There’s only so much higher a $5 trillion stock can go.

Listen to the audio version of this article (generated by AI).

Hello, Reader.

There’s one simple problem with investing in a company like Nvidia Corp. (NVDA):

There’s only so much upside left to a $5 trillion stock.

- If shares were to double again, it would make Nvidia worth more than the Dutch East India Co. (VOC), the most valuable company in history in inflation-adjusted dollars ($8 billion).

- If it were to triple, Nvidia would be worth more than every stock on the Japanese and U.K. stock markets combined ($12 billion).

- And if it were to rise 10X, that would make Nvidia worth almost as much as the total U.S. stock market.

Like a goldfish in a bowl, every corporation is limited by the economies they swim in. And no matter how successful Nvidia becomes, it’s still constrained by having only 8.3 billion potential customers… at least until they figure out how to sell AI chips to rabbits and mice.

Now, I fully believe that Nvidia is an amazing company. In fact, I recently compared the world’s most valuable company to Babe Ruth, the most famous baseball player in American history. The chipmaker will keep hitting home runs, and there could be at least another 30% upside in shares, especially after last week’s brutal selloff.

But I think you can do better than that.

Thirty percent returns are table stakes on Wall Street… something you can earn with a high-dividend stock in three to four years, or by buying a house in the right ZIP code. In fact, my old Lexus rose 30% in value while sitting in my driveway in 2021.

That’s why I’ve built my career around finding 1,000% winners instead – the extraordinary stocks that can rise 10X or more. Most people only need to buy two or three of these over their entire careers to make a life-changing amount of money. I’ve found over 40.

Last year, my focus was on chipmakers like Advanced Micro Devices Inc. (AMD) and data center companies like Oracle Corp. (ORCL). These “second wave” AI winners were still growing fast, even as Nvidia’s growth was plateauing.

Now that those stories have played out, I’ve turned my attention to a third wave of AI companies: “Enablers.”

These far smaller firms are providing the “picks and shovels” to the AI buildout and are the new set of stocks that can rise 10X.

These are the companies I’m now recommending.

In fact, I recently added one to my flagship service, Fry’s Investment Report.

So, in today’s Smart Money, I’d like to tell you about this little-known energy company with incredible potential.

Then, I’ll share how you can find even more Enabler companies with bigger upsides than Nvidia.

Let’s dive in…

AI’s Energy Problem

We all know that electricity has gotten expensive in America. The average household now pays roughly $2,000 per year in utility bills, or 2.5 times more than in 2000.

That figure is even higher in fully deregulated states like Massachusetts and Maryland, where private companies are free to set their own rates.

Now, we can’t blame energy costs. Henry Hub natural gas prices have only risen from $2.42 per unit in 2000 to $2.94 today… a 21% increase in 26 years. (Again, my car did that and more in 12 months).

“Greedy” energy utilities aren’t responsible for the spike, either… at least not entirely. For instance, Massachusetts’ largest private utility has been cash-flow negative for nine of the past 10 years and struggles to meet its dividend payments.

Instead, the real culprit is that America doesn’t make enough electricity.

Most of America’s coal-fired power plants were built 40 to 60 years ago, and they’re reaching their end-of-life all at once. Natural gas power has filled around two-thirds of that gap, but it is hitting a limit from shortages of gas turbines and pipeline capacity. Offshore wind power has proved phenomenally expensive. The Massachusetts utility I talked about earlier has already lost $2.5 billion on its wind projects… and still counting.

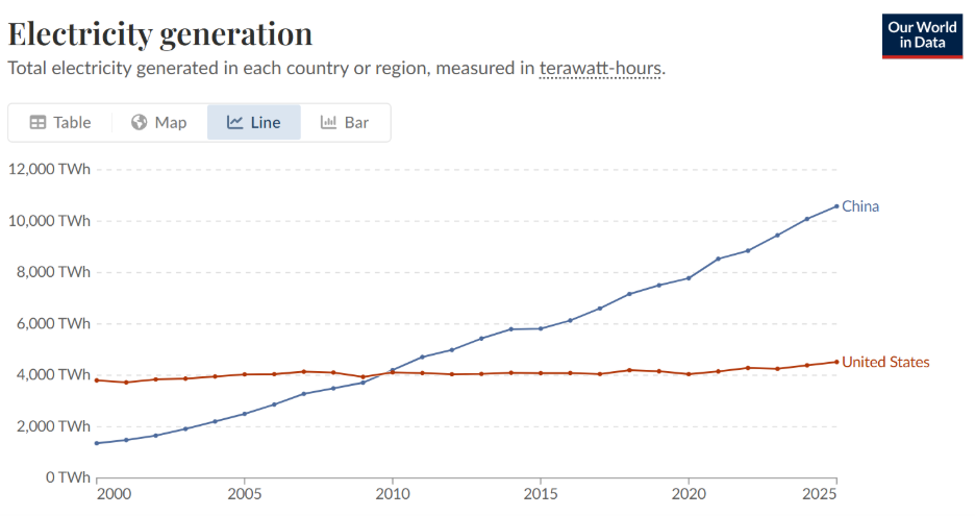

In fact, America’s growth in electrcity generation looks like a rounding error compared to growth in countries like China. The chart below tells the tale.

