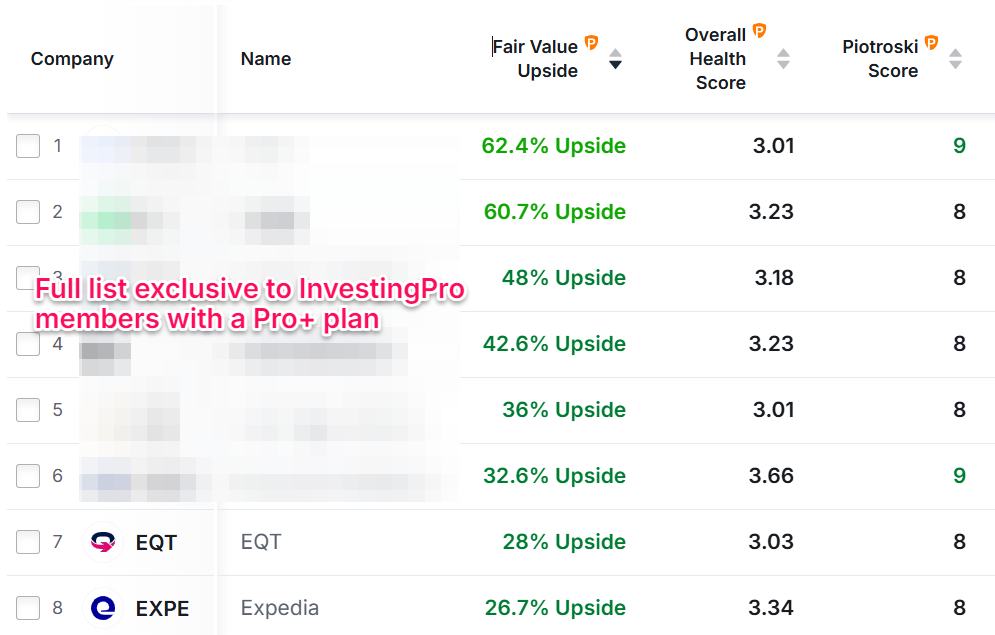

Key Points

-

Nvidia may be willing to give up some share of the computing layer if it can keep NVLink at the center of the AI system.

-

Marvell’s strategic value may come from its ability to help customers build custom chips and connectivity for both NVLink and UALink.

-

As AI clusters grow, moving data becomes a larger bottleneck, increasing demand for Marvell’s electrical and optical interconnect technologies.

- 10 stocks we like better than Marvell Technology ›

Imagine AT&T joined a coalition building an alternative to Verizon‘s network. Then Verizon invested $2 billion in AT&T. After that, Verizon asked AT&T to make its devices and network infrastructure compatible with Verizon’s network, too.

That sounds strange. Why invest in a company helping build an alternative to your own network? A version of that relationship is now taking shape in artificial intelligence.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a “Double Down” signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same “Total Conviction” signal is flashing for a company 1/100th the size of Nvidia. Continue »

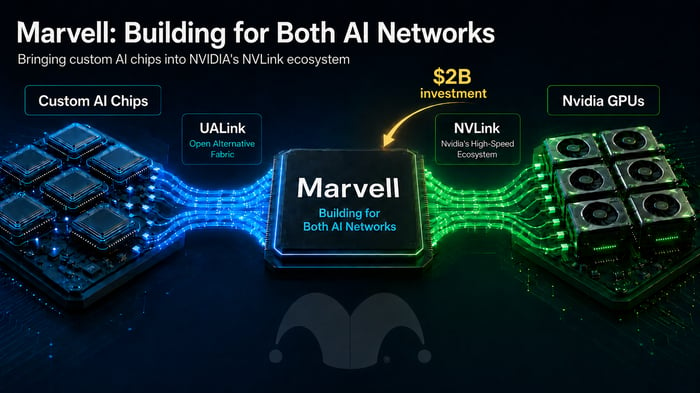

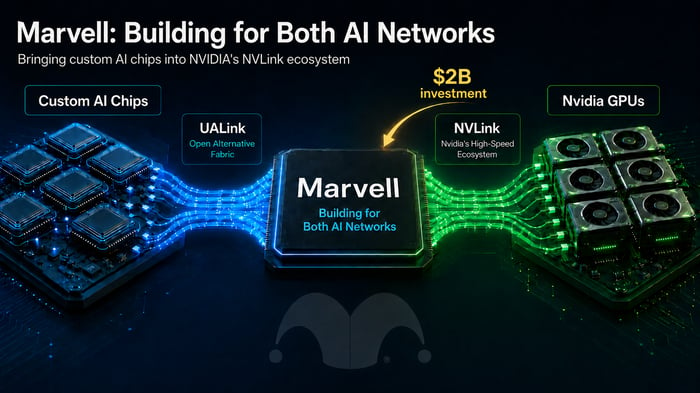

Marvell Technology (NASDAQ: MRVL) supports UALink, an open interconnect standard designed to give AI chipmakers an alternative to Nvidia‘s (NASDAQ: NVDA) proprietary NVLink fabric. Marvell has developed technology that can help customers build custom accelerators, switches, and scale-up networks around the standard.

