Sell in May? Ha! Try “buy in July.”

Truth is, summer is the best time to troll for dividend deals—especially July. We’re going to “back up the truck” on two tickers in a sec.

Why July?

Because it’s the strongest month of the year for stocks, according to a 2024 report from the Carson Group, a financial-advisory firm. Here’s the upshot: Over the 20 years leading up to July 2024, the rose 2.3% on average.

And that’s just the average. Many years saw bigger gains than that.

This is our short-term play.

On the horizon, we’ve got the midterms. We’re not going to linger on that dreaded event. Suffice it to say, the vote is not what we’re interested in—it’s what traditionally comes in the year after it: stock-market gains.

A May study by RBC Wealth Management sets the table here. Going back to 1932, it found that the year following the midterms was the strongest in the four-year presidential cycle, with S&P 500 rising 14% on average.

The bottom line for us is that we’ve got a nice setup for gains this summer, plus another price pop setting up for 2027.

And despite what the headlines say, inflation (and interest rates) will come down. We’re already seeing it in oil prices, and the International Energy Agency (IEA) actually forecasts an oil glut next year.

Oversupply of the goo is fuel (sorry, couldn’t resist!) for growth. It’s an inflation-killer, too.

But we don’t want to be naïve. There’s certainly concern out there. But at times like these, it pays to remember the old stock-market adage: Stocks climb a wall of worry.

They’re certainly doing that now! And my indicators suggest they’ll keep it up. That makes now a good time to buy. Here are two dividend-growth plays to put on your list.

ITW: Hated By Wall Street, Loved By Dividend Investors

Illinois Tool Works (NYSE:) (ITW) is one of those stocks analysts hate. That’s because it’s basically an umbrella name covering a range of businesses that aren’t really connected.

Kitchen ovens and fryers? ITW makes ’em under its Hobart and Vulcan brands. Gear for testing electronics? It makes that, too. Fasteners and components for cars? Check.

It’s enough to drive Wall Street—which loves a “clean” single-product story—batty! According to the WSJ, and only two analysts covering the stock rate it a buy right now, with 11 at hold, two “underweight” and five sells. Perfect. We love disliked stocks like these because as they beat low expectations, more analysts come onboard, creating a feedback loop that boosts its price.

And there’s every reason for that to happen.

For one, the company follows what it calls the 80/20 model, where it zeroes in on its biggest/most profitable clients or products—the top 20% or so—which the company sees as providing the bulk (or 80%) of the company’s sales. That tight focus keeps margins high: in Q1, operating margins rose 60 basis points, to 25.4%.

Revenue also jumped a tidy 5% and EPS gained 12%. And management raised full-year guidance by $0.10, to between $11.10 to $11.50. The stock trades at a reasonable 24-times the midpoint of that range.

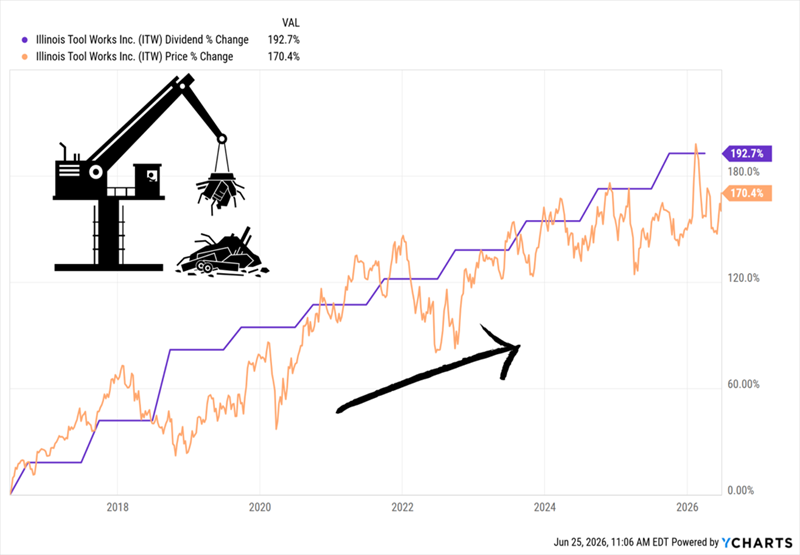

Which brings me to another reason why ITW is overlooked: the dividend. As I write this, shares yield 2.4%, which sounds okay—until you look at the company’s payout history:

ITW’s “Industrial Strength” Dividend Magnet

As you can see, over the last decade, ITW has nearly tripled its dividend. You can also see what I call the “Dividend Magnet” in action: The share price has climbed in lockstep. That gap on the right side represents further upside.

That means, of course, that an investor who bought back then is not yielding 2.4% today. They’re pocketing 6.2% (and climbing) on their buy instead. And that’s before we account for the 17% of the company’s float that management has bought back in that time, throwing an additional lift under the stock.

ITW, in other words, is the picture of shareholder friendliness, which makes it worth our attention now.

Deere: Buy for the Construction Boom, Stay for the Farm Revival

Deere (NYSE:) is sitting in a “sweet spot” for us to buy now.

For starters, the company, a holding my Hidden Yields service, boasts a booming construction-equipment segment, with management forecasting a 20% sales gain, plus 10% to 12% operating-margin expansion for this business, in 2026.

That’s the good news.

The drag? The segment of its agricultural business focusing on large farms, where sales slumped 14% in Q1, and management sees slipping 5% to 10% this year, according to the company’s latest earnings presentation.

But there are green shoots in these numbers, namely that corn and wheat prices have been firming up in the last few weeks, according to the two Teucrium ETFs tracking them, and management itself has said it sees now as the bottom of the ag cycle:

Corn, Wheat Prices “Plant” a Bottom

That’s a nice window for us: We never chase a boom. We buy the bottom instead. And as with ITW, we’re looking at a stock that Wall Street doesn’t understand.

Beyond that, high fuel and fertilizer costs, as well as high borrowing costs, have been squeezing farmers, but fuel costs look set to trend lower (see the oil glut mentioned above), and a decline in overall inflation should slow the rise of other costs, as well.

Meantime, as with ITW, Deere’s share price has been following the furrow plowed by its dividend—a trend I expect to continue as the ag cycle turns and global infrastructure spending (including, yes, on data centers) keeps Deere’s construction-equipment business booming:

Another High-Powered Dividend Magnet

A final upside driver for the payout? Deere’s low payout ratio, with the divvie accounting for just 47% of the last 12 months of free cash flow. That’s very manageable and lends itself to strong payout growth, especially in this “sweet spot” in the ag-growth cycle.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.