And now, the tightness is getting worse because of artificial intelligence. Data centers are already using around 5% of electricity in the U.S., and they’re only getting started.

For instance, the “Stratos” AI data center planned for Box Elder County, Utah, will need 9 gigawatts of electricity – more than double what the entire state currently uses. If estimates are correct, we’ll need anywhere from 12 to 20 of these “Stratos”-sized projects by 2032 just to keep up with AI demand.

That’s a lot of electricity.

To play this trend, longtime readers will know that I’ve selected several natural gas plays, which are outperforming many of the “obvious” AI plays like Nvidia.

But American data centers and utilities alike are now turning to another power source to get ahead…

The Sun Also Shines

Solar power.

This intermittent source of electricity has become a surprisingly popular way to add generation capacity. Solar panels are cheap, battery storage is viable, and the technology is supported by both sides of the political spectrum.

My home state of California still leads the nation in installed solar capacity, but Texas, at No. 2, has almost caught up. Florida, Arizona, and North Carolina round out the next three spots.

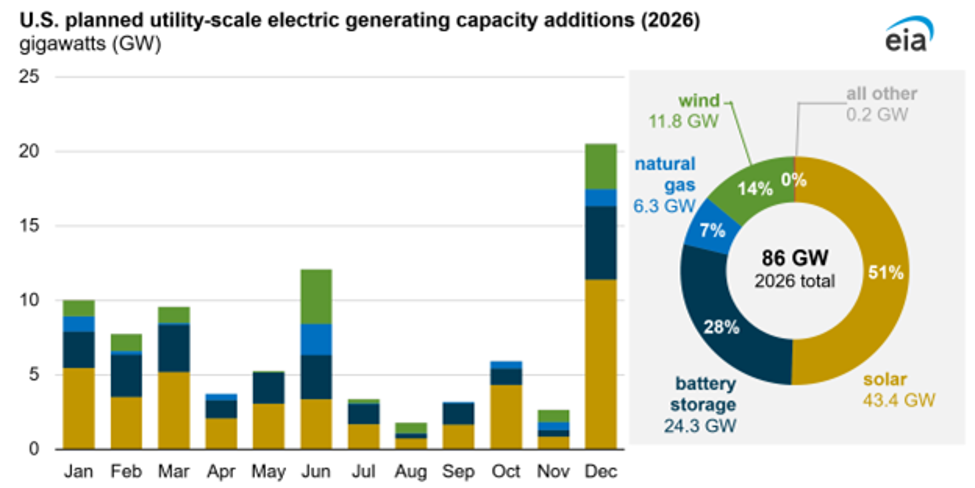

In fact, 51% of American power-grid additions in 2026 is expected to come from solar, and another 28% from battery storage, according to the U.S. Energy Information Administration (EIA). Most will happen in the South and Southeast.

Solar and battery storage will dominate new electricity additions this year.

Source: EIA

That’s creating a bonanza for solar stocks, which have risen 84% in the past year alone.

Solar power is also surprisingly useful for AI data centers. Solar output matches the 9-to-5 workloads of corporate AI use (not to mention peak cooling demands of AI data centers), and many state utilities now allow new data centers to “cut the line” for grid connections if they add solar-and-battery capacity. BloombergNEF estimates that battery storage can cut a data center’s connection timeline by five years – an eternity in the AI arms race.

Now, there are many terrible solar companies out there. The industry is cut-throat competitive from years of international price-dumping, and Chinese-related companies now control 80% to 90% share of solar components.

Western firms like Canadian Solar Inc. (CSIQ) must pay whatever their Chinese suppliers demand. We’ve already seen two major solar bankruptcies this year: SOLON Corp. and Freedom Forever. The latter ironically named firm is now being investigated by the state of Texas for fraud.

But I believe I’ve found an innovative energy firm that should do far better.

This company has developed a battery storage technology that absorbs and smooths the violent swings between AI data center demands and solar power generation. It’s solving a multiyear problem that has plagued the data center industry.

For instance, in July 2024, a small electrical disturbance in Northern Virginia’s “Data Center Alley” that lasted just a few milliseconds triggered emergency shutoffs that cut 1.5 gigawatts of load from the grid all at once – the equivalent of turning off an entire midsized city. Power plants across Virginia and Maryland were ordered to throttle output to prevent a cascade of damage, and engineers were then forced to manually reconnect each data center to the network.

This company helps prevent such wild swings, making data centers easier to connect to the grid. And growth is expected to surge.

Nvidia is a remarkable company. I’ve said that before and I’ll say it again. But remarkable companies and remarkable returns are different things — especially when the company is already worth $5 trillion.

This goldfish has nearly outgrown its bowl.

The energy company I’ve described today is still swimming in open water.

Revenue growth is expected to flip from negative 16% last year to positive 48% this year, and then remain in the 20% range after that. And it looks set to break even this year before profits start rolling in during the fiscal 2027 year.

Its technology is solving a problem that’s costing data centers billions. And its stock hasn’t been discovered yet by investors still staring at Nvidia.

That’s where the 1,000% winners come from. Not from the most famous fish in the tank — but from the ones nobody’s watching yet.

You can click here to learn how to access the name of this AI energy company.

Regards,

Eric Fry

Editor, Smart Money

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.