Stocks are sky-high, but us contrarians are looking for dividend deals. And we found them in one forgotten corner of the Wall Street world. Here, we’re going to bank yields between 11% and 13%.

That’s right—up to 13%, for as little as 68 cents on the dollar.

What does that mean? Well, these funds are trading at discounts as large as 32% off their book values.

Where are we looking? We’re talking about business development companies, or BDCs. These are publicly traded firms that lend to mostly privately held companies—small and medium-sized businesses.

The BDC business itself can be a bit of a cardiac kid. It’s all about getting paid back on these loans. The smart lenders can do very well over time. The sector is so potentially lucrative that it attracts some less-than-ideal managers—hence a bit of a shady reputation.

But in these shadows is where we can find value.

2026 has been rough sledding for BDCs. There have been fears about the creditworthiness of the loans they’ve extended. It’s come to fruition—about one in four companies in the non-penny-stock BDC world have cut their dividends over the past few months.

Ugly, ugly, ugly.

So why are we diving in this dumpster for dividends? Well, we’ve got three reasons to be intrigued.

- BDCs tend to own floating-rate debt, which means their income rises as short-term rates move up. And inversely, it drops as rates drop. High oil prices have put Federal Reserve rate cuts on hold indefinitely, and this has helped stabilize BDC income.

- Even after the dividend cuts we’ve seen, BDCs still remain one of the top sources of income for dividend investors. I mean, come on—where can we find yields like these?

- Hey—these stocks are rarely this cheap. Industry valuations haven’t been this low since COVID. As contrarian investors, we are stepping in to sort through the wreckage.

So let’s talk about these dividend payers, dishing between 11.8% and 13% yields. We are looking for values here, not falling dividend knives, so these details matter.

Nuveen Churchill Direct Lending (NYSE:)

Dividend Yield: 11.8%

Investing in business development companies often means hitching our wagons to the market’s most prominent asset managers. Take, for instance, Nuveen Churchill Direct Lending Corp. (NCDL), which bears the name of both fund manager Nuveen (the asset manager for TIAA) and BDC manager Churchill, a Nuveen affiliate.

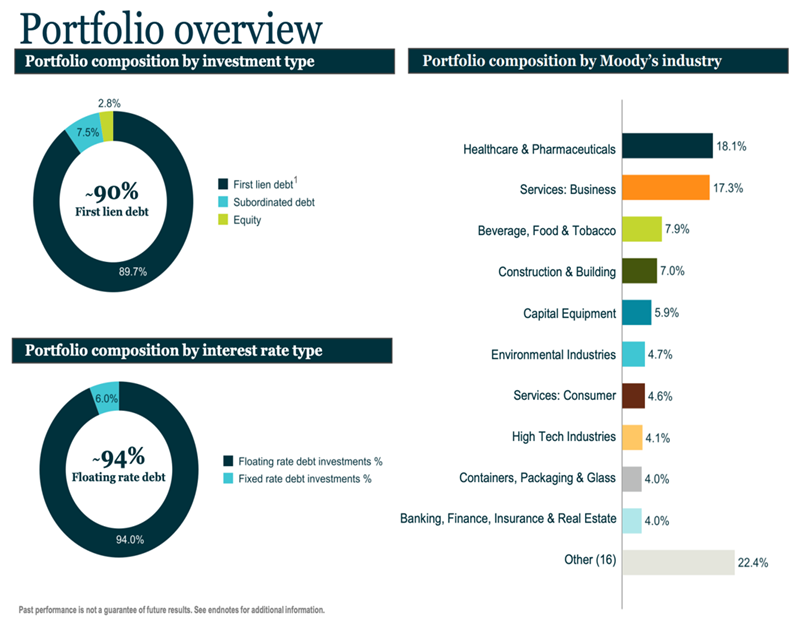

NCDL targets U.S. middle-market companies backed by private equity sponsors. It’s currently invested in 236 companies across 26 industries, with significant bents toward healthcare/pharmaceuticals and business services. It spreads out risk well, too—its top 10 holdings make up just 13% of the portfolio’s weight.

Nuveen’s BDC does most of its financing via first-lien debt, and the lion’s share of that is floating-rate in nature—helpful in that higher interest rates can boost loan income, though they can also drive down loan demand.

Source: Nuveen Churchill Direct Lending Corp. Q1 2026 Investor Presentation

Nuveen Churchill Direct Lending has less than three years’ worth of trading under its belt, most of it just pinballing up and down. And because we’re in the midst of one of its sharp downturns, we can buy it for a cavernous 26% discount to its net asset value (NAV).

But what would we be buying?

A big dividend, sure—but one that’s been quietly shrinking since NCDL first hit the market. The 45-cent quarterly with a 10-cent supplemental on top? Gone. The supplemental dried up first. Then this year, the base got cut to 36 cents, with a 4-cent top-up thrown in as a consolation. Then that supplemental shrank to 2 cents in Q2.

Death by a Thousand Trims?

What makes the underperformance and dividend difficulties surprising is that NCDL at least appears to be a solid operator. Non-accruals grew in the most recent quarter, but at just 1.3% of the portfolio at cost, so credit quality is excellent. (Non-accruals are loans that are delinquent for a prolonged period, usually 90 days.) It has a favorable fee structure thanks to waivers. Management is conservative and steeped in private-credit experience. Software exposure is low.

