Let’s talk about big dividend payers that are seeing strong buying from insiders.

Yes, we’re talking about the big boss slapping down their own money for shares nobody is forcing them to buy—shares they may already have plenty of.

Why do we like buying as a signal? Insiders can sell for a variety of reasons:

- A new divorce

- A new boat

- A higher burn rate

- Kids off to college

There are many reasons an insider may sell for the cash. But there’s only one reason they buy: they believe the shares are going up.

Today, we have stock indices near all-time highs. By and large, the market looks pricey. But these big bosses are saying, “Oh no—these shares of the company I run happen to be cheap, and I am slapping down my own ‘hard-earned’ money to do it.”

When these fat cats happen to run big dividend payers, I like this strategy best because they are investing as we do, exchanging cash today for passive income streams tomorrow. And we’ve got a few gushers! I’m talking divvies from 5.1% all the way up to 11.3%…

RLI Corp (NYSE:)

Dividend Yield: 5.1%

Recent Noteworthy Buys:

- President and CEO Craig Kliethermes: 2,000 shares ($104,000) on 5/27/26

- Chief Operating Officer Jennifer Klobnak: 2,000 shares ($105,440) on 5/27/26

- Director David Duclos: 2,500 shares ($129,975) on 5/28/26

- Director Clark Kellogg: 3,000 shares ($152,700) on 6/1/26

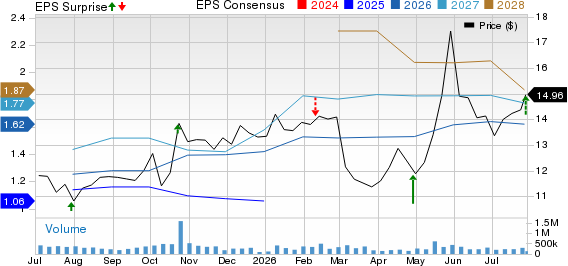

Let’s start with Illinois-headquartered RLI Corp. (RLI), a specialty insurer that provides business insurance, personal insurance and surety bonds, among other products.

RLI is in the throes of a deep bear market dating back to November 2024. Shares have lost 40% of their value not amid any meaningful drop in its operational results—2025 operating earnings and net earnings were both better than they were in 2024—but a sharp decline in what investors appear to be willing to pay for the stock. Shares that went for nearly 5 times book 18 months ago now trade for almost half that.

Numerous insiders started exercising options and making non-open-market purchases in May shortly after the stock bottomed. Kliethermes and Klobnak kicked things off with about $367,000 worth of purchases mid-month. More recently, they and two other directors—including Clark Kellogg of Ohio State Buckeyes, Indiana Pacers and broadcasting fame—have bought almost half a million dollars’ worth of shares.

RLI Insider Buying Picks Up the Pace

Their buying coincides with a lot of shifts in the business. RLI is an elite underwriter, boasting 30 consecutive years of underwriting income. But property rates, especially in catastrophe-prone areas, are worsening. It’s instead trying to capitalize on improving rates in commercial auto liability and personal umbrella—and it’s shifting that latter book of business away from the coasts and toward the Midwest.

These insiders are also buying a prolific dividend grower. RLI is a Dividend King, boasting 51 consecutive years of increases to its quarterly dividend. But the regular payout itself is small, only amounting to about 1.3% in annual yield—it substantially bolsters that with a yearly supplemental dividend that pushes its yield north of 5%.

LTC Properties (NYSE:)

Dividend Yield: 6.2%

Recent Noteworthy Buys:

- Executive VP, Chief Investment Officer Dave Boitano: 10,000 shares ($346,900) on 06/04/26

LTC Properties is a real estate investment trust, or REIT, that owns senior housing and skilled nursing properties. It’s also a historically low-drama stock featuring low beta—and thus low volatility—and it’s a monthly dividend payer to boot.

The company has spent the past couple of years shifting its portfolio toward REIT Investment Diversification and Empowerment Act (RIDEA)-structured contracts. Within this structure, LTC owns the assets outright and either manages the property or hires a third-party manager.

In 2024, triple-net-lease (NNN) senior housing—in which tenants are responsible for various expenses, LTC just collects rent—accounted for 54% of the portfolio’s asset value, and skilled nursing made up the rest.

However, thanks to aggressive acquisitions and converting some of its own tenants, the company expects its “SHOP” (senior housing operating portfolio) to make up the greatest percentage (45%) of gross asset value this year; NNN senior housing will make up 32%, and skilled nursing will drop to less than a quarter.

This move has stabilized shares following a sharp drawback across 2022 and 2023. But when shares dropped in early June along with the rest of the REIT sector, CIO Dave Boitano took advantage for his third 10,000-share direct purchase in roughly a year’s time.

Yet Again, Boitano Bought on the Dip

Buying the dips also helps Boitano earn better yields on his LTC shares—and that’s really the only way he’ll sweeten that income in the foreseeable future. LTC’s dividend hasn’t grown in roughly a decade.