Then, in March 2026, Nvidia invested $2 billion in Marvell. The companies also announced a strategic partnership covering custom AI chips, NVLink Fusion-compatible networking, optical interconnects, and silicon photonics.

Marvell was helping customers build for an alternative network. Now Nvidia is investing to make sure Marvell can build for its network, too. So has Marvell abandoned UALink? There is no public indication that it has.

The more interesting possibility is that Marvell is becoming valuable because it can build for both sides.

Image source: The Motley Fool.

Nvidia Is Changing What It Means to Win

Nvidia built its position in AI around a tightly integrated platform. Its GPUs perform the computing. NVLink connects those GPUs inside large systems. Nvidia’s networking equipment moves data across racks and data centers. Its software helps customers operate the entire architecture. Each layer makes the others more valuable.

But hyperscalers want more control. Companies such as Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) Meta (NASDAQ: META), and Microsoft (NASDAQ: MSFT) are developing custom chips for workloads where a specialized processor may cost less, consume less power, or perform a specific task more efficiently than a standard GPU.

Those chips can reduce their dependence on Nvidia.

Nvidia could treat every custom accelerator as a threat. Instead, NVLink Fusion gives the company another way to participate. The technology allows custom CPUs and accelerators to connect to Nvidia’s NVLink fabric and rack-scale architecture. Nvidia may not manufacture every processor in the system, but it can still provide the network that allows those processors to work together.

That is the bargain. Nvidia gives customers more freedom at the computing layer. In return, it gets another chance to keep NVLink at the center of the system.

Put more simply: Nvidia may be willing to give up some compute share if NVLink remains the fabric connecting the system.

Marvell Can Sell Customers Either Path

This strategy makes Marvell unusually useful. Marvell helps hyperscalers design custom silicon. It also develops the technologies needed to connect that silicon, including high-speed electrical interfaces, switches, copper connectivity, optical signal processors, and silicon photonics.

Marvell’s advantage is not any single component. It can help design the processor, choose the fabric, and connect the finished system.

Customers can now take at least two paths. One path uses UALink, an open scale-up interconnect supported by a coalition seeking an alternative to Nvidia’s proprietary fabric. The other connects custom chips to Nvidia’s ecosystem through NVLink Fusion.

Supporting Nvidia does not require Marvell to stop supporting UALink. Its business is helping customers build the architecture they choose.

One hyperscaler may prefer UALink for greater openness and supplier flexibility. Another may choose NVLink because Nvidia already has a mature software, networking, and rack-scale ecosystem. A large customer could use both for different workloads.

Marvell benefits as long as customers need custom processors and the connectivity required to make them work. Nvidia’s investment may therefore be less about breaking the UALink coalition and more about preventing custom silicon from automatically pushing customers outside Nvidia’s ecosystem.

Before NVLink Fusion, choosing a custom accelerator could also mean choosing another scale-up fabric. Now those decisions can be separated. A customer can choose a non-Nvidia processor without necessarily giving up Nvidia’s interconnect. Marvell helps make that possible.

AI’s Bottleneck Is Expanding Beyond the GPU

The partnership is happening because the technical problem inside AI data centers is changing.

The first stage of the AI boom centered on computing power. Companies needed more accelerators to train larger models and serve more users. But adding more processors creates another bottleneck. Those processors must constantly exchange data.

As AI systems grow from individual servers into racks containing dozens of accelerators, and eventually into clusters containing hundreds of thousands of chips, moving information becomes almost as important as processing it.

A fast accelerator cannot deliver its full performance if it spends too much time waiting for data from another chip. The system needs more than powerful processors. It needs higher bandwidth, lower latency, cleaner signals, and lower power consumption across every connection.

This is where networking stops being a supporting component and becomes part of the computing architecture itself.

Copper Still Works, but It Needs More Help

Copper does not suddenly stop working at 1.6 terabits per second. Marvell’s own products demonstrate that.

Its Alaska A 1.6T digital signal processor sits inside an active electrical cable and cleans up the signal as it travels. The chip carries eight lanes running at 200 gigabits per second each. Marvell says the technology allows copper connections to reach beyond three meters inside an AI rack.

But the solution also reveals copper’s trade-off. At higher speeds, moving an electrical signal farther requires additional silicon to retime, reconstruct, and correct the data. That adds power, cost, and complexity.

