What the Market Missed

has returned roughly $400 to $500 million to shareholders every year for the past five years, combining buybacks with a quarterly dividend now running at $0.60 per share. Against a current market capitalization of approximately $5.7 billion, that capital return represents a 7 to 8% yield before any growth in the underlying businesses. The company runs both VITAS Healthcare, the nation’s largest hospice provider with more than 22,700 patients in daily care, and Roto-Rooter, the nation’s largest commercial and residential plumbing network, with no long-term debt.

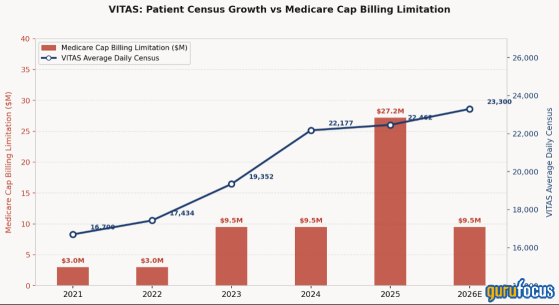

What brought the stock from $581 to $424 across the past twelve months was not a deterioration in either franchise. In 2025, VITAS accrued $27.2 million in Medicare Cap billing limitations, the majority concentrated in Florida, versus roughly $9.5 million in each of the two prior years. The difference was an arithmetic mismatch: Florida reimbursement rates grew at 5.2% while the per-beneficiary cap ceiling grew at only 2.9%. Management resolved it by shifting admissions toward hospital-referred patients with shorter stays. The Q1 2026 results confirmed the fix: VITAS accrued only $2.4 million in Medicare Cap for the quarter, tracking well below the $9.5 million full-year estimate. Admissions grew 6.9%. ADC reached 22,723, up 2.2%. Management raised full-year VITAS ADC growth guidance to 4.5 to 5.5%, up from the original 3.5 to 4.0%, and raised revenue growth guidance excluding Medicare Cap to 6.5 to 7.5%, up from 5.5 to 6.5%.

The second disruption is Roto-Rooter, where the adjusted EBITDA margin fell to 22.5% in Q1 2026 from a historical range of 27 to 29%. Two causes account for the gap: a permanent shift in customer acquisition from organic search to paid digital leads, and elevated write-offs in the water restoration business from insurance carrier scrutiny. These are discussed in detail below, but the short version is that the paid lead cost increase is structural rather than cyclical, and the right way to model Roto-Rooter’s future contribution is at the revised margin guidance of 21.5 to 22.5%, not at the historical 27 to 29%.

The combined effect of VITAS’s acceleration and Roto-Rooter’s margin pressure produced a raised 2026 adjusted EPS guidance of $24.00 to $24.75, up from the original $23.25 to $24.25. The midpoint of $24.375 implies approximately 13% growth over 2025’s $21.55. At $424 per share, the owner is paying 17.4 times the raised midpoint. The stock traded at 24.4 times on average over the past five years. Whether the current discount is justified depends on the answer to one question: is Roto-Rooter’s margin decline permanent enough to offset VITAS’s secular growth? The rest of the article addresses that directly.

The Hospice Architecture

Hospice care in the United States is funded almost entirely by the Medicare Hospice Benefit, a daily reimbursement structure established in 1983 that pays providers for every calendar day a patient receives care. The rate is set by CMS annually and escalates with the inpatient hospital market basket: for fiscal 2026, beginning October 1, 2025, CMS finalized a 2.6% payment update, adding an estimated $750 million in total hospice payments across the industry. At VITAS’s scale, caring for more than 22,000 patients daily, that 2.6% rate increase applies to a daily revenue base of approximately $4.8 million and compounds persistently without requiring additional capital expenditure or competitive repositioning.

VITAS became the largest single-source hospice provider in the United States by doing something the industry has found surprisingly difficult to replicate: focusing exclusively on hospice and scaling it with the operational rigor that scale demands. Nearly 12,000 VITAS professionals delivered care to more than 92,000 patients across 15 states and the District of Columbia during 2025. The average daily census grew from approximately 16,700 in 2021 to 22,462 in the fourth quarter of 2025. That growth is structural rather than episodic; it reflects an aging American population, a hospice utilization rate that remains below its theoretical maximum as referral patterns from hospital systems and nursing facilities continue to mature, and VITAS’s own de novo and acquisition strategy expanding into underpenetrated geographies.