Patient investors might eventually be rewarded. Until then, Nuveen’s BDC clearly isn’t treating the dividend with kid gloves.

Blackstone Secured Lending Fund (NYSE:)

Dividend Yield: 12.9%

Blackstone Secured Lending Fund (BXSL) leans on the rich resources of Blackstone (NYSE:) and its Blackstone Credit & Insurance arm. And that brings up another important aspect of many BDCs: They’re not just lenders and stakeholders. BXSL’s 316 portfolio companies also enjoy the expertise and operational support of one of the world’s largest alternative credit platforms—and Blackstone Credit & Insurance doesn’t claw fees away from the BDC for the privilege.

Blackstone’s BDC deals almost entirely in floating-rate first-lien debt. It likes larger companies in sectors with historically lower default rates. It’s plenty diversified, too, with its top holdings making up less than 20% of assets.

However, while the portfolio is spread across nearly 40 industries, that top industry is a red flag.

Source: Blackstone Secured Lending Fund Q1 Earnings Presentation

BXSL took a big step back in Q1. Non-accruals jumped to 4.7% at cost, while its net asset value declined by more than 2% quarter-over-quarter.

Every other BDC seems to be hacking its dividend. Blackstone Secured Lending Fund’s has held at 77 cents. But it might just be late to the wake: Net investment income (NII) covered the payout this quarter, yet full-year 2026 and 2027 estimates are sliding toward levels that can’t sustain it.

Shares have lost 20% of their value since July 2025, which has plumped up its static dividend to a yield of nearly 13%. But deterioration in net asset value has kept BXSL from falling into deep value territory—it currently trades at a decent 9% discount to NAV.

Carlyle Secured Lending (NASDAQ:) (CGBD)

Dividend Yield: 13.0%

Carlyle Secured Lending (CGBD) is yet another double-digit-paying BDC tethered to a well-known asset manager: Carlyle Group (NASDAQ:). It invests in middle-market companies sponsored by PE. And its preferred deal type is floating-rate first-lien debt.

But CGBD stands out for a much tighter portfolio of just 60 companies. And its financing is more spread out—first-lien debt makes up less than 85% of fair value; it also has mid-single-digit exposure to second-lien debt, equity investments and investment funds.

Source: Carlyle Secured Lending Q1 Earnings Presentation

Around this time last year, I wrote that CGBD’s first half of 2025 was a “train wreck.” It had just put together back-to-back earnings disappointments, experienced rising non-accruals, and failed to issue a supplemental dividend for the first time in years.

Since then? Some ups, and some downs.

The distribution was pared down even more. After a couple quarters of keeping the dividend level, CGBD in April announced a 12.5% cut to 35 cents per share.

But the company has been putting together more promising results. While CGBD’s NAV declined by more than 2% during the first quarter, NII beat estimates, and non-accruals declined to just 1% of cost after portfolio company Alpine restructured its balance sheet. Carlyle Secured Lending also has a pair of joint ventures—Middle Market Credit Fund (MMCF) and Structured Credit Partners (SCP)—that are continuing to ramp.

When I looked at Carlyle Secured Lending in mid-2025, it had been greatly underperforming other BDCs for months. It has continued to decline since then, but its red ink has been more in line with the industry. Still, that has dragged CGBD’s price down to a 32% discount to NAV, putting this Carlyle vehicle in the cheapest third of traded BDCs.

Barings BDC (NYSE:)

Dividend Yield: 12.3%

Barings BDC (BBDC) hasn’t always been tied up with manager Barings LLC. It was known as “Triangle Capital” for many years until August 2018, when the company rebranded, trying to put years of write-offs and dividend cuts in the rear-view mirror.

It wasn’t just a brand refresh, either. The new name reflected its new relationship with global financial services firm Barings, which became an external advisor and went to work cutting out the portfolio’s rot.

Today, Barings invests primarily in middle-market companies owned by PE, though about 5%-15% of its investments are “non-sponsored” upper-middle-market and opportunistic middle-market deals, and another 5%-10% is exposure to Eclipse Business Capital and Rocade Capital—originators of middle-market first-lien loans. BBDC has the lowest exposure to first-lien debt of the group, at just 70%. Roughly 20% of its deal mix is in equity, and the rest is scattered among second-lien and mezzanine debt, as well as other financing options.

Source: Barings BDC Q1 Fixed Income Investor Presentation

We’ve already booked gains in Barings BDC twice through our Dividend Swing Trader service, so I constantly keep my eye on BBDC for short- and long-term opportunities alike.

Last year, I was encouraged by a string of small quarterly supplementals—the company hadn’t made “top-up” specials in a decade. They didn’t last, but the regular dividend has remained intact, powering a 12%-plus yield.

But that yield might have a clock on it. Earnings are pacing below the dividend, and the math only works as long as spillover earnings can bridge the gap.

One helpful development just popped up about a week ago. Barings BDC terminated a credit support agreement, which will result in a $67 million payout by the end of the month—money the company can use to fund additional investments.

And while BBDC has been a source of relative strength in 2026, down just a few percent versus double-digit declines for the BDC industry, it’s still dirt-cheap. This mega-payer currently trades at a 23% discount to NAV.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.