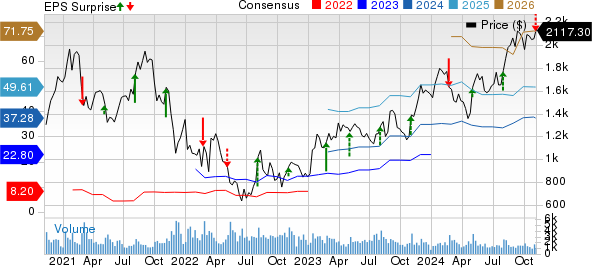

Warner Bros. Discovery’s Struggle Amidst Sector Growth

Warner Bros. Discovery (WBD) finds itself in a quagmire this year. With shares plummeting 27.6% year to date, the entertainment giant is trailing behind not just its peers like Netflix, Fox, and Roku but also the broader Consumer Discretionary sector’s performance. The uphill battle can be attributed to a myriad of factors, including a 7.1% year-over-year dip in revenues in the first half of 2024.

Recent sluggishness in the linear advertising market in the US, renewed sports and affiliate rights uncertainties, and an impaired relationship between market capitalization and book value have all contributed to the downtrend. Warner Bros. Discovery is grappling with a decline in ad sales and distribution revenues, further exacerbated by challenges in specific international markets and its exit from the AT&T SportsNet business.

Adapting to Changing Dynamics

Despite the setbacks, Warner Bros. Discovery is not throwing in the towel. The company is focusing on expanding its presence across various platforms, such as Hulu and Sling TV, to enhance overall traffic. There is optimism surrounding the surge in viewership of non-fictional content on Discovery+, promising a silver lining amidst the gloom.

Warner Bros. Discovery is actively striving to boost its financial health by enhancing subscriber-related trends, fostering stronger engagement, delivering personalized content, and maintaining a tight grip on expenses. These measures are deemed crucial for the company’s potential recovery.

Strategic Partnerships and Operational Insights

The strategic partnerships Warner Bros. Discovery has forged, including agreements with Esports World Cup Foundation, SF Studios, and Stan Sport, are seen as sources of growth stimulation. The recently inked deal with Charter Communication, the largest Pay-TV distributor in the US, is particularly noteworthy.

By securing an agreement with Charter, Warner Bros. Discovery is set to counterbalance the loss of the NBA partnership. The collaboration entails an increment in broadcast fees paid by Charter and grants its customers access to Warner Bros. Discovery’s streaming platforms like Max and Discovery+ at no extra cost. This move aims to tap into Charter’s extensive customer base – a prudent step in boosting subscriber revenues and delivering tailored content.

Furthermore, Warner Bros. Discovery is eyeing global expansion by taking its channel, Max, to a broader market. Currently accessible in 65 international markets, plans are underway to introduce Max to new territories within the next 18 to 24 months. Operational optimization, including restructuring initiatives and facility consolidation, is on the agenda to achieve cost efficiency.

Forecasting Challenges and Opportunities

While estimates for 2024 paint a somewhat bleak picture with a projected year-over-year revenue decline and wider loss per share, there are signs of optimism. Growth in third-quarter 2024 earnings and revenues hints at potential recovery.

Investors stand at a crossroads when evaluating whether to buy, hold, or sell Warner Bros. Discovery shares. The company’s prospects are as alluring as they are daunting, with a Value Score of B underlining undervaluation. A Zacks Rank #3 (Hold) advises a cautious approach, possibly waiting for a more favorable entry point.