We often hear that appearances can be misleading, a truth we tend to overlook. Micron (MU), a leading semiconductor company specializing in memory chip design, embodies this adage. Initially, the stock may appear overvalued with earnings of $0.67 per share over the past year, resulting in a hefty price-to-earnings ratio of 161x. However, such surface-level assessments fail to consider crucial factors like future guidance and consensus estimates that project a more nuanced picture of the stock’s actual worth.

To delve deeper into Micron’s potential, Michael Byrne at Tipranks has penned a detailed analysis of MU stock, accessible here.

Let’s explore three key insights that shed light on MU’s valuation from a broader perspective.

- Forward-Looking Valuation: While Micron’s trailing price-to-earnings ratio may seem inflated presently, investors are forward-looking creatures. Projections for the next quarter reveal an anticipated earnings surge to $1.74 per share, more than doubling its current figure. Looking ahead to Fiscal 2025, analysts foresee earnings hitting an impressive $8.93 per share, leading to a more reasonable P/E ratio of 11.8x. Furthermore, estimates for 2026 point to an even lower multiple of 8.2x, signaling significant upside potential.

- Comparison to Industry Peers: Despite exhibiting lower gross margins and a less glamorous profile compared to industry giants like Nvidia (NVDA) and AMD (AMD), Micron’s future trajectory hints at promising prospects. While Nvidia and AMD may boast higher margins, the growing importance of memory chips in GPU processors, crucial for AI advancement, places Micron at an advantageous position. As AI evolves, the demand for greater RAM capacities, catered to by Micron’s specialized memory chips, is set to soar, aligning well with the industry’s future trajectory.

- Technological Advancements: Micron’s expertise in developing high bandwidth memory chips perfectly aligns with the heightened demand for data processing in contemporary GPUs fuelled by AI evolution. As AI applications burgeon, the need for robust RAM support intensifies, a demand Micron is uniquely positioned to meet. This alignment foretells robust growth potential for the California-based firm, underpinning an optimistic earnings outlook for the years ahead.

MU’s Price Target

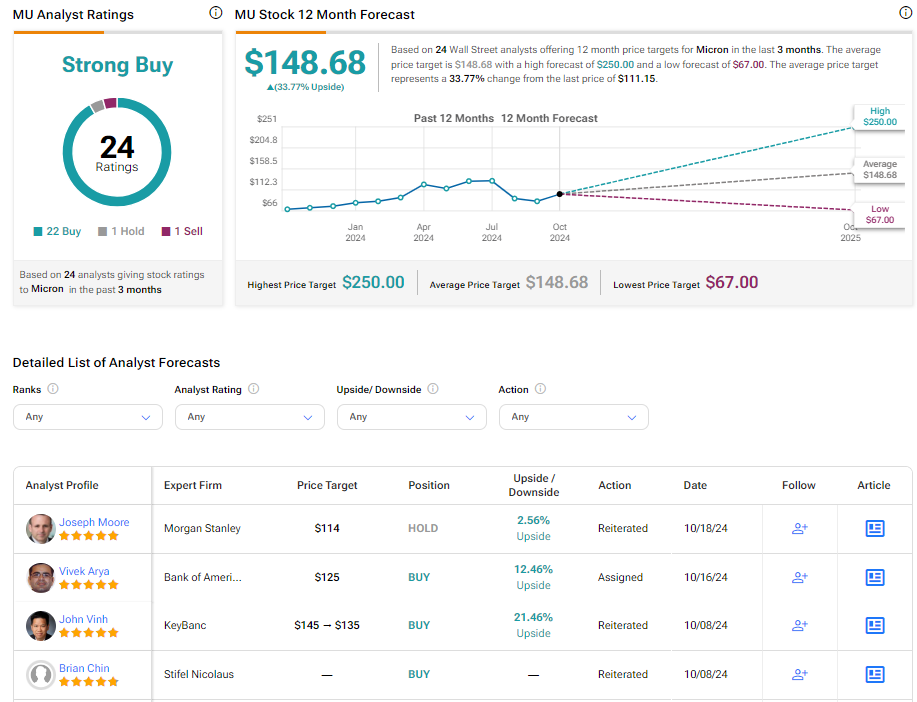

Wall Street exudes confidence in Micron, with 22 analysts rating it as a Strong Buy, 1 as a Hold, and 1 as a Sell. The average price target for MU stock stands at $148.68, hinting at a promising 33.77% upside.

Explore More MU Analyst Ratings Here

In Closing

Although Micron’s valuation might seem lofty on the surface, a deeper exploration of the company’s trajectory reveals a compelling narrative and a potentially lucrative entry point for savvy investors. Positioned to leverage the AI revolution, Micron stands ready to capitalize on the burgeoning need for RAM in the AI landscape.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.