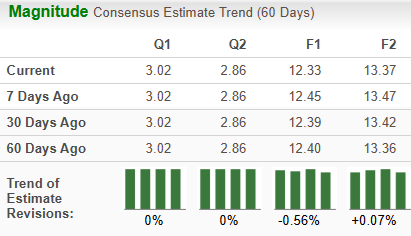

International Business Machines Corporation IBM is scheduled to report second-quarter 2026 earnings after the closing bell on July 22. The Zacks Consensus Estimate for sales and earnings is pegged at $17.66 billion and $3.02 per share, respectively. Earnings estimates for IBM for 2026 have declined 0.56% to $12.33 per share over the past 60 days, but are up 0.07% for 2027 to $13.37.

IBM Estimate Trend

Image Source: Zacks Investment Research

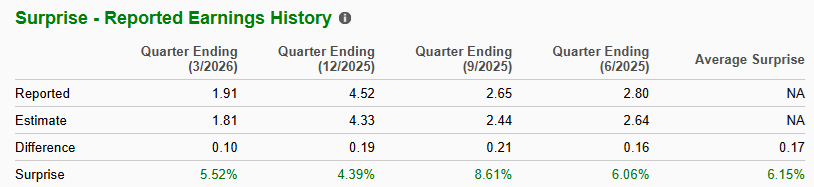

Earnings Surprise History

The cloud and data platform provider delivered a four-quarter earnings surprise of 6.15%, on average, beating estimates on each occasion. In the last reported quarter, the company delivered a 5.5% earnings surprise.

Image Source: Zacks Investment Research

Earnings Whispers

Our proven model does not predict an earnings beat for IBM for the second quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

IBM currently has an ESP of -0.33% with a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping Upcoming Results

During the second quarter, IBM launched two new managed services, Red Hat AI Inference and Red Hat OpenShift Virtualization Service on IBM Cloud. The new solutions are designed to support faster AI adoption while improving the security and efficiency of virtual workloads. IBM formed a collaboration with OpenAI during the quarter. The alliance focuses on taking AI capabilities beyond just improving productivity and efficiency and integrating AI directly into an organization’s cybersecurity operations. This will likely act as a catalyst for IBM’s project Lightwell, which aims to improve security across the open-source software ecosystem. IBM has committed $5 billion to this project. Such investment in innovation and strategic collaboration will likely boost IBM’s commercial prospects in the growing cybersecurity space and are likely to have generated incremental revenues for the Software segment.

During the to-be-reported quarter, IBM partnered with Google Cloud to help businesses adopt AI faster and modernize their technology systems. The deal creates a new Google Cloud Practice within IBM Consulting, combining IBM’s industry expertise and AI-powered IBM Consulting Advantage platform with Google Cloud’s Gemini Enterprise AI platform. The collaboration strengthens the company’s expertise in cybersecurity, data management and cloud infrastructure. By integrating Google Cloud’s Gemini AI capabilities with its watsonx platform and using technologies such as Red Hat OpenShift, HashiCorp, Apptio, BigQuery and Confluent, IBM aims to help businesses improve automation, gain deeper data insights and enhance operational efficiency. These are likely to have generated additional revenues for the Consulting segment.

However, despite solid hybrid cloud, quantum technology and AI traction, IBM faces stiff competition from Amazon Web Services and Microsoft’s Azure. The company is also facing challenges from AI firm Anthropic as the latter’s Claude Code tool can modernize legacy COBOL systems — a foundational programming language deeply embedded in IBM’s mainframe ecosystem. With Claude Code proposing to substantially automate code exploration, documentation, refactoring and security analysis, it threatened to reduce enterprises’ reliance on specialized legacy service providers like IBM, bringing its sustenance at stake. This is likely to redefine the competitive landscape, leading to a broad-based downslide across the sector. Increasing pricing pressure is eroding margins, and profitability has trended down over the years, barring occasional spikes.

