Coca-Cola is not without headwinds, but it is navigating them well, delivering market-beating results and driving ample cash flow.

Its Q1 earnings results highlighted its strengths, with organic sales picking up and margins improving. Among those strengths is its reliable cash flow, which underpins a healthy capital return.

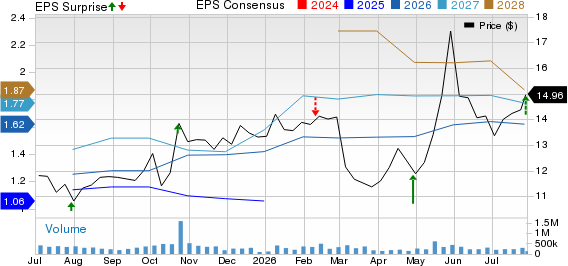

KO stock tends to trend higher over the long term, and, despite a post-earnings surge, still presents a buying opportunity in early Q2 2026. Dividends and buybacks help with leverage. The Q1 release included outperformance and margin strength, a trend likely to continue through year’s end due to consumer resilience and labor market health.

Coca-Cola Stock Trades at Value Levels in 2026

Trading below its long-term P/E average, this stock could rise by two to seven price multiples over the coming quarters and then sustain the higher valuation going forward. In addition to its position as a healthy dividend stock, it is a great diversifier in a world dominated by AI. The stock has a low beta below 0.2X, which means it can help reduce portfolio volatility while providing steady income.

Evidence of KO’s buy-and-hold quality can be seen in its institutional activity, which shows that institutional investors bought KO stock throughout the Q4 2025 and Q1 2026 tech market consolidation. MarketBeat data show that institutional investors own more than 70% of KO stock, providing solid support for its price. They have accumulated at a $2-to-$1 pace on a trailing 12-month basis, ramping activity into Q1 2026.

Q1 2026 institutional activity accelerated to about $3-to-$1, providing a strong price tailwind reflected in the chart. KO’s price action rocketed higher at the year’s start, breaking to new highs and setting a peak in March. The likely outcome for Q2 is that institutions extend the trend, as the April price pullback aligned the market with the 150-day exponential moving average, a benchmark for institutional buying.

Analysts are also aligned with KO’s uptrend in stock price. MarketBeat data shows 15 analysts rating the stock as a Buy, with a 100% Buy-side bias. The consensus price target, which has increased over the past month, quarter, and year, forecasts a double-digit upside from the critical support levels, and the trend leads to the high-end range. The high target of $90, set prior to the release, puts this market at a fresh all-time high and is likely to be surpassed by year’s end. Assuming Coca-Cola can sustain its current trends, as guidance indicates, analysts’ sentiment will remain positive.

Distribution Growth Makes KO a Great Stock for Compounding

’s capital return is central to its buy-and-hold quality. Buybacks are part of the equation, but not the driving force, as they barely offset dilution and serve more as a stabilizer than a boost for shareholder leverage. Dividends, on the other hand, are more robust. The company pays out approximately 65% of its earnings, average for a Dividend King with over 60 years of annual increases in its history, and yields about 2.7% with shares near $80. Looking ahead, the payment is reliable and likely to continue increasing at a modest single-digit pace, offsetting inflation’s impact.

Coca-Cola Moves Higher as Organic Strength Shines

Coca-Cola had a good quarter, much better than it may appear, because the growth is organic. Acquisitions are fine; they boost top- and bottom-line figures and build leverage for future growth spurts and/or business recoveries, but organic growth is best. It reflects strength in core markets and increased by 10% in Q1. Organic growth was driven by an 8% increase in concentrate sales and 2% increase in price and mix. Concentrate sales were impacted by days and timing, but that’s always a factor; this time around, the impact was favorable, and core strengths are also present.

Margin news was also good. The company widened GAAP and adjusted margin, with foreign exchange tailwinds adding hundreds of basis points to the operating income. GAAP operating income increased by 19%, adjusted operating income by 12%, with the GAAP and adjusted EPS both rising by 18%. Cash flow is another critical detail, coming in at $2 billion, with $1.8 billion in free cash flow, sufficient for management to sustain its full-year outlook. While not a robust catalyst, a sustainable cash-flow and capital-return outlook is all this market needs.

Catalysts for KO include gains in market share. The company reported gains in share across total non-alcoholic beverages and is positioned to continue gaining share over time. Key growth drivers include emerging markets in Latin America and Asia, where rapidly industrializing nations and their expanding middle classes drive consumption.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.