The allure of artificial intelligence (AI) is undeniable and the tech industry sees it as a goldmine. Projections suggest that the AI market might skyrocket to over $1.8 trillion by the decade’s end with a jaw-dropping annual growth rate of 36.6%. Tech giants are thus splurging on groundbreaking technologies to grab a piece of the pie.

However, the AI landscape is fiercely competitive. The recent revelation that OpenAI, the creator of ChatGPT, anticipates $5 billion in losses despite raking in $3.7 billion in revenue serves as a stark reminder of the profitability hurdles in the AI domain.

One heavyweight diving deep into AI is none other than Microsoft (NASDAQ: MSFT). Apart from backing OpenAI, Microsoft is injecting substantial capital into infusing AI capabilities into its lineup of products and services. The looming question remains – will this investment translate into a lucrative return for the tech giant?

Microsoft’s Surging Capex Investments

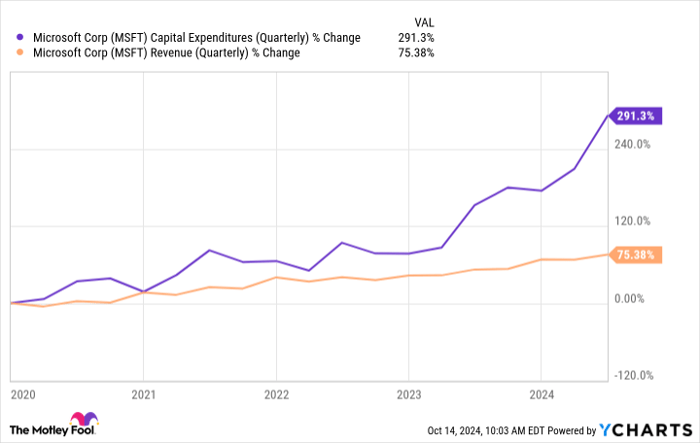

Over the past years, Microsoft’s capital expenditures (capex) have witnessed an astronomical surge. Capex represents the funds a company channels into expanding, enhancing, or upkeeping its assets, fueling long-term business growth. Notably, Microsoft’s capex spike has outpaced its revenue escalation in recent times.

MSFT Capital Expenditures (Quarterly) data by YCharts

This seemingly aggressive capex splurge should ideally sow the seeds for heightened revenue upswings in the forthcoming future.

The litmus test lies in whether this escalated investment flow paves the way for an acceleration in Microsoft’s growth trajectory.

The Perils of Blind AI Expenditure

Microsoft boasts the financial muscle to dive headlong into AI initiatives. Nonetheless, showering copious amounts of money on AI projects doesn’t guarantee a profitable outcome. With the AI market teeming with a plethora of AI-based solutions, Microsoft needs to demonstrate superiority in its offerings to trigger robust revenue growth.

CEO Marc Benioff of Salesforce likened Microsoft’s latest Copilot AI to the ill-famed Clippy of yesteryears. While Microsoft recently debuted an upgraded Copilot version, the litmus test remains in its acceptance among commercial customers and its ability to justify the $30/month per user price tag for Microsoft 365. Failure to impress could jeopardize the ROI on Microsoft’s AI investments.

Investment Prospect for Microsoft Stock

Microsoft’s stock has notched a moderate 12% uptick this year (compared to the S&P 500’s 23% surge). Investors appear to be growing wary of the stock’s valuation and the pivotal role that AI might play in propelling the company forward. Currently trading at 36 times earnings, the tech stock carries a somewhat lofty price tag, reflecting its $3.1 trillion market valuation, making it one of the world’s top-valued firms.

If you have a long-term investment horizon and are willing to weather market storms, Microsoft still presents a strong investment case. Its dominance in office software, the widely-used Windows operating system, and forays into the gaming sphere position the company favorably for sustained success. However, tepid growth in AI could fuel apprehensions among investors, leading to reluctance in paying a premium for the stock.

In due course, Microsoft is expected to navigate the AI landscape, learning from missteps and honing its approach. The company has the financial buffer to experiment, pivot, and eventually hit the jackpot. In the interim, should Copilot disappoint the market, short-term hurdles may loom, yet sustained stock appreciation is likely over the long haul.

Final Thoughts on Investing in Microsoft

Before plunging into Microsoft’s stock, it’s prudent to ponder over a few considerations:

The Motley Fool Stock Advisor team recently uncovered the top 10 stocks primed for impressive returns, with Microsoft conspicuously absent. These recommended stocks harbor the potential to yield colossal profits in the forthcoming years.

Reflect on the case of Nvidia, which featured on a similar list back in April 2005 – an investment of $1,000 at the recommendation juncture would have ballooned to a staggering $806,459*!

Stock Advisor furnishes investors with a roadmap to prosperity, proffering counsel on portfolio construction, periodic analyst insights, and two fresh stock picks monthly. Boasting more than quadrupled returns compared to the S&P 500 since 2002*.

*Stock Advisor returns as of October 14, 2024

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Microsoft and Salesforce. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.