Source: www.barchart.com

Source: www.barchart.com  Source: www.barchart.com #2. Amazon: The Stealthy AI Powerhouse

Source: www.barchart.com #2. Amazon: The Stealthy AI Powerhouse  Source: www.barchart.com

Source: www.barchart.com  Source: www.barchart.com Unveiling the Resilience of Baidu in the Chinese Tech Landscape The Resilience of Baidu in the Chinese Tech Space

Source: www.barchart.com Unveiling the Resilience of Baidu in the Chinese Tech Landscape The Resilience of Baidu in the Chinese Tech SpaceCopper remains attractive across the shortest connections. Passive copper can provide low latency and low power when chips sit close together. Active electrical cables extend that reach by adding signal processing.

Optics becomes more practical as the distance grows. Optical modules convert electrical data into light, send that light through fiber, then recover and correct the signal at the other end. Fiber can carry enormous amounts of data over greater distances with less signal degradation than copper.

The future will not be entirely copper or entirely optical. Copper will remain important inside racks. Optics will move closer to the processors as AI systems require more bandwidth across racks, rows, buildings, and data center campuses. Marvell supplies technology for both.

Rubin Raises the Networking Stakes

The problem becomes more important as Nvidia moves into the Rubin generation. Rubin is not simply a faster GPU.

More computing power means more traffic moving among processors, memory, switches, and storage. Each increase in computing density puts greater pressure on the surrounding network.

The GPU can improve, but the rest of the system has to keep up. That creates demand for technologies Marvell has spent years developing. Its SerDes technology sends and receives high-speed electrical signals between chips. Its switches direct traffic through the network. Its optical DSPs prepare and recover data traveling through fiber. Its custom-silicon business helps customers design processors around specific workloads.

These products solve different parts of the same problem: keeping an increasingly large AI system operating as one coordinated machine. For Marvell, Rubin is more than another Nvidia product cycle. It expands the connectivity problem Marvell is positioned to solve.

It also explains why Nvidia might want Marvell closer. Nvidia’s future performance depends partly on technologies outside the GPU. A faster processor cannot deliver its full value if networking, signal integrity, or power consumption becomes the limiting factor.

Polariton Is a Bet on the Next Optical Limit

Marvell is already preparing for another increase in optical speeds. In April 2026, the company acquired Polariton Technologies, a developer of plasmonics-based modulation technology.

A modulator turns electrical data into changes in light that can travel through an optical connection. As data rates rise, conventional optical components face harder trade-offs involving bandwidth, size, signal quality, and power consumption.

Marvell says Polariton’s technology can advance its optical roadmap toward 3.2T connections and beyond. The acquisition does not guarantee commercial success. Promising photonics technology still has to move from technical demonstrations into reliable, economical, high-volume manufacturing. Competitors are investing in other approaches. Adoption may take longer than investors expect.

But the strategic logic is clear. AI systems will need more bandwidth. Optics will need to move closer to the processors. Power efficiency will become more important. Marvell is buying technology aimed at those constraints before the market fully arrives.

The $2 Billion Is a Strategic Signal, Not Proof

Nvidia’s investment gives this relationship more weight than an ordinary supplier agreement. Nvidia is committing capital to a company that helps hyperscalers develop custom processors and supports a competing scale-up interconnect.

That suggests Nvidia sees strategic value in Marvell’s position across the market. But investors should not treat the investment as proof that Marvell will win.

Technical importance does not automatically create attractive economics. Custom-chip design wins can take years to enter production. Large customers can divide projects among several suppliers or bring more work in-house.

Marvell also faces formidable competition. Broadcom has deep custom-silicon relationships and a broad networking portfolio. Nvidia continues developing more of the surrounding infrastructure itself. Other suppliers are investing heavily in switches, connectivity, and optical technologies.

Marvell still has to convert its engineering position into durable revenue, margins, and cash flow.

Marvell May Be More Valuable Because It Has Not Chosen a Side

The easy interpretation is that Nvidia’s investment brings Marvell into Nvidia’s camp. That may be too simple. Marvell can help customers build custom chips that reduce their reliance on Nvidia GPUs. It can support an open fabric such as UALink. It can also connect custom processors to Nvidia’s NVLink ecosystem.

Its value may come from not belonging entirely to either side. As AI infrastructure becomes more modular, the boundaries between processors, fabrics, switches, copper links, and optical connections become more difficult to manage.

Marvell is positioning itself at those boundaries. Nvidia’s $2 billion investment suggests those boundaries are becoming strategically important. The investment question is whether Marvell can turn that position into lasting economics. If it can, its opportunity will not depend on defeating Nvidia or abandoning UALink.

It will come from becoming one of the companies that both sides need to build the next generation of AI infrastructure.

Should you buy stock in Marvell Technology right now?

Before you buy stock in Marvell Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Marvell Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $396,542!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,299,961!*

Now, it’s worth noting Stock Advisor’s total average return is 931% — a market-crushing outperformance compared to 210% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of July 15, 2026.

Beegee Alop has positions in Alphabet, Amazon, Broadcom, Meta Platforms, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Broadcom, Marvell Technology, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Verizon Communications. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.