American Assets Trust (NYSE:)

Dividend Yield: 5.6%

Recent Noteworthy Buys:

- Executive Chairman Ernest Rady: 10,000 shares ($234,000) on 6/1/26

- Executive Chairman Ernest Rady: 10,000 shares ($246,400) on 6/10/26

- Executive Chairman Ernest Rady: 10,000 shares ($246,200) on 6/11/26

- Executive Chairman Ernest Rady: 10,000 shares ($246,300) on 6/12/26

- Executive Chairman Ernest Rady: 10,000 shares ($242,100) on 6/15/26

American Assets Trust (AAT) is a hybrid REIT that operates 31 buildings across the Pacific Coast, Hawaii and Texas. Those buildings include 4.3 million square feet of office space, 2.4 million square feet of retail space, 2,302 multifamily units, and 369 hotel suites.

Earlier this year, I wrote about potential contrarian plays among Wall Street’s Sell calls. That included American Assets Trust, which has gone on to rip 30% higher year-to-date. The analyst community is still frigid on AAT shares, but founder, former CEO and current Executive Chairman Ernest Rady can’t get enough of his company’s stock.

Ernest has bought roughly 50,000 shares over the past two weeks, and 769,000 shares across all of 2026. He’s stacked that stock on top of the several million shares he had previously purchased for a number of trusts and other vehicles he has direct control over.

Ernest Goes to Buy More AAT

Wall Street, to its credit, has (and still has) plenty of reason to give AAT the side-eye. It has had some vacancy issues, and FFO growth is virtually nonexistent.

The dividend—which has fallen below the 6% mark—looks safe at around 70% of FFO. But it’s paying enough to make it difficult for American Assets Trust to pursue growth opportunities. Management said earlier this year it might sell off its mixed-use assets just to buy more multifamily or retail buildings. A dividend cut is not out of the question.

But there are signs that AAT’s operating environment is improving. And CEO Adam Wyll pointed out that the REIT entered Q2 with 244,000 square feet of previously signed leases that haven’t yet commenced, as well as a proposal pipeline of 200,000—good news for its occupancy issues.

TXO Partners LP (NYSE:)

Distribution Yield: 11.3%

Recent Noteworthy Buys:

- Director, Chairman of the Board Bob Simpson: 369,153 shares ($5,134,918) on 6/3/26

- Director, Chairman of the Board Bob Simpson: 230,847 shares ($3,095,658) on 6/2/26

Bob Simpson has been backing up the truck.

Bob is the founder, director and board chairman of TXO Partners LP (TXO), an independent oil and natural gas company that has roughly 1.3 million gross acres across three premier oil-and-gas basins: the Permian (west Texas and New Mexico), San Juan (New Mexico and Colorado) and Williston (Montana and North Dakota). It’s also a different type of E&P play, focusing on drilling locations that have already been developed—so production is generally lower than when the assets were proven, but operation costs tend to be both lower and more steady.

This isn’t Bob’s first rodeo. He previously founded XTO Energy and served as its chairman until 2010, when it merged with Exxon Mobil (NYSE:) in a massive $41 billion transaction. Two years later, he spun up TXO, then helped take it public in 2023.

Bob owned 4.5 million shares of the company two years ago. He owns double that today. His most recent transactions—spending more than $8 million on 600,000 shares in early June—are just the latest in a nearly $30 million buying binge since early May.

Sure, he’s purchasing while TXO shares are on the upswing in 2026.

But He’s Also Buying a Deep Longer-Term Dip

He’s doubling down on TXO while the company is starting to focus more on its core positions. In April, the company announced several asset sales meant to liquidate its position in the Cross Timbers JV. And it plans to spend about 80% of its developmental expenditures on the Williston Basin this year.

As far as income is concerned, TXO Partners is an oddity in that it’s an E&P play structured as a master limited partnership (MLP). Its policy is to distribute all available cash to unitholders, so payments will change from one quarter to the next—but even at lower distributions of late, TXO is still paying out a generous 11%-plus.

This Growing 11% Dividend Is One of Our Top Buys Right Now

My problem with TXO: Giant payouts are supposed to be our shock absorbers. But when the distribution moves around as much as the stock price, it’s not absorbing anything. All we’re really getting is a false sense of security.

Not to mention, because it’s an MLP, we have to deal with the dreaded K-1 come tax time.

One of my favorite high-yielding funds is a much better way to collect 11%-plus.

Just check out the dividend history: The only changes in this fund’s monthly payout are for the better—the regular distribution has grown over time, and its shareholders have even pocketed the occasional special dividend!

This 11% Payday Is the Real Deal

We can also sleep soundly at night knowing that this fund is helmed by one of the best managers in the bond business. Morningstar previously named him Fixed Income Manager of the Year. And he’s literally a hall-of-famer, honored by the Fixed Income Analysts Society Hall of Fame.

And because this fund is actively managed, it can drop in and hoover up sudden bond discounts that index funds simply aren’t built to identify and snare.

This “battleship” fund is a must-buy for all income investors, and I want to share my complete research on it right now.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.