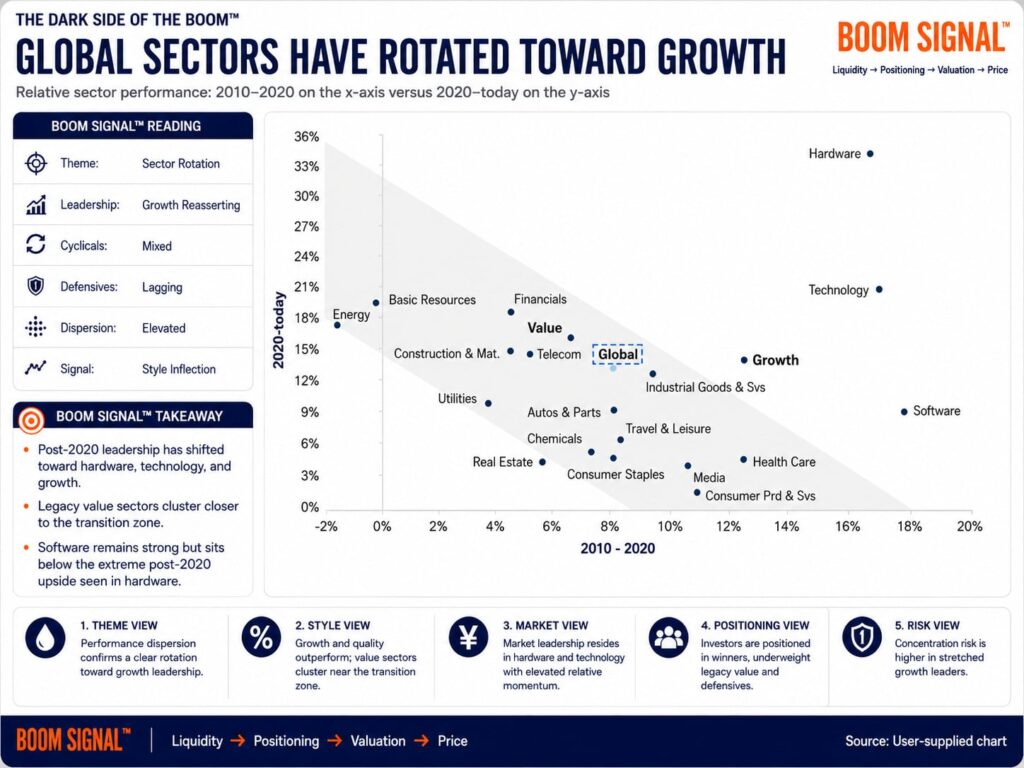

Here is a screen grab where the picture is worth a thousand words

The first chart captures the changing shape of market leadership. Areas that struggled during the long stretch of low rates and abundant liquidity are finding a more natural role in a world where inflation, regionalization, capital expenditure and industrial resilience matter far more.

Asset-heavy businesses are no longer simply old-economy ballast in a technology-led market. They are increasingly part of the technology trade itself. The companies that provide the power, capacity, materials, networks and industrial framework beneath the AI buildout may be just as important as the companies writing the software at the top of it.

That does not mean the market has abandoned mega-cap technology. Far from it. But it does suggest that the next phase may be more selective and more demanding. Investors will increasingly need to distinguish between companies building genuine economic engines and those simply spending heavily out of fear of being left behind.

Next week will provide a useful test of whether this balance can hold. May on Thursday will tell us whether the cooling in oil is beginning to filter through the inflation narrative quickly enough to ease some of the pressure around policy. Friday’s University of Michigan update will offer a more direct read on how households are responding to the combination of still-high rates, shifting energy costs and an increasingly uneven economic backdrop.

’s earnings on Wednesday will also be important, not only for the memory cycle but for the broader AI infrastructure story. Investors will be looking less at the quarter that has just passed and more at whether the company’s guidance supports the view that this remains a genuine capacity cycle rather than a market attempting to price perfection too early.

FedEx (NYSE:), Carnival (NYSE:), KB Home (NYSE:), Commercial Metals (NYSE:) and Paychex (NASDAQ:) should provide a useful counterweight. Their results will give the market a more practical read on the consumer, freight, housing, construction and corporate spending environment, which may matter just as much as the latest AI headline once the next earnings season begins to take shape.

For now, the market has managed to move from an oil shock to an oil relief rally without losing its footing. But the path ahead is less about broad beta and more about whether lower energy prices can offset a that is still sounding cautious, a that remains firm and a rates market that has not fully accepted the idea that the inflation scare is over.

The easy part of the reversion trade may be behind us. The next phase will focus on earnings, capital discipline, and identifying which companies can turn this great investment wave into something more durable than a very expensive promise.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.