Editor’s Note: The U.S. stock market and the InvestorPlace offices, including Customer Service, will be closed tomorrow, May 25, in observance of Memorial Day. Our regular hours will resume on Tuesday, May 26, at 9 a.m. Eastern.

Tom Yeung here with your Sunday Digest.

For centuries, Swiss cheesemakers considered the famous holes in their products as manufacturing defects. Bubbles were unsightly, made blocks hard to cut, and sometimes even caused cheese wheels to crack or explode.

We now know these holes are caused by microscopic hay particles in the cheesemaking process, and customers have come to expect them in their Swiss cheese. In fact, many makers now add powder to the cheese milk to create more holes.

The gaps have also become the basis of the “Swiss Cheese Model” of safety. Every safety check has some error rate. So, if you stack enough of these inspections together, that’s usually enough to stop most errors from getting through.

It’s why hospitals generally ask every patient to say their name and planned procedure before a major operation. Even if a patient is wearing that information on a wristband, that additional layer of “cheese” (no matter how porous) provides extra protection from mistakes.

InvestorPlace Senior Analyst Jonathan Rose and investment guru Marc Chaikin are now putting that same concept to work in investing. Over the past several months, they have been experimenting with their smart money indicators, combining them into a “Convergence Trigger” signal with exceptional back-tested results. The two systems help screen for red flags that either one may have missed.

In their upcoming presentation, on May 28 at 8 p.m. Eastern, Jonathan and Marc will show how their new system works, and how it has helped them boost results by 45% and help avoid two out of every three losing trades. They will also reveal their top five “Convergence Trigger” picks. You can sign up for their free Convergence Summit event here.

It’s the perfect time for their tools to succeed. Their indicators have historically performed best during periods of volatility, and we’re entering a market phase where instability is almost guaranteed. Rising energy prices… collapsing consumer sentiment… sky-high stock prices…

To borrow a metaphor from cheesemaking, pressure always finds the weak spots first. And this market has plenty of that building beneath the surface.

In the meantime, I’d like to showcase one of these stocks to demonstrate how this system works. And to get the other four, be sure to get on the VIP list when you reserve your spot for Jonathan and Marc’s presentation.

The Big Cheese of America’s Energy Infrastructure

Ameresco Inc. (AMRC) is a Boston area-based business that has transformed itself from a niche energy efficiency player into one of the four leading Energy Service Companies (ESCO) in America. Together with Schneider Electric SE (SBGSY), Johnson Controls International plc (JCI), and Siemens AG (SIEGY), Ameresco provides a broad range of energy infrastructure solutions for utilities and governments. This includes onsite energy generation, electricity storage, biogas, microgrids, EV charging, financing, and more.

The transformation has put Ameresco on a rapid growth path. Revenues have roughly tripled over the past decade, and profits have risen fivefold. Analysts expect around 10% sales growth and 40% earnings growth annually through 2028.

Now, Jonathan and Marc’s systems have converged and identified Ameresco as a compelling stock to buy. The company easily passes both of their “smart money” screens, and lifting the hood helps explain why.

Improving With Age

In 2020, Ameresco began building its own energy assets, rather than just constructing them for clients. For instance, the company constructed a gas plant in Houston that year to convert landfill gas into usable energy, then opened a wind farm in Ireland in May of that same year.

Today, Ameresco owns 839 megawatt electrical (MWe) of energy-producing assets, enough to power 700,000 homes. It also has another 568 MWe of assets in development. In the most recent quarter, nearly three-quarters of the company’s adjusted operating earnings came from these energy assets.

That makes Ameresco’s revenue far more stable than investors might expect from a former energy efficiency firm. The company has over $3.8 billion in revenue already booked for its energy assets – enough for two years of sales. And because more than half of its energy production comes from solar, the company stands to gain from higher fossil fuel prices as rivals’ input costs go up.

The company is also a major builder of energy projects for other entities. Ameresco has $5.3 billion of backlog in this segment, divided between the U.S. federal government (35%), municipalities and schools (29%), utilities (22%), and commercial customers, including data centers (14%).

