purchase of is interesting not because Berkshire noticed that the stock has worked in the past. Plenty of stocks have worked in the past. Berkshire’s investment is interesting because it implies that, at the right price, Domino’s may still have a durable economic engine capable of compounding from here.

That is the more useful question: not whether Domino’s has been a good business, but why it has compounded so much better than many public restaurant peers, and whether the source of that outperformance is structural enough to continue.

The obvious explanations only get us so far. Domino’s has a strong brand, but so do McDonald’s, Pizza Hut and . Domino’s has digital ordering, but digital ordering is no longer rare; Papa John’s also reports that approximately 85% of its domestic sales come through digital channels. Nor is the answer simply that pizza is a better category than burgers, chicken or tacos. If that were true, Pizza Hut and Papa John’s should have compounded more like Domino’s.

So the question becomes narrower and more interesting: what does Domino’s do structurally better than other restaurant systems?

My answer is that Domino’s has built one of the densest and most capital-efficient delivery networks in QSR. The company is not merely selling pizza through restaurants. It is placing pizza-making capacity close to recurring demand. That makes the store less like a traditional restaurant box and more like a local fulfillment node.

In that specific sense, Domino’s may be the closest thing QSR has to Amazon. Amazon does not maximize revenue per warehouse. It places inventory close to customers so delivery becomes faster, cheaper and more habitual. Domino’s does something similar with pizza. It places food-production capacity close enough to customers that delivery becomes faster, cheaper and more reliable.

That distinction matters because it changes how we should interpret the company’s reported metrics, especially same-store sales.

Same-store sales is useful, but not the scoreboard

Most restaurant analysis begins with same-store sales. For many concepts, that makes sense. A McDonald’s restaurant with rising same-store sales is usually becoming more productive. The restaurant itself is the main economic unit. More traffic, higher ticket, better throughput and stronger store-level margins tend to show up in the same box.

Domino’s is different. A Domino’s store is partly a restaurant, but it is also a local fulfillment node. Its job is not only to make pizza. It is to place pizza-making capacity close enough to demand that delivery is fast, reliable and cheap.

That makes same-store sales a useful number, but a dangerous primary scoreboard. For Domino’s, same-store sales is closer to revenue per Amazon warehouse than revenue per McDonald’s restaurant. It is interesting, and higher is usually better, but it does not mean the same thing.

When a Domino’s territory becomes too busy, the best answer may not be to force more sales through the existing store. The better answer may be to split the territory, add another store and shorten the delivery radius. That can depress same-store sales at the old location. But if the result is higher local system sales, shorter delivery times, better driver utilization and attractive franchisee returns, the system has improved.

The question is not whether every store can keep pushing more sales through the same box indefinitely. The question is whether the system can keep adding profitable delivery capacity while improving the customer experience.

Habit plus physical density

The Domino’s model works only if two forms of density reinforce each other. The first is habit. Customers must order often enough to create local demand. The second is physical density. Stores must be close enough to customers to deliver quickly and cheaply.

Physical density without habit is just cannibalization. Habit without physical density produces long delivery times and weak peak-hour service. The advantage appears when the two compound together.

Better ordering, value and delivery reliability make Domino’s easier to use. Easier use creates repeat habit. Repeat habit increases local order density. Higher local order density makes another store economic. Another store shortens delivery routes. Shorter routes improve speed and labor efficiency. Better speed and reliability reinforce the habit.

This is what I mean by customer productivity. Domino’s improves the productivity of a common customer job: getting an affordable meal quickly with minimal effort. The customer spends less time deciding, ordering, waiting and worrying. The app is familiar. The price is predictable. The delivery window is manageable. The product is standardized enough to travel well.

The attractive part of this model is that the same design choice can improve both cost and service. Shorter delivery routes mean the customer gets the order faster, especially during peak demand. But shorter routes also mean a driver can complete more deliveries per hour. In a labor-intensive delivery business, that matters enormously.

Many businesses must choose between lower cost and better service. Domino’s delivery density can improve both at the same time.

The evidence in the filings

The filings provide several measurable traces of this advantage.

First, Domino’s is winning the part of the pizza category where its model matters most. The company says the U.S. QSR pizza category is primarily made up of dine-in, delivery and carryout, with delivery and carryout the two largest segments. It also reports that it is the U.S. market-share leader in both delivery and carryout, with about 32.9% delivery share and 19.6% carryout share for the year ending December 2025.

That is important. Domino’s is not winning restaurants in the abstract. It is winning the specific occasions where speed, convenience, value and local fulfillment density matter most.

Second, Domino’s stores are built for this job. A Domino’s unit is not a large restaurant designed around seating, ambience and a broad in-store experience. In the U.S., it is primarily a delivery and carryout kitchen. Domino’s says many of its stores offer casual seating and allow customers to watch food preparation, but in the U.S. and many international markets they do not offer full-service dine-in; as a result, stores generally do not require expensive restaurant facilities and staffing.

