After earning $1.91 per share last year, analysts expected Micron Technology Inc. () to grow earnings by nearly 11X year-over-year (YoY) to $20.83 for fiscal Q3 2026, a tall order to say the least. Micron blew past estimates after $25.00 per share. This sent the stock surging 17% higher the following morning, reaching new all-time highs of $1,255.00, but it was met with profit-taking as shares fell as low as $1,007.50 in the following days. Leaving investors to ponder if there is any more upside in the stock?

The Bar Was Set High, But Micron Flew Way Over It in Q3

Expectations were set very high for fiscal Q3 2026. Micron reported earnings per share (EPS) of $25.00, well above the $20.83 consensus estimate by $4.28. Revenues skyrocketed 345.8% YoY to $41.46 billion, crushing consensus estimates of $35.85 billion. Capex was $7.1 billion, and adjusted free cash flow rose to $18.3 billion. Non-GAAP gross margin rose to 84.9% compared to $74.9% quarter-over-quarter (QoQ) and 39% YoY.

The Cloud Memory Business Unit revenues nearly doubled to $13.77 billion QoQ. Core Data Center Business Unit revenue rose to $11.5 billion, up from $5.7 billion QoQ. Mobile and Client Business Unit revenue surged to $11.5 billion, up from $7.7 billion QoQ. Total data center revenue grew to $25 billion in FQ3, indicating a $100 billion run rate. Data Center SSD revenue more than doubled QoQ to $5 billion.

The Company raised fiscal Q4 2026 EPS guidance to $30.00 to $32.00, with a midpoint of $31.00, versus $25.72 billion in consensus analyst estimates. Revenues are expected between $49.00 billion andand $51 billion, with a midpoint of $50.00 billion, versus $43.58 billion in analyst estimates. Non-GAAP gross margins are expected to rise to 86% in FQ4.

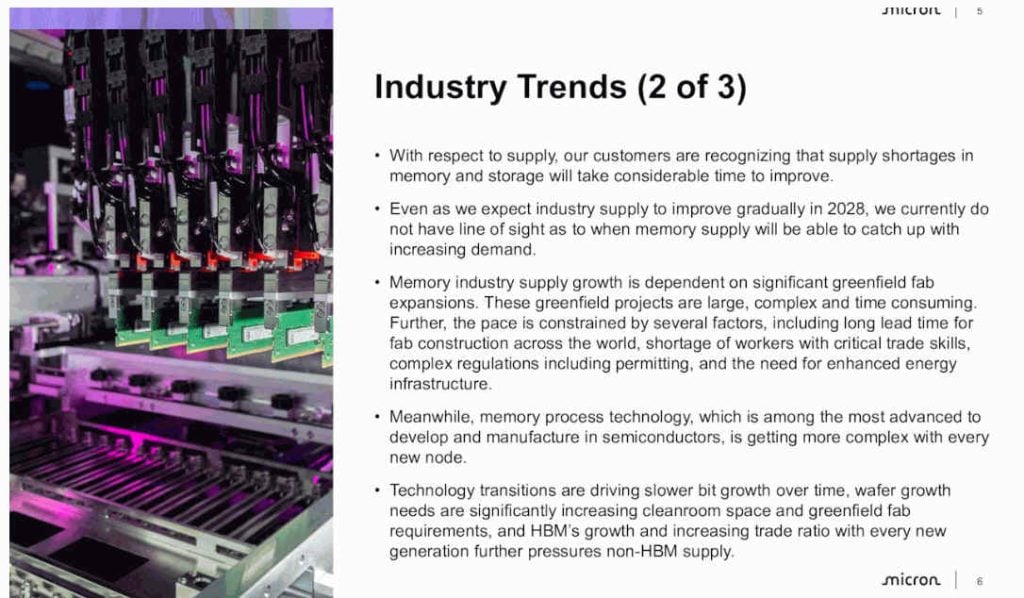

Supply Shortages Are Not Expected to Improve Until 2028

The AI boom has an insatiable hunger for memory and storage capacity, as evidenced by Micron’s results.

While supply shortages are expected to improve gradually in 2028, Micron doesn’t have an exact timeline for when memory supply will catch up with demand. The Company has secured 16 multi-year Strategic Customer Agreements (SCAs), which cover nearly 20% of its DRAM volume and a third of its NAND volume. This includes nearly $100 billion in revenue and $22 billion in deposits, enhancing the visibility and predictability of its financial performance moving forward.

Micron’s Valuation Hinges on This Distinction

The problem with Micron’s valuation has been the cyclical nature of the DRAM market. During boom times, its P/E has climbed into the 10X to 15X range, but during bust times it has dropped into the 5X to 9X range. Micron currently has a forward P/E around 14X.

The SCAs support management’s contention that the memory market is becoming more durable and less cyclical, a concern that has long plagued the commoditized DRAM market. They are trying to convince the market that it’s no longer a classic cyclical memory company but an AI infrastructure supplier, thanks to enhanced pricing visibility. This is because AI infrastructure companies typically trade at 20X to 25X forward earnings, while higher-tier companies trade at 30X to 60X.

MU Stock Has Potential to Surge to $1,364 or Drop to $731

After hitting all-time highs at $1,255.00, MU stock is at a crossroads. It can propel itself higher towards its upper Bollinger Bands at $1,362.63 or sell off down towards its 15-week simple moving average (SMA) at $731.72.

MU stock formed a weekly market structure high (MSH) sell trigger at $1,023.65, below its 5-week SMA. The weekly stochastic is overbought at the 87-band. If the stochastic falls below the 80-band, then gravity can set in as it oscillates lower. A fall under the 20-band would indicate an oversold condition. The nominal pullback level on the weekly uptrend would be its 15-week SMA near $731. Investors looking for pullback entries may consider targeting this area for potential entries.

Micron Technology has been an original member of the index since 1985, which can be tracked using the Sigmanomics NASDAQ-100 forecast. It carries a 4.8% weight in the index, ranking fourth-largest behind Microsoft Co. (NASDAQ: MSFT).

Writtten by, Jea Yu

With over 25 years of investing, analysis and trading experience in the equities and options market, Jea brings layered insights into the mechanics of how markets and trends operate. Jea is a four time published author with finance books focused on trading and risk management published by McGraw-Hill, John Wiley & Sons and Bloomberg Press. Jea has written over 2,500 articles across various digital platforms spotlighting and highlighting stocks, trends and trading strategies.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.