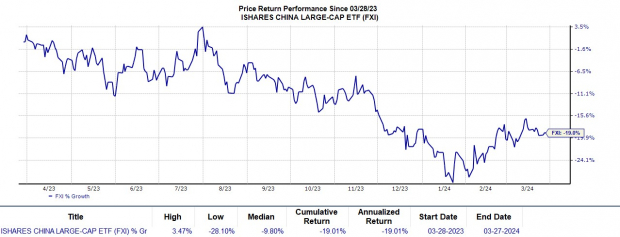

The Impact of Trump's Policies on the Magnificent Seven StocksTrump's Potential Impact on the Magnificent Seven CompaniesIn the annals of American history, only one former president has managed to secure reelection after losing the first term - Grover Cleveland in 1892, a solitary figure in this political parable. Fast forward to the present, where former President Donald Trump is in a neck-and-neck race with Vice President Kamala Harris for the 2024 presidential throne. Should Trump emerge victorious, his policy decisions could cast a long shadow on the fortunes of the revered "Magnificent Seven" companies that include tech behemoths like Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. An intriguing narrative unfolds as investors weigh their options in this high-stakes drama.

Former President Donald Trump. Image source: Official White House Photo by Shealah Craighead.

Assessing Trump's Proposals and Their RamificationsA trio of Trump's propositions loom large over the future of the Magnificent Seven, with his corporate tax cut scheme taking center stage. If re-elected, Trump vows to slice the federal corporate tax rate from the current 21% to a paltry 15%, a move that could recalibrate the financial landscape for these titans of industry. Tariffs are another cornerstone of his economic blueprint, with up to 20% levies on imports and a spotlight on China evident in his rhetoric. Moreover, Trump's zeal for deregulation, epitomized by a promise to scrap onerous rules at a 10:1 ratio against new regulations, could create seismic shifts, especially around artificial intelligence governance.

Forecasting the Corporate Weather for the Magnificent SevenWhile a reduced tax burden might sound like sweet music to the ears of the Magnificent Seven, a deeper dive reveals a nuanced backdrop. Unveiling the effective tax rates paid by these giants in the last fiscal year paints a revealing picture. Alphabet, Amazon, Apple, Meta Platforms, Microsoft, and Nvidia all operate below the current 21% threshold, with Tesla even benefiting from a 50% tax boon, making the tax cut impact a mixed bag of fortunes.

Trump's tariff barrage could rattle the foundations of reliant companies, stirring debates on cost pass-through to consumers and the resultant sales pendulum. Apple's global supply chain stands vulnerable to the tariff storm, though players like Alphabet and Meta, deriving significant revenue from services, might weather the storm better.

The shadow of deregulation could sway fortunes in the cloudy skies of AI governance. Amazon, Microsoft, Alphabet, Nvidia, and to a lesser extent, Meta and Tesla, stand to gain from relaxed regulations, shaping a turbulent yet potentially rewarding horizon.

Trump's pointed criticism of Alphabet and Meta, juxtaposed with his favorable stance towards Microsoft and Nvidia, sets the stage for a strategic showdown where winners and losers are yet to emerge from the fog of political warfare.

Identifying the Ripest Pick among the Magnificent SevenAs the curtain rises on the looming political drama, the quest for the choicest investment amidst the Magnificent Seven intensifies. Microsoft and Nvidia emerge as prime contenders in this investment battleground. While Microsoft could reap the fruits of Trump's tax cuts due to its high tax rate and navigate the tariff headwinds, Nvidia's growth potential offers a tantalizing allure, promising the elixir of prosperity beyond the mirage of political turbulence. In the tumultuous landscape of Trumpian economics, the astute investor's choice between these icons could unfold as a pivotal journey towards prosperity.

Investment Insights: Assessing the Timing of Lucrative Opportunities Investment Insights: Assessing the Timing of Lucrative Opportunities