That lower capital requirement changes the local decision. A franchisee does not simply ask whether one store can reach the highest possible sales number. The better question is whether two nearby stores can together generate more profit, better service and a higher return on incremental capital than one overloaded store.

A franchisee might prefer one store doing $1.2 million of sales to two stores doing $700,000 each if the second store adds too much rent, labor, equipment and management complexity. But if the second store is cheap enough to build, and if shorter routes allow drivers to serve more customers per hour, then the equation changes. The second store may add incremental profit even while reducing the reported same-store sales of the first store.

Third, the U.S. business appears highly productive even with this small-box, delivery/carryout format. Sales per store is not the most important metric for Domino’s, for the reasons already discussed, but it is still useful as a sanity check. If Domino’s had lower sales per store because it relied on small delivery nodes, the model might be less impressive. Instead, the mature U.S. system appears to generate substantial volume through those nodes.

Fourth, franchisee behavior (item 1, business) suggests the economics work. Domino’s is primarily a franchised system, with approximately 99% of global stores owned and operated by independent franchisees as of Dec. 28, 2025. In the U.S., Domino’s had 6,924 franchised stores operated by 754 independent franchisees. The average U.S. franchisee owned about nine stores and had been in the system for over 15 years.

That matters because densification requires franchisees willing to keep reinvesting. The most important vote of confidence may not come from public shareholders, but from operators who renew, open more stores and keep capital inside the system.

Papa John’s also has a commissary system and strong digital ordering. Its 2023 10-K reported that approximately 85% of domestic sales came through digital channels and that its North American franchised restaurants in the 2023 comparable base generated average annual unit sales of $1.2 million. So Domino’s is not alone in having digital ordering or centralized supply. The difference is the combination: digital demand, delivery/carryout focus, local density, lower-cost stores, supply-chain scale and franchisee reinvestment.

Domino’s corporate and its franchisees are not optimizing for precisely the same thing. Corporate benefits from higher system sales, stronger customer retention and more supply-chain volume. The franchisee must earn an adequate return on the capital and labor invested in each local node. Fortressing works only when those incentives overlap: the customer gets faster service, the franchisee earns an attractive return and corporate receives more royalty and supply-chain dollars from a larger system.

That is why the strategy is harder to copy than it looks. Opening more stores is easy. Opening more stores that improve service, preserve franchisee returns and increase total local demand is much harder.

Valuation: what am I paying for the system?I use several valuation lenses because no single metric captures Domino’s properly. Earnings multiples tell us what we pay for the current corporate profit stream. EV per store tells us what the market is paying for each node in the network. System sales per store gives a rough sense of the volume each node supports. None of these is perfect, but if several imperfect lenses point in the same direction, the conclusion becomes more useful.

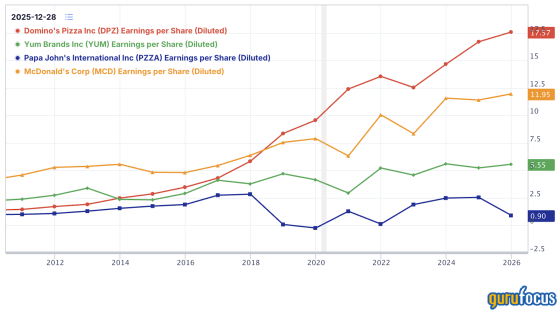

On peak earnings, Domino’s does not look expensive relative to its quality. Using rough peak earnings, Papa John’s trades at about 15 times peak per-share earnings of roughly $2.50 in 2024. Domino’s trades around 19 times peak earnings of roughly $17.50 in 2025. Yum trades closer to 29 times peak 2025 earnings.

That makes Papa John’s the obvious Graham-style candidate: a decent business with depressed 2025 earnings, a lower multiple and a plausible path to rerating. It may also have strategic value. If I were running a large QSR platform such as Yum, I would at least be thinking about whether Papa John’s could be a better pizza asset than trying to fix Pizza Hut from within.

Domino’s is different. Berkshire Hathaway’s Domino’s position is not interesting because Domino’s has already compounded well. Berkshire does not buy a business merely because the rear-view mirror looks good. The implicit question is whether the compounding engine can continue. Berkshire’s February 2026 13G/A disclosed ownership of 3.35 million Domino’s shares, representing 9.9% of the company.

A rough per-store comparison makes the trade-off clearer:

Company EV per storeSystem sales per storeComment

| Papa John’s | ~$340k | ~$0.85M | Cheaper asset, possible rerating case |

| Domino’s | ~$720k | ~$0.9M globally / ~$1.4M U.S. | Higher price, stronger delivery network |

| ~$880k | ~$1.08M | Blended KFC/Taco Bell/Pizza Hut/Habit valuation |

Domino’s is not cheap per store. Investors pay roughly twice as much for a Domino’s node as for a Papa John’s restaurant. But Domino’s also appears to generate more volume per node, especially in the mature U.S. market, and those nodes are part of a denser delivery network. That is the relevant trade-off: Papa John’s may be the cheaper asset, while Domino’s may be the better compounding system.

