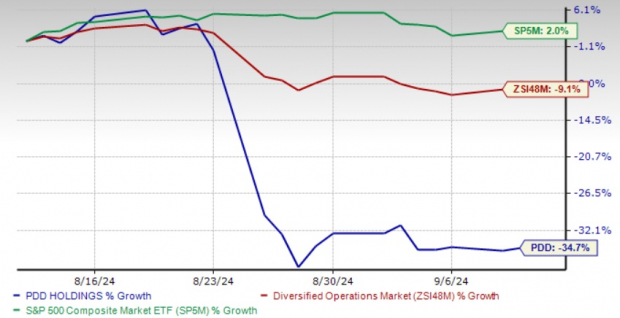

What a whirlwind ride for investors in Pinduoduo (NASDAQ: PDD) this week. Despite an astounding 86% surge in revenue during the latest quarter, the e-commerce powerhouse watched its stock plummet by over 30%. But is the landscape truly as bleak as it seems? Let’s dissect this further.

Image source: Getty Images.

The Rise of Pinduoduo: An Unprecedented Journey

Pinduoduo’s trajectory in the Chinese tech realm over the past decade has been nothing short of remarkable. From its humble beginnings in 2015, the company swiftly ascended to challenge giants like Alibaba and JD.com. By 2023, Pinduoduo was a revenue behemoth, raking in $34.9 billion with a net profit of $8.5 billion.

Despite its massive scale, Pinduoduo sustained high double- to triple-digit growth rates in recent quarters. The company’s revenue skyrocketed by 86% to $13.4 billion in the second quarter of 2024, with net profit more than doubling to $4.4 billion. A burgeoning domestic business coupled with the foray into cross-border e-commerce via Temu fueled this growth.

Pinduoduo’s unwavering dedication to ecosystem enhancement, superior services, and customer value retention has cemented its position in the market. Moreover, the firm leveraged operational efficiency, with fixed costs rising at a slower pace compared to its revenue surge.

It’s noteworthy that despite rapid expansion, Pinduoduo managed to shore up a substantial (and growing) cash reserve. By Q2 of 2024, the company boasted $39.2 billion in cash, cash equivalents, and short-term investments, alongside minimal debt, showcasing a rare blend of expansion, profitability, and financial fortitude.

Management’s Gloomy Outlook Amidst Growth

While many enterprises strive to accentuate their successes and veil their weaknesses, Pinduoduo adopts a candid approach. The latest quarter saw the tech titan not only cautioning about fluctuations in the future but also shedding light on imminent challenges.

Lei Chen, Pinduoduo’s chairman and co-CEO, emphasized the hurdles ahead in the earnings release, despite a staggering 144% surge in net profit. Mentioning fierce competition, substantial ecosystem investments, and an anticipated profitability dip, Chen painted a realistic picture: sustained growth will be arduous, and profitability might wane. Similarly, the uncertain and competitive landscape obscured hopes that Temu could preserve Pinduoduo’s hypergrowth trajectory.

Further denting investor confidence was management’s veto on returning capital through dividends or share buybacks in the near term. This stance likely spurred an exodus from the stock.

Implications for Stakeholders

Pinduoduo’s stratospheric rise has rendered it a colossus rivaling Alibaba. Nonetheless, the sheer magnitude could impede future growth, as perpetual 86% leaps are unsustainable.

Yet, a ray of hope gleams as Pinduoduo acknowledges this and endeavors to sustain its growth engine. Invested in ecosystem development, merchant support, and trust enhancement, these initiatives, though costly, may foster sustainable progress in the long haul.

Should You Dive into PDD Holdings Now?

Before plunging into PDD Holdings shares, take heed:

The Motley Fool Stock Advisor analysts, renowned for spotting potential winners, bypassed PDD Holdings in their 10 best stocks to buy. These elite selections harbor the promise of monumental returns in the foreseeable future.

Consider the case of Nvidia’s inclusion in 2005; an investment of $1,000 then would have burgeoned to $630,099, underscoring the potential with diligently chosen stocks.

The Stock Advisor service, a beacon for investors, outperformed the S&P 500 by over fourfold since 2002, guiding with precision on building a diversified portfolio and providing monthly stock picks.

Explore the 10 stocks unearthed by their discerning eye.

*Stock Advisor returns reflect data up to September 3, 2024.