The Medicare Cap mechanism is widely misunderstood and deserves a precise explanation for an owner thinking about 2026 and beyond. Each Medicare-certified hospice provider operates under a statutory aggregate billing limitation: for the government fiscal year 2026, the cap amount is $35,361.44 per beneficiary served. Providers whose total Medicare billings for a given program exceed this cap multiplied by the number of beneficiaries admitted must refund the difference. The problem that emerged in VITAS’s Florida programs in 2025 was not excessive care costs or poor clinical performance. It was a rate differential: the Florida programs saw reimbursement rates increase approximately 5.2%, while the per-beneficiary cap ceiling increased only 2.9% for the same period. That 2.3-point mismatch mechanically increased the cap exposure even as census and revenue were growing. Management resolved it by temporarily shifting the admissions mix toward hospital-referred patients, who typically have shorter care durations and therefore generate fewer days of reimbursement per beneficiary. As of the fourth quarter of 2025, the Florida exposure had been effectively neutralized.

The cost of that strategy is visible in the near-term numbers. A higher proportion of short-stay patients produces less revenue per patient episode and compresses adjusted EBITDA margins, because the fixed cost of a nursing and support team does not scale proportionally with episode length. VITAS’s adjusted EBITDA margin, excluding Medicare Cap, was 21.7% in the fourth quarter of 2025, below the 22 to 24% range that longer-stay patient mix supports. The 2026 narrative for VITAS is the mirror image: hospital-based admissions taper from their artificially elevated share, longer-stay patients re-enter the census mix, and per-patient revenue per episode expands. Management guides 2026 VITAS ADC growth at 3.5 to 4.0% and revenue growth of 5.5 to 6.5% before Medicare Cap.

The Plumbing Franchise

If VITAS is the secular compounder with a temporary billing arithmetic problem, Roto-Rooter is the durable franchise with a cyclical margin issue. The business operates 123 company-owned branch locations and 328 franchise locations across North America, making it the largest commercial and residential plumbing and drain cleaning network in the country. Residential customers represent approximately 71% of branch revenues. The service is overwhelmingly nondiscretionary: a burst pipe, a blocked drain, a sewage backup. These are not calls that customers defer when sentiment softens.

Revenue trends through 2024 and into 2025 reflected real pressure. Housing turnover slowed as elevated mortgage rates kept existing homeowners in place and curtailed the moving activity that historically drives peak demand for plumbing services. Water damage restoration, a higher-revenue segment within the residential business, came under pressure from insurance carriers tightening documentation requirements, leading to elevated write-offs as billed revenue was challenged and reversed. In the fourth quarter of 2025, water restoration write-offs increased by approximately $4 million, or 57%, over the prior-year quarter, accounting for the bulk of the margin deterioration in isolation.

The lead acquisition structure is the second pressure point, and it carries a structural dimension worth examining carefully. Roto-Rooter built its residential demand base around a combination of brand awareness and organic search prominence. As Google’s algorithm changes and private equity-backed competitors with aggressive digital marketing budgets entered the market, natural search traffic declined and paid leads became a proportionally larger share of call volume. Paid leads carry materially higher customer acquisition costs than organic ones, directly compressing gross margin per job. Management acknowledges this is a competitive development rather than a temporary fluctuation, and the response is operational: tighter field discounting controls, higher approval thresholds for price concessions, and an internet-focused marketing campaign targeting residential plumbing. Residential branch plumbing revenue responded, growing 6.3% year over year in the fourth quarter of 2025. Commercial branch revenue is also recovering, with excavation up 10.9% and drain cleaning up 2% in the same period.

The honest assessment of Roto-Rooter’s margin trajectory requires separating what is cyclical from what is not. The water restoration write-off issue is cyclical: insurance carriers tighten documentation standards periodically, claims resolution backlogs clear, and the revenue per job eventually normalizes. Management’s centralized collection initiative is already addressing this. The lead cost shift is structural. Private equity-backed competitors have permanently raised the cost of acquiring a residential plumbing customer through digital channels, and Roto-Rooter’s organic search advantage has eroded in a way that a marketing campaign can mitigate but is unlikely to reverse. At a gross margin of 51% in Q1 2026, the business is still healthy at the job level. The margin compression is above the gross line, in selling and marketing costs that now run several hundred basis points higher than they did three years ago. Management lowered full-year 2026 adjusted EBITDA margin guidance to 21.5 to 22.5% from the original 22.5 to 23.0%, reflecting this reality. A return to the historical 27 to 29% range would require either a collapse in competitor marketing spend or a structural rebuild of Roto-Rooter’s organic search presence, neither of which is a near-term probability. The right base case for an owner modeling this business over the next five years is a margin range of 22 to 24%, roughly 400 basis points below the historical average. On Roto-Rooter’s 2026 revenue guidance of approximately $990 million, the difference between 22% and 27% adjusted EBITDA margins is approximately $50 million, or roughly $2.70 per diluted share after tax. That is the cost of the structural shift in lead economics, and it is already reflected in the current price.

