To no one’s surprise, Japan and South Korea entered a full-scale risk unwind.

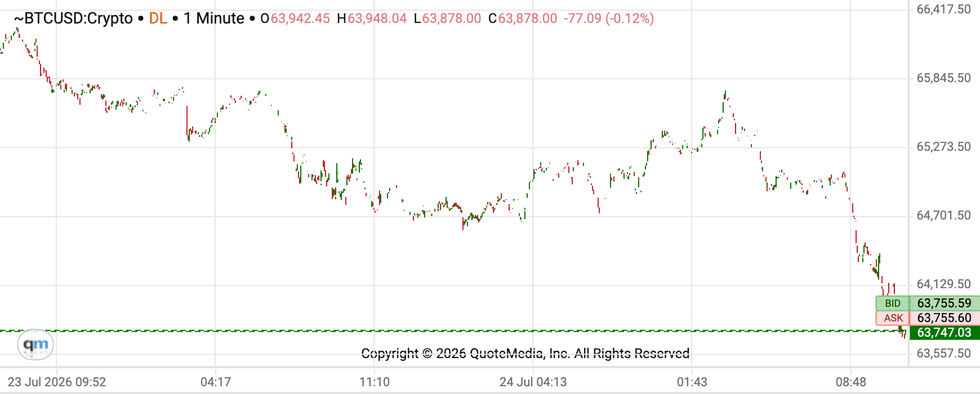

The selling was concentrated exactly where the crowd had been most comfortable. Samsung Electronics and SK Hynix fell around 7% to 8%, while Kioxia tumbled 10% in Japan. The slipped back below 70,000, dragged lower by the same semiconductor complex that had done so much of the heavy lifting on the way up.

Takeaways

-

Korea’s open was not a normal risk-off move. A KOSPI sidecar halt, KORU down around 30%, and 7% to 10% losses in the semiconductor heavyweights point to forced de-risking, not patient institutional selling.

-

The pressure landed exactly where the market was most crowded: AI, memory, leveraged ETFs and retail margin. Samsung, SK Hynix and Kioxia became the first visible casualties of a trade that had been priced for perfection.

-

The SOX collapse overnight provided the spark, but Korea’s leverage structure supplied the fuel. Once retail stops are hit, the market can trade on liquidation logic rather than valuation logic.

-

The immediate question is whether US semis stabilise. Until they do, every rebound in Japan and Korea risks becoming an opportunity for trapped longs to reduce exposure rather than a clean dip-buying signal.

Japan and South Korea Open Into a Semiconductor Storm

To no one’s surprise, Japan and South Korea entered a full-scale risk unwind.

Korea was hit first and hardest. The dropped more than 6% at the open, briefly breaking below 8,000 as program selling became so aggressive that the exchange activated a sidecar halt. was down roughly 30%. For anyone watching the build-up in retail leverage, margin debt and leveraged ETF exposure, this was not a mystery. It was the margin-call massacre many had been waiting for.

That was fast.

The selling was concentrated exactly where the crowd had been most comfortable. Samsung Electronics and SK Hynix fell around 7% to 8%, while Kioxia tumbled 10% in Japan. The Nikkei slipped back below 70,000, dragged lower by the same semiconductor complex that had done so much of the heavy lifting on the way up.

The overnight trigger was ugly enough. US equities reversed lower, while the fell more than 6%, sending an immediate warning flare across Asia’s AI and memory names. But the real damage came from the market structure underneath. When a heavily owned, highly levered sector begins falling into an open where retail participation is large and forced selling is close, price stops being a view and becomes a liquidation mechanism.

Korea is now the sharper version of the broader AI unwind. The issue is not whether Samsung, SK Hynix or Kioxia remain strategically important companies. They do. The issue is that a great earnings story can still become a terrible trading vehicle when leverage, momentum and crowded positioning all decide to leave through the same exit.

The sidecar halt may slow the machinery, but it does not remove the pressure. If the SOX remains under stress and US tech does not stabilise, Asia’s semiconductor complex will keep trading less like an investment theme and more like a weather system: violent, fast-moving and unforgiving to anyone caught standing in the wrong place.

The market had spent months rewarding momentum. This morning, it began charging interest on it.

Here are the key excerpts from this morning’s New Close Note, advising people in North Asia to fasten their seatbelts.

Korea Set to Open Into a Momentum Storm

Yesterday, that machine started to cough.

rallied while semis, memory names, and neocloud plays were taken to the wood chipper. High-beta momentum baskets, now loaded with chip and memory exposure after their extraordinary first-half run, suffered one of their worst sessions in years. One major high-beta momentum basket fell around 9%, while the long-short version was down roughly 10%, putting it on pace for its ugliest day since the vaccine shock in 2020.

The winners and losers had suddenly started moving in the wrong direction at the same time, which is usually when traders realise they are no longer dealing with a normal sector rotation. This was a repricing of duration. The market is beginning to ask whether capex growth peaks before earnings estimates have had time to catch up with the optimism already embedded in the chip complex.

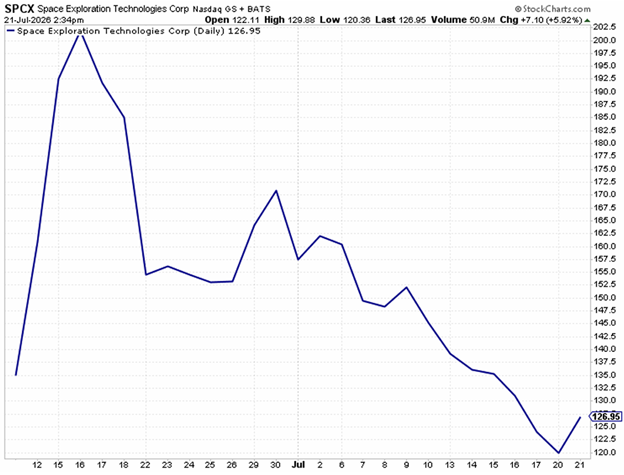

has become one of the cleaner fault lines. It has not closed below its 20-day moving average near 1049 since early April, a remarkable stretch for a stock with this much volatility. If it loses that level, the next obvious area sits closer to the 50-day moving average around 842, roughly 20% lower. Reports that Apple (NASDAQ:) may be exploring alternative memory-chip supply channels have not exactly helped the mood, but the larger issue is whether investors are still willing to pay for a memory cycle built on the assumption that demand remains hotter for longer while some of the largest buyers of compute begin talking about unused capacity.

That is why Korea matters so much this morning.

Korea sits directly in the blast radius of the memory unwind. It has heavyweight semiconductor exposure, deep retail participation, sizeable leveraged-product flows and a familiar ability to turn a global growth theme into a domestic trading carnival. When the story is rising, the carnival is glorious. The rides are fast, the crowd gets louder, and nobody is particularly interested in asking whether the ground beneath the tent is softening.

When the story turns, the hyper-leveraged exits narrow very quickly.

KORU’s 23% fall is not just another ugly number on the screen. It is a warning that leverage once again collides with a narrative reversal, and that rarely ends gently. The question heading into Seoul today is not whether the market feels the move, but how much of the opening must be processed through forced de-risking, volatility circuit breakers, and traders realizing that a crowded trade does not need a terrible earnings print to unravel.

It only needs the story to stop getting better.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.