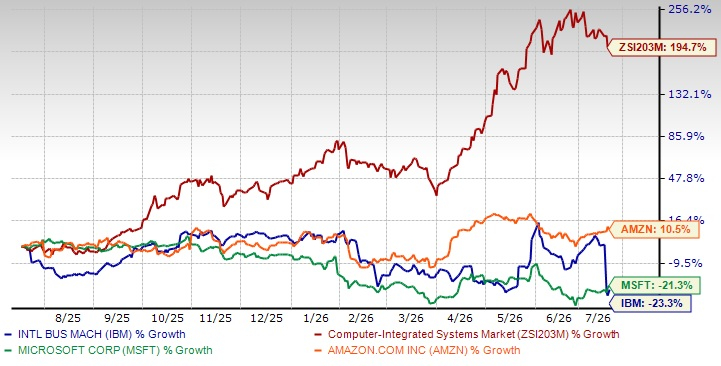

Price Performance

Over the past year, IBM has plummeted 23.4% against the industry’s rise of 194.7% and its peers like Microsoft Corporation MSFT and Amazon.com, Inc. AMZN. While Microsoft has declined 21.3%, Amazon surged 10.5% over this period.

One-Year IBM Stock Price Performance

Image Source: Zacks Investment Research

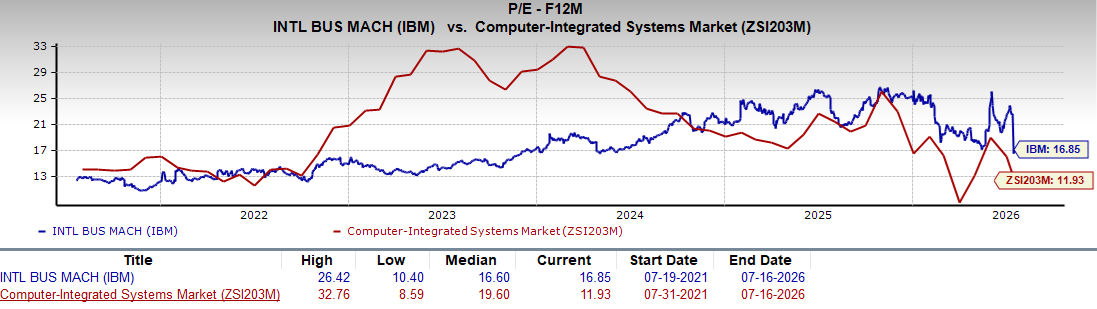

Key Valuation Metric

From a valuation standpoint, IBM appears to be trading at a premium relative to the industry and is trading above its mean. Going by the price/earnings ratio, the company shares currently trade at 16.85 forward earnings, higher than 11.93 for the industry and the stock’s mean of 16.6.

Image Source: Zacks Investment Research

Investment Considerations

IBM aims to benefit from the increasing propensity of business enterprises to undertake a cloud-agnostic and interoperable approach to secure multi-cloud management with a diligent focus on hybrid cloud and generative AI solutions. With a surge in traditional cloud-native workloads and associated applications, along with a rise in generative AI deployment and quantum computing, there is a radical expansion in the number of cloud workloads that enterprises are currently managing. This has resulted in heterogeneous, dynamic and complex infrastructure strategies, which have led to a healthy demand trend.

However, IBM’s margins might have been strained by limited cost-cutting opportunities and intense competitive pressures, likely delaying key product launches. Stiff competition from established players and new challengers has dented its growth prospects. Management observed that rapidly evolving, industry-wide cybersecurity concerns adversely impacted the client’s buying patterns as quarterly capex spending shifted more toward servers, storage and memory purchases. This is likely to have affected its Infrastructure business in the quarter.

End Note

IBM is trading at a premium valuation, and investors could wait for a better entry point to cash in on its long-term fundamentals. With declining earnings estimates, the stock is witnessing a negative investor perception. Consequently, it might be prudent to trade with caution at the moment.

IBM expects its growth to be driven primarily by analytics, cloud computing and security services. A better business mix, improving operating leverage through productivity gains and increased investments in growth opportunities, will likely be conducive to long-term growth. IBM is expected to benefit in the long run from strong demand for hybrid cloud and AI, which will likely drive growth in the Software and Consulting segments. Investors might therefore hold the stock for long-term gains.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers “Most Likely for Early Price Pops.”

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

International Business Machines Corporation (IBM) : Free Stock Analysis Report

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.