Capital Return Record

Chemed’s capital return history is the clearest expression of management’s confidence in the combined franchise. Since the repurchase program’s inception, the company has returned more than $2.9 billion to shareholders through buybacks at an average cost of approximately $167 per share. The current price near $395 means that long-term shareholders who participated through the program’s full history have seen extraordinary per-share value creation from the reduction in share count alone.

The most recent activity tells a specific story. In Q4 2025, management repurchased 400,000 shares at $436.39 each, deploying $174.6 million. In Q1 2026, the pace accelerated: 500,000 shares for $197.7 million. Total buyback authorization remaining at March 31, 2026, was approximately $229.6 million. The board added $300 million to the program on February 13, 2026, before Q4 results were released, knowing the numbers would be unfavorable. From an owner’s perspective, the current price is actually more attractive for buybacks than the Q4 average: every share retired at $424 is accretive relative to the $436.39 at which management was buying three months earlier. In Buffett’s framing, an owner should prefer the stock not to re-rate quickly so long as management continues retiring shares at these levels. At a $5.7 billion market cap and $400 to $500 million in annual capital returns, the share count declines by 3 to 4% per year at today’s price. That is a compounding mechanism that works regardless of what the multiple does.

The dividend record adds a further layer of institutional commitment. Chemed has paid 219 consecutive quarterly dividends across 54 years as a public company. The quarterly dividend was raised 20% from $0.50 to $0.60 per share in August 2025, a period when VITAS’s Medicare Cap pressures were already fully visible to management. A company that raises its dividend by 20% into a year where it subsequently misses earnings guidance is making a statement about its view of normalized earning power that differs substantially from how the market is currently pricing the stock. The annualized dividend of $2.40 represents a yield near 0.6% at the current price, and the payout ratio of approximately 11% of adjusted earnings leaves the majority of free cash flow available for buybacks.

At What Price

At approximately $424 per share, against the raised midpoint of 2026 guidance of $24.375 in adjusted diluted EPS, the owner pays roughly 17.4 times forward earnings. The earnings yield is 5.7%. Free cash flow in 2025 was $388.3 million; at a similar conversion rate on the midpoint of 2026 guidance, free cash flow reaches approximately $330 million, or a 5.8% yield on the current market cap of $5.7 billion.

The owner-return framework is more useful than a multiple comparison. Over the past five years, Chemed has returned $400 to $500 million annually through buybacks and dividends. At the current price, that rate of return reduces the share count by 3 to 4% per year. VITAS’s raised guidance of 6.5 to 7.5% revenue growth excluding Medicare Cap adds mid-single-digit organic growth on the roughly 65% of consolidated earnings VITAS represents. Roto-Rooter, at the revised 21.5 to 22.5% margin guidance, contributes modest revenue growth on the remaining 35%. The combined effect, before any multiple change, is an annual owner return in the range of 10 to 13%: approximately 5.7% earnings yield, 3 to 4% from share count reduction, and 2 to 3% from underlying earnings growth at VITAS’s secular pace.

CompanyFwd P/EDebt/EquityFCF Yieldvs 5-Yr Avg P/E

| Chemed Corporation | ~17.4x | 0x | ~5.8% | -29% |

| Ensign Group | ~26.5x | ~1.0x | ~2.4% | +12% |

| Healthcare Svcs Median | ~17.5x | varies | ~3-4% | n/a |

Chemed trades at 17.4 times, below the healthcare services median and at a 29% discount to its own five-year average, despite no long-term debt and $2.9 billion returned through buybacks at an average cost of $167 per share. Ensign Group, which operates in a related but more capital-intensive segment of post-acute care, trades at 26.5 times with a leveraged balance sheet. The discount Chemed carries is explained almost entirely by the Roto-Rooter margin compression. The question is whether a 400-basis-point structural decline in one segment’s margins, on a business that represents roughly 35% of consolidated earnings, justifies a 29% discount to the company’s own historical valuation on the remaining 65% that is accelerating. At today’s price, an owner does not need the multiple to expand. The capital return and organic growth do the work. If the multiple does normalize, it is an additional return on top of a mid-teens compounding base.

