The performance of electric vehicle stocks has varied in recent times. While Tesla (NASDAQ:TSLA) has witnessed significant growth, with a surge of 137%, Lucid Group (NASDAQ:LCID) has faced a decline of 30%. This divergence highlights the competitive nature of the EV industry and the imperative to discern long-term winners. Bolstered by favorable global EV adoption prospects, certain companies have the potential to thrive and create value in the coming decade.

Here are seven electric vehicle stocks, whose potential growth and innovation make them worthy holdings until 2030.

Tesla (TSLA)

Tesla has defied skeptics and emerged as a significant value generator. Given the global growth opportunity in the EV sector, TSLA stock has the potential for substantial multifold returns from current levels. This cements its position as one of the premier electric vehicle stocks to hold until 2030.

One of the key reasons for optimism surrounding Tesla is its steadfast commitment to innovation. The company has dedicated $2.9 billion to research and development in the first nine months of 2023. This emphasis on R&D is poised to maintain Tesla’s competitive edge within the industry.

Additionally, Tesla boasts strong brand appeal and operates with lower marketing expenses compared to traditional automakers and other EV firms. This has enabled the company to generate robust cash flows, with operating cash flow totaling $8.9 billion in the first nine months of 2023. With a substantial cash reserve of $26 billion as of September, Tesla is well-positioned to execute its ambitious global expansion plans, which may include establishing multiple new factories. Notably, the upcoming launches of Cybertruck and Roadster are anticipated to be significant growth drivers in the near future.

Li Auto (LI)

Li Auto (NASDAQ:LI) has registered a robust 64% year-to-date uptrend, underpinned by increasing deliveries and expanding free cash flows. The company’s strategic focus on the Chinese market and its endeavors to enhance market share in various cities positions it as one of the top Chinese EV enterprises.

Of note, Li Auto is intensifying its presence in both tier one and tier two cities in China, where it currently commands a 50% market share in the well-developed SUV market segment priced above RMB300,000. As it continues to expand its retail footprint and introduce new vehicle models, Li Auto is expected to further bolster its market share, including in third-tier cities, thereby propelling its growth trajectory.

Moreover, the company’s investments in R&D, aimed at developing autonomous driving technology, signify its long-term growth vision. Supported by a robust cash position of $12.13 billion as of Q3 and strong cash flows, Li Auto has the flexibility to pursue innovation and product development

Panasonic Holdings (PCRFY)

Among EV battery companies, Panasonic Holdings (OTCMKTS:PCRFY) emerges as an attractive investment proposition for multiple reasons. The stock trades at a compelling forward price-to-earnings (P/E) ratio of 8 and offers a dividend yield of 2.3%, underpinning its investment appeal.

Further, the company has outlined ambitious growth plans through 2031, entailing the establishment of multiple new facilities to ramp up EV battery production capacity. The overarching goal is to quadruple the production capacity to 200GWh compared to the previous financial year. This strategic initiative is poised to translate into robust revenue and cash flow upsurge.

With a revenue target of 2.5 trillion yen by the financial year 2031, coupled with an improved EBITDA margin, Panasonic is also focused on enhancing battery density and developing solid-state batteries for drones, slated for commercialization by 2029. These concerted efforts bolster the investment case for PCRFY stock, with the potential for substantial returns in the long run.

Albemarle Corporation (ALB)

While renowned as a global specialty chemicals provider, Albemarle Corporation (NYSE:ALB) stands out as a key beneficiary of the burgeoning demand for lithium, propelled by the EV industry’s growth trajectory. Trading at an attractive forward P/E of 7, ALB stock presents a compelling investment opportunity.

The company’s lithium conversion capacity is projected to increase from 200ktpa in 2022 to 600ktpa by 2027. This expansion, combined with an anticipated upswing in lithium prices, positions Albemarle for robust revenue growth and heightened cash flow potential.

Furthermore, with a formidable balance sheet, Albemarle is actively considering potential acquisitions as part of its growth strategy, presenting a potential catalyst for value creation in the long haul.

3 Undervalued Stocks That Could Surge by 2030

Lithium Americas (NYSE:LAC) is another lithium stock that looks massively undervalued. Considering the asset base, I believe that LAC stock can potentially deliver 10x returns by 2030.

Lithium Americas (LAC)

The potential of Lithium Americas is nothing short of formidable. The company holds 100% interest in the Thacker Pass project in the United States, which features the largest measured and indicated lithium resource in the country, boasting an after-tax net present value of $5.7 billion. Needless to say, the current market valuation of Lithium Americas at $1 billion seems unjustly paltry.

Adding to its allure, General Motors (NYSE:GM) is investing $650 million in the project. GM also holds an 100% offtake agreement for phase one production for 10 years. With such extraordinary developments, it’s just a matter of time before LAC stock skyrockets.

Blink Charging (BLNK)

Blink Charging (NASDAQ:BLNK) stands out as a promising contender in the realm of EV charging infrastructure. The company has seen an 18% surge in its stock over the past month, and this bullish momentum is expected to persist.

One compelling reason to remain bullish is the company’s projected achievement of positive EBITDA by December 2024. Additionally, Blink reported a staggering 152% year-on-year revenue growth to $43.4 million for Q3 2023, having sold or deployed 5965 chargers.

In the coming quarters, the emergence of fast DC chargers is poised to significantly impact the revenue mix. Furthermore, Blink Charging’s low capex investment related to L2 installation diminishes operational costs substantially, affording the company a competitive edge in offering services at a lower cost.

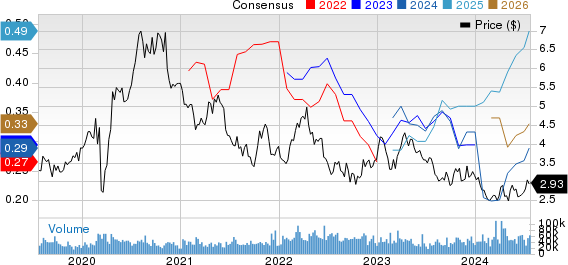

Solid Power (SLDP)

Solid Power (NASDAQ:SLDP) serves as a compelling choice in the realm of penny electric vehicle stocks, despite the associated risks. If the company can successfully commercialize solid-state batteries, it stands to deliver multibagger returns from its current levels of $1.5.

Notably, Solid Power has made its first A-1 EV cell deliveries to BMW (OTCMKTS:BMWYY), marking its formal entry into automotive qualification. Ford (NYSE:F) is also an investor and automotive partner. The potential validation from these automotive giants is likely to catapult SLDP stock to higher echelons.

With a cash buffer of $422 million, the company’s strong financial position alleviates concerns of equity dilution for the foreseeable 12 to 18 months, instilling a sense of confidence in its long-term prospects.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.