The biggest validation of America’s semiconductor reshoring bet just landed, and it wasn’t from Washington.

surged past $130 on Monday, hitting a fresh all-time high after The Wall Street Journal confirmed a preliminary agreement for Intel to manufacture chips for devices. The stock is up roughly 500% over the past year, and this deal explains why the rally still has legs. When the world’s most demanding chipmaker that ships over 200 million iPhones annually, decides your fabs are good enough, that’s not a trade. That’s a structural shift.

People throw around ’trade’ and ’structural shift’ like they mean the same thing. They don’t. And this situation is a good example of why that distinction actually matters.

The difference between a trade and a structural shift is the difference between buying a stock because it is moving and rebuilding your entire supply chain around someone’s industrial capability. Traders chased Intel on the government stake, on ’s investment, on Google’s partnership, and those are all events with defined shelf lives. What Apple represents is categorically different. Yes, the White House pushed for this deal, and yes, Tim Cook took that meeting. But Apple’s procurement team does not sign off on foundry agreements on that alone. They sign off when the yields pass their internal benchmarks, when the node roadmap makes sense for their silicon timeline, and when the risk of staying concentrated with one manufacturer outweighs the risk of trusting someone new.

Apple had already burned that trust with Intel once before, on processor design, and spent years building a supply chain specifically to escape that dependency. For them to come back, on manufacturing this time, means Intel’s fabs cleared a bar that most of the industry thought was still two or three years away. And that is the part that compounds. Because every other serious chip buyer watching Apple make this call now has technical and political cover to follow. The government opened the door. Intel’s 18A node had to close the deal.

The Deal That Changes Everything

The Intel-Apple agreement, hammered out over more than a year of intensive talks, represents the first meaningful crack in monopoly on Apple’s custom silicon. Apple CEO Tim Cook told analysts on the company’s most recent earnings call that iPhone 17 production had been “constrained during the quarter” because TSMC couldn’t produce enough A19 chips to meet demand. That supply bottleneck, combined with geopolitical anxiety around Taiwan, made diversification inevitable.

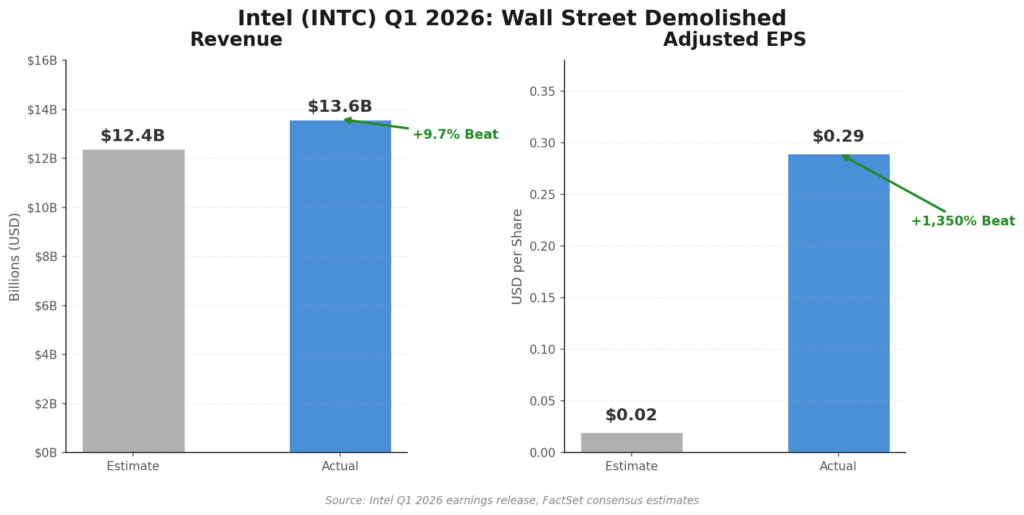

Intel CEO Lip-Bu Tan has been laser-focused on exactly this opportunity since taking over. The company’s Q1 2026 results showed the turnaround is real: revenue hit $13.6 billion, beating Wall Street’s $12.4 billion estimate by nearly 10%. The data center and AI segment grew 22%, and adjusted EPS of $0.29 demolished the consensus call of $0.02. “We are maximizing factory output and establishing AI-centric product leadership,” Tan said on the earnings call.

Q1 Results")

But the Apple deal isn’t the only vote of confidence Intel has collected. Nvidia committed $5 billion to Intel’s foundry services earlier this year. Elon Musk plans to build his $119 billion Terafab in Austin on Intel’s next-generation 14A node. and Cisco are already customers for advanced packaging. The customer pipeline is turning into a customer avalanche.

