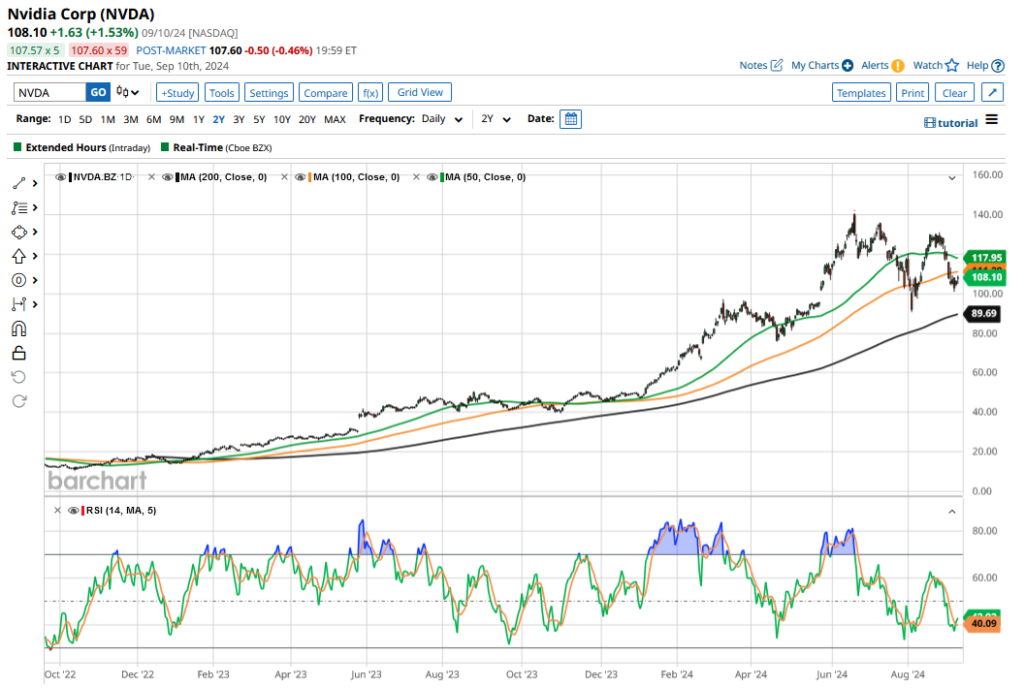

Even though Nvidia (NVDA) has experienced a retreat from its peak, it remains a strong player in the financial markets, boasting a remarkable 119% surge in value over the year. This has positioned it as the standout performer within the esteemed S&P 500 Index ($SPX). Despite recent stagnation, characterized by tight price fluctuations since its zenith in June, which mirrors Nvidia’s tendency towards volatility, all eyes are on the potential trajectory of this technology frontrunner. In this piece, we delve into the perils and prospects confronting the Nvidia-led by the visionary Jensen Huang. The primary question on investors’ minds is whether the stock has the mettle to resurrect to its historic highs.

The defining obstacle for Nvidia, starkly outlined by its recent earnings report, is the burden of sky-high expectations weighing heavy on its prospects. Despite exceeding analyst projections for fiscal Q2 2025 and delivering a promising guidance, investor reaction was subdued, reflecting the market’s insatiable anticipation for an even grander performance.

Key Risks That Nvidia Investors Should Watch Out For

Several risks loom on the horizon for Nvidia investors:

- Revenue concentration: In fiscal Q2 2025, almost half of Nvidia’s revenue was attributed to its top four clients. Adding to the peril, these prominent customers, labeled as “hyperscalers,” are embarking on crafting their custom AI chips.

- A severe slowdown or a recession: Although the likelihood remains low, a drastic economic deceleration could curb the expansive AI investments by tech juggernauts, thus dampening the demand for Nvidia’s AI chips.

- Chip breakthrough: Nvidia’s dominance in the AI chip sector faces a formidable challenge posed by a potential breakthrough from a U.S. or Chinese competitor. Any emerging competition in this space could not only impact Nvidia’s revenue streams but also erode its robust gross margins.

- Antitrust concerns: U.S. regulators are increasingly scrutinizing Nvidia’s commanding presence in the AI chip realm. The specter of antitrust action, spurred by the intensified focus on monopolistic practices, poses a significant threat to the company.

- Geopolitical risks: Nvidia stands vulnerable to heightened geopolitical tensions, particularly in the context of the potential resurgence of stringent policies under former President Donald Trump, whose tough stance on China could disrupt Nvidia’s significant market presence in the region.

The Demand for NVDA’s AI Chips Is Broadening

Despite the prevailing challenges, Nvidia is poised to capitalize on several key opportunities on the horizon. During the fiscal Q2 earnings call, Nvidia’s CEO Jensen Huang exuded optimism about the data center landscape, anticipating GPUs to supplant CPUs across these facilities. The company also assuaged concerns regarding its clients’ return on investment in Nvidia’s AI chips.

Moreover, with AI investments extending beyond the initial adopters, a broadening demand portfolio emerges, encompassing enterprises and even sovereign entities according to Goldman Sachs semiconductor analyst Toshiya Hari.

Furthermore, Nvidia represents a strategic investment vehicle intertwined with multiple high-growth sectors, including gaming, the metaverse, blockchain, and autonomous driving. While these avenues hold promise, Nvidia’s AI chip sales reign supreme at present.

Will Nvidia Stock Rebound?

Market analysts anticipate a resurgence in Nvidia stock, with a mean target price of $149.22 denoting a 38% upside potential from the current valuation. The lofty Street-high target price of $200 forecasts an 85% premium, coupled with a unanimous “Strong Buy” rating from analysts.

Pundits project Nvidia to report an adjusted EPS of approximately $4 in the upcoming fiscal year concluding in January. Given the current stock price, this implies a credible FY 2026 price-to-earnings (P/E) multiple of 27x, an appetizing prospect in light of the robust 40% earnings growth expected in the ensuing fiscal year following a stellar 120% surge this year.

Although the allure of a premium tech entity like Nvidia sporting a PE-to-growth (PEG) ratio of less than 1 is compelling, market apprehensions linger regarding its sustained AI chip sales at lucrative margins post-2026, especially as hyperscalers potentially curtail their capital expenditures.

While Nvidia’s recent performance has been subdued, there is a silver lining as the company transitions into behaving more akin to a conventional stock, liberating itself from single-handedly propelling the AI euphoria. In light of this evolution, investors should recalibrate their expectations towards more moderated returns from NVDA stock moving forward.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.