Institutional Conviction

AQR Capital Management holds 326,000 shares valued at approximately $139 million, the largest hedge fund position visible in the ownership data, accumulated at an average cost of $481.80. Cliff Asness’s systematic firm added 89% to its position during a period when the stock fell from $580 to $395, expressing a model-based conviction about the earnings stream independent of near-term sentiment. Joel Greenblatt (Trades, Portfolio)’s Gotham Asset Management added 38% at an average cost of $475. Millennium Management increased its position by 72% at $507.35. Mario Gabelli (Trades, Portfolio)’s Gamco Investors, with an average cost of $115.14 representing a gain of more than 200%, added another 9.4% in the most recent period after holding through decades of appreciation. Moore Capital and Mangrove Partners both initiated new positions.

The pattern is straightforward: long-duration investors with substantial gains have not exited, and quantitative capital has been building exposure through the drawdown. At $424 after the Q1 earnings beat, every major holder in the register bought at prices above or below the current level and held. That does not guarantee a positive outcome, but it describes the quality of capital on the other side of the selling that drove the stock from $581 to $384 and back.

Risks

The Medicare Cap mechanism is less predictable than its current resolution might imply. The 2025 exposure in Florida emerged from a specific rate differential that was not anticipated in the company’s initial 2025 guidance. If a similar differential recurs in 2026 or subsequent years, a problem that management considers resolved could reappear. The same certificate-of-need strategy that helped mitigate Florida in 2026 may not be replicable in every market where VITAS operates, and the company’s growing scale means that even a smaller relative cap exposure translates into larger absolute billing limitation amounts. VITAS’s California programs also contributed to the 2025 cap, and the dynamics there are separate from the Florida resolution.

Reimbursement policy risk is structural and persistent for any hospice operator. The Medicare Hospice Benefit has been largely stable since its establishment, but fiscal pressure on the federal healthcare budget is a recurring feature of the policy environment. Any meaningful reduction in reimbursement rates, tightening of eligibility criteria, or changes to the cap calculation methodology would directly reduce VITAS’s revenue per patient day without a corresponding reduction in clinical costs. The 2.6% rate increase for fiscal 2026 is within the normal historical range and CMS has shown no immediate intent toward structural change, but a long-term owner should price this as a low-probability, high-magnitude tail risk.

Roto-Rooter’s lead economics represent the more immediate concern. Private equity capital has entered the residential plumbing services market with resources for digital marketing that traditional franchise models find difficult to match. The shift from organic to paid leads is a permanent cost increase unless Roto-Rooter rebuilds organic search standing, which is a multi-year effort with uncertain outcomes. If margins settle structurally in the low-to-mid twenties rather than recovering toward the high twenties, the contribution from that segment to consolidated earnings is permanently lower than historical norms suggest, and the 2026 guidance would represent a ceiling rather than an interim step. Management does not believe this is the case, but the data remains inconclusive.

Finally, the owner math at $424 is simpler than the narrative makes it sound. VITAS provides hospice care to 22,700 patients daily, funded by Medicare at rates that increase 2.6% annually, with admissions growing 6.9% and guidance raised across every metric. Roto-Rooter clears blocked drains and repairs broken pipes, services that are nondiscretionary, at margins that have been permanently compressed by roughly 400 basis points due to structural changes in lead acquisition costs. The combined business generates $400 to $500 million in annual free cash flow against no long-term debt, returns all of it substantially, and is guided to earn $24.00 to $24.75 per share in 2026.

At 17.4 times the raised midpoint, the stock trades 29% below its own five-year average. An owner at today’s price earns a 5.7% yield, plus 3 to 4% annually from share count reduction, plus mid-single-digit growth from VITAS’s secular expansion. That is a 10 to 13% annualized return before any change in how the market prices the business. A management team that bought back shares at $436 in Q4, accelerated to $197.7 million in Q1 at lower prices, and then raised guidance, is not behaving as though the business is impaired. The next checkpoint is Q2 2026 results in late July, where VITAS ADC trends and Roto-Rooter margin stabilization will confirm whether the raised guidance holds.

This content was originally published on Gurufocus.com

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.