How to Play the Foundry Boom

- Intel (INTC) — ~$127, the anchor play. The stock has gone parabolic — up 240% year-to-date — and the weekly RSI is screaming overbought at 89. But here’s the thing: Bank of America just raised its price target to $96 from $56 while maintaining an Underperform rating. When your bear case is 25% below the current price and you’re still raising targets, the fundamentals are dragging analysts uphill whether they like it or not. Roth Capital upgraded to Buy with a $100 target, calling Tan’s execution “impressive.” The 14A node enters volume production in 2029, and the customer list already includes Apple, Nvidia, and Tesla. Near-term pullback risk is real given the vertical move, but the multi-year foundry thesis is just beginning.

- Apple (AAPL) — ~$291, the diversification play. AAPL hit a new all-time high above $294 last week after a monster Q2 report: $111.2 billion in revenue (+17% YoY), EPS of $2.01 (+22%), and a $100 billion buyback authorization. The INTC deal isn’t about abandoning TSMC, it’s about never being constrained again. Evercore ISI noted the Intel partnership “could add flexibility” for Apple’s supply chain, reducing single-source risk on the most critical component in every device it ships. Wedbush raised its AAPL target to $400 from $350. With a market cap above $4.3 trillion and gross margins at 49.3%, Apple can afford to dual-source and pass the cost along.

- — ~$74, the specialty foundry beneficiary. If Apple is diversifying away from TSMC concentration, the entire U.S. foundry chain benefits. GFS reported Q1 revenue of $1.634 billion with an earnings beat ($0.40 EPS vs. $0.34 expected) and guided Q2 to roughly $1.76 billion, above consensus. CEO Tim Breen highlighted 50% growth in design wins and plans to double silicon photonics revenue in 2026. The stock has nearly doubled from its 52-week low of $31.51, and Susquehanna just upgraded to Positive with a $100 price target. GFS won’t compete on leading-edge nodes, but its mature-node specialty work in automotive, aerospace, and defense gets a valuation lift when the market reprices U.S. foundry assets.

- — ~$459, the foundry competition winner. Here’s the counterintuitive angle: Intel building a credible foundry actually helps AMD. If TSMC capacity loosens even slightly because Apple shifts some volume to Intel, AMD gets better access to the leading-edge nodes it needs for its Instinct AI accelerators. Q1 revenue hit $10.25 billion (+38% YoY), with the data center segment surging 57% to $5.78 billion. CEO Lisa Su guided Q2 to $11.2 billion, roughly 46% growth. AMD doesn’t need Intel to fail for AMD to win. It needs the foundry pie to grow, and that’s exactly what’s happening.

- — ~$520, the basket approach. For investors who don’t want to pick individual foundry winners, SOXX closed at a record high last week. The ETF is up roughly 60% year-to-date and holds all the key names: MU at 8.9%, AMD at 8.7%, Broadcom at 7.4%, Intel at 6.9%, and Nvidia at 6.8%. The modified market-cap weighting caps single-stock exposure, so you get the full semiconductor cycle without concentration risk.

The Bear Case: TSMC Isn’t Going Quietly

Let’s be honest about the risks. Taiwan Semiconductor (TSM) still fabricates roughly 70% of the world’s advanced chips, and that dominance didn’t happen by accident. TSMC’s gross margins exceed 60%, and analysts project 30% sales growth in 2026. Barclays has a $470 price target. Intel’s foundry segment, by contrast, is still losing money — Q1 included a sizable net loss, and the capital spending required to compete is staggering. The 14A node won’t reach volume production until 2029, meaning Apple won’t actually receive Intel-made chips for at least two to three years.

There’s also execution risk. Intel has promised transformational process technology before and underdelivered. TSM traded lower on Monday’s news, slipping toward $401, but the decline was modest and the market isn’t pricing in a real threat to TSMC’s dominance yet. If Intel stumbles on yields or timeline, the Apple deal could end up being a headline without the revenue to match.

Also, the valuation question is legitimate. INTC has run 500% in a year. The forward P/E is near 140. BofA’s $96 raised target still implies 25% downside from where INTC trades today. Momentum can carry a stock far beyond fair value, and history says parabolic moves eventually correct. Position sizing matters here.

What to Watch

Three catalysts will determine whether the foundry trade keeps running:

May 13 — Cisco earnings. Cisco is already an INTC advanced packaging customer. Strong results and any commentary on Intel’s foundry progress could reinforce the reshoring thesis. Cisco also reports the same day as Nebius and Alibaba, making it a packed midweek session.

May 14 — earnings. AMAT is the picks-and-shovels play for every new fab being built. If Intel, TSMC, and Samsung are all spending aggressively, AMAT’s order book will show it. Guidance here serves as a real-time barometer for global foundry spending.

May 20 — Nvidia Q1 earnings. Nvidia’s $5 billion investment in Intel’s foundry validates the technology. Jensen Huang’s commentary on the Intel relationship, combined with Nvidia’s own $1 trillion AI revenue trajectory, will set the tone for the entire semiconductor complex through the summer.

The semiconductor cycle has entered a new phase. It’s no longer just about who designs the best chips, it’s about who can build them, where, and for whom. Apple just answered that question, and the answer was Intel.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.