GuruFocus’ GF Value estimate is also above the current market price. That matters less to me as a precise target price and more as another sanity check. The earnings multiple, per-store valuation and GF Value framework all point to the same general conclusion: Domino’s is not a deep-value stock, but the market does not appear to be charging an extreme price for a superior network.

Put simply, Papa John’s may be the better cheap stock. Domino’s may be the better great business. At today’s valuation, the interesting point is that the great business does not appear to require a heroic multiple.

Owner returns: the long-term bet

The owner-return case does not require a complicated model. Domino’s has compounded both earnings per share and dividends at more than 15% annually over the past decade. The question is not whether that history was impressive. The question is whether the engine can keep producing attractive per-share growth from here.

The bet is that it can.

If Domino’s can continue growing system sales through a combination of modest same-store sales growth, unit growth, international expansion and share repurchases, then double-digit owner returns remain plausible. The current dividend yield is not the main attraction. The attraction is the possibility that per-share earnings and dividends continue to compound at high rates for many years because the system still has room to densify and replicate.

This is why the time horizon matters. A Papa John’s investment may depend more on normalization and rerating. Domino’s does not require the same near-term exit strategy. The long-term owner is making a different kind of bet: that the density advantage, franchisee economics and international runway remain intact long enough for the business to compound through cycles.

That is also why Berkshire’s involvement is relevant. Not because Berkshire is always right, and not because investors should copy the purchase blindly. It is relevant because Domino’s looks like the kind of business one could reasonably own without needing the market to reopen next month. If the model keeps working, the owner return should come primarily from business compounding, not from a quick multiple rerating.

The thesis is not that Domino’s will compound at 17% forever. The thesis is that if the structural advantages persist and the runway remains long, double-digit annual owner returns are a reasonable expectation.

Risks and runway

The main risk is confusing density with demand.

Densification is not magic. If Domino’s opens too many stores into a market where demand is not deepening, the new store merely cannibalizes the old one and adds fixed costs. That hurts franchisees and weakens the system. Domino’s itself acknowledges this risk, warning that its fortressing strategy may negatively impact sales at existing stores and could result in closures if executed too rapidly, as seen in certain international markets. The model works only if incremental habit formation supports incremental physical density.

Another risk is that the economics of delivery become more difficult. Labor, fuel and food costs can rise, and higher menu prices can pressure demand. But this risk also cuts in Domino’s favor relative to weaker competitors. If delivery becomes more expensive, route density becomes more valuable. A chain with shorter delivery radii and more deliveries per driver hour should be better positioned than a competitor serving the same market from fewer, larger nodes.

In other words, delivery inflation may hurt the category while strengthening Domino’s relative advantage inside the category. Some marginal operators may be forced to raise prices, accept lower margins or reduce service quality. Domino’s is not immune to higher absolute costs, but its dense network gives it more ways to absorb them.

A separate risk is brand damage. Brand may not be the full explanation for Domino’s compounding, but it still matters. Papa John’s is the obvious cautionary tale. A few damaging public controversies around its founder helped weaken customer perception, pressured demand and forced the company into a painful repair process. The lesson is simple: the brand may not create the whole moat, but damaging the brand can interrupt the habit formation that the moat depends on.

The domestic runway is not simply more stores. The United States is already a mature Domino’s market. The runway is continued improvement in the customer proposition: faster ordering, better loyalty, shorter delivery routes, more reliable peak-time service and more carryout convenience.

The international runway is larger but less uniform. Not every country will adopt pizza delivery and carryout with the same frequency as the U.S., U.K. or Australia. Culture, labor markets, urban density, local food habits, traffic and delivery expectations all matter. But where the habit forms, the model can last a long time. The U.S. is proof of that. Domino’s has operated there for decades, and the system is still being densified.

Conclusion

Domino’s should not be judged only by whether one store sells more pizza this quarter than it did last year.

The better question is whether the system can keep adding profitable delivery capacity while making the customer’s life easier. Same-store sales matters, but it does not define the thesis. For a delivery-first network, same-store sales can understate the economics if territory splitting leads to higher system sales, faster service and better franchisee returns.

Domino’s has outperformed because it compounds habit density and physical density together. Repeat customer demand makes low-cost delivery nodes economic. Those nodes shorten routes, improve labor efficiency, strengthen service and reinforce the customer habit.

The investment case is that this engine still has a long runway. At roughly 19 times peak earnings, Domino’s is not a classic cheap stock, but it also does not look expensive for a business that may continue compounding earnings and dividends at double-digit rates. Papa John’s may offer the cleaner rerating opportunity. Domino’s offers the better long-term compounding system.

That is why Domino’s may be the closest thing QSR has to Amazon: not because it sells everything, but because its advantage is not the individual box. It is the density and efficiency of the fulfillment network.

This content was originally published on Gurufocus.com

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.