Expensive Price Tag on Microsoft Stock

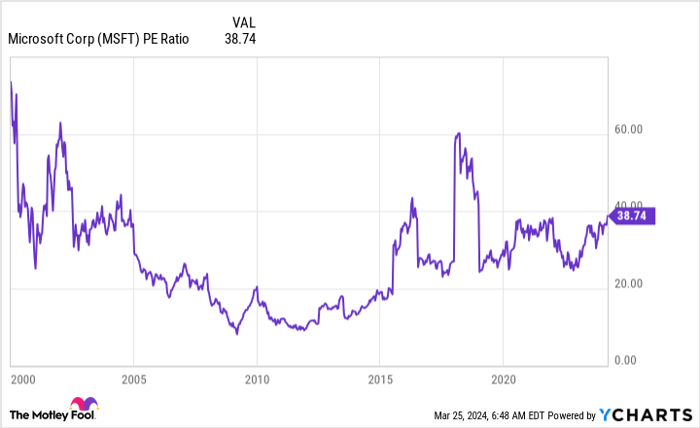

Microsoft, currently the largest company globally with the NASDAQ ticker symbol (MSFT), is raising eyebrows with its price-to-earnings ratio of 39. This red flag could signal caution for investors as they navigate the market landscape.

The warning sign illuminating for Microsoft’s stock predominantly revolves around its valuation. Trading at almost 39 times earnings, this marks Microsoft’s highest valuation (excluding outliers from early 2000s) in several years.

The spike in Microsoft’s valuation stems from its ventures into artificial intelligence (AI) and its success in that domain. The company’s adeptness in leveraging AI technologies, especially within its digital assistants, demonstrates commendable execution. Microsoft has seamlessly integrated AI features into its products, notably offering Co-pilot for Microsoft 365 at a reasonable $30 per month with an annual commitment.

Further contributing to Microsoft’s valuation surge is its collaboration with OpenAI and ChatGPT product, renowned as a leading generative AI model. Microsoft’s cloud computing wing, Azure, has outpaced competitors, growing at 30% year over year in the latest quarter versus 26% for Google Cloud and 13% for Amazon Web Services, hinting at Azure potentially outshining Amazon in the cloud computing arena.

Amid its product successes, the market has bestowed a premium on Microsoft stock. Yet, the snag lies in the forward earnings estimates not significantly trimming the stock’s lofty valuation.

Risks of Microsoft’s Premium Valuation on Broader Market

Assessing a company’s value through the forward price-to-earnings (P/E) ratio proves more insightful for businesses navigating a swiftly transforming landscape. Utilizing analysts’ earnings forecasts for the upcoming year, this metric aids in fairly pricing stocks.

Microsoft’s forward P/E, lagging slightly behind its trailing P/E, hints at restrained growth prospects sighted by Wall Street analysts. Notably, Nvidia, despite phenomenal growth metrics, trades at 38 times forward earnings compared to 80 times trailing earnings.

To sustain investor satisfaction, Microsoft must uphold its rapid growth trajectory. Analysts project around 6% revenue growth for the upcoming quarter, followed by 6.4% for FY 2024 ending June 30, and a subsequent 14% growth the following year.

If Microsoft falters in meeting investor expectations and its stock depreciates, the broader market could endure repercussions. Given Microsoft’s substantial weightage in the S&P 500 at roughly 7%, a dip in Microsoft’s stock price could influence the index negatively, impacting countless investors with S&P 500 holdings.

Furthermore, a decline in Microsoft’s performance may hint at economic challenges impeding a myriad of other firms. Microsoft’s software solutions serve as foundational productivity tools for global enterprises. A drop in demand for its offerings could signify a slowdown in businesses worldwide, possibly sparking a larger market downturn.

Investors with stakes in Microsoft should approach with caution. While the company shows promise, its current overvaluation poses a conundrum, potentially posing obstacles for the broader market. As the market prices in massive AI demand for Microsoft, any deviations from this trajectory could pose significant hurdles.

While Microsoft stands as a stalwart business, its sky-high expectations reflected in the stock price forecast challenging investment prospects over the upcoming years. Considering other stocks like Nvidia showing stronger growth, alternative investment avenues might offer better returns.

Investing your faith in Microsoft’s continued success, growing moderately (or surpassing the norm), albeit excessively priced, could complicate profiting over the next few years.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.