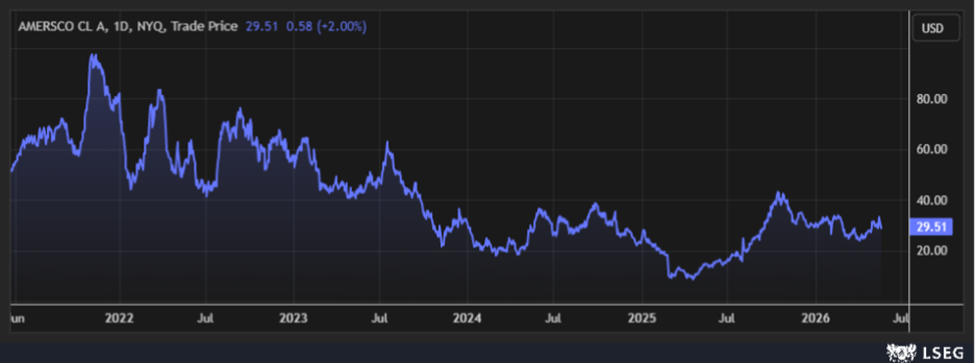

Fortunately, Ameresco’s share price has not yet caught up to its pivot. Over the past five years, shares of AMRC stock have actually fallen 43% as investors exited “clean-tech” stocks and sold Ameresco along with its former peers.

Ameresco (AMRC) stock price

Meanwhile, other energy infrastructure firms like Johnson Controls have seen shares more than double over the past five years. And the reason for this growth is something I will discuss next…

Johnson Controls (JCI) stock price

Artificial Intelligence’s Appetite

Wall Street’s sudden interest in power system builders and other power generation companies has been driven by the insatiable appetite of the AI Revolution. AI “agents” like Claude Code can use over 50 times more energy than traditional large language models, worsening an electricity shortage that’s gripping America.

Wholesale electricity prices in the core “Data Center Alley” in Northern Virginia have already risen 80% in the past five years. They will likely keep going up as AI models grow more complex.

Dominion Energy Inc. (D), the state-granted monopoly in the region, says that data centers have now requested 70,000 megawatts (MW) per day – more than three times Dominion’s all-time peak load of 24,678 MW.

Some data centers are taking matters into their own hands. In 2024, Microsoft Corp. (MSFT) signed a 20-year agreement to restart the infamous Three Mile Island nuclear power plant near Harrisburg, Pennsylvania, to power a data center. It has since made an even larger agreement with Chevron Corp. (CVX) and investment firm Engine No. 1 to build 2.5 GW of power for a West Texas location. Other companies, from Meta Platforms Inc. (META) to Alphabet Inc. (GOOGL) also are signing deals.

That’s bullish news for energy contractors, including Ameresco. Grid infrastructure companies help build power systems for AI data centers (among many other activities), and demand is rising. In September 2025, for instance, the company reached an agreement with the U.S. Navy to develop a 100 MW AI-focused data center at the Naval Air Station Lemoore, the Navy’s largest Master Jet Base, south of Fresno, California. This microgrid will include engine generators, control systems, and infrastructure upgrades.

Ameresco’s historical focus on wind and solar is also not a major hurdle. Hyperscale data center projects usually have hookups to the main grid, and renewables are a way for these major projects to gain access to the power grid. Microsoft itself plans to deliver more than 10.5 GW of renewable power capacity through a collaboration with Brookfield, an alternative asset management company.

Passing the Cheese Test

Most power-related stocks are now failing smart money screeners. NRG Energy Inc. (NRG), for instance, saw roughly $5.3 billion of sales by two major holders, a bearish sign. Constellation Energy Corp. (CEG) flipped from “Bullish” in Marc’s system to “Very Bearish” in 2025, where it remains today.

Constellation Energy (CEG) Chaikin Power Gauge Rating

That’s because power stocks tend to trade more like stable income investments than growth companies. Smart money will typically sell on the upswing to avoid the eventual reversion.

Fundamental screeners are also turning negative on many utility stocks. Earnings quality is falling, input costs are rising, and profits are on the decline. NRG, for instance, is expected to report net income margins of 4.88% this year, down from 5.23% last year.

Fortunately, Ameresco passes these screens. Insiders have largely avoided open-market sales in the past six months, and earnings per share are expected to rise 26% this year and 56% the next as the company reaches scale. As I mentioned earlier, the company’s focus on renewables also shields it from rising fossil fuel prices.

That makes Ameresco an unusually attractive play in an industry lacking good options. The company is still growing, and it’s riding one of the most powerful investment waves of our generation. Below is a five-year price chart of the stock, which you can see was negatively rated by Marc’s system until it started a recovery in August, 2025.

Ameresco (AMRC) Chaikin Power Gauge Rating

And so, I highly encourage you to watch Jonathan and Marc’s free presentation on May 28 at 8 p.m. Eastern, where they will go into more detail about how their system works, how it can help you screen for other promising stocks, and what their other four top “Convergence Trigger” picks are.

Sign up for the Convergence Summit event by clicking here.

Until next week,

Thomas Yeung, CFA

Market Analyst, InvestorPlace

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.