Essent Group Ltd. ESNT sits between mortgage credit, housing affordability and capital discipline. The stock’s appeal is less about momentum and more about valuation and balance-sheet protection.

The debate is whether those supports are enough while rates, affordability pressure and reserve needs limit near-term growth.

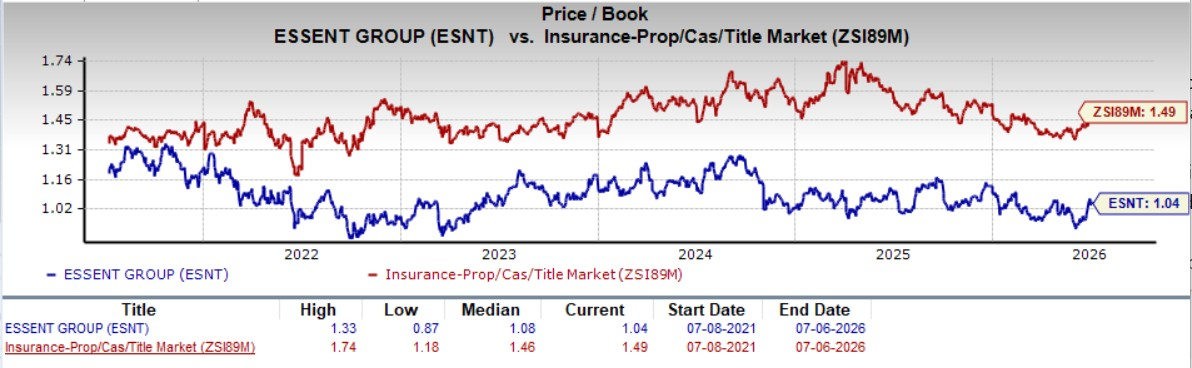

Why ESNT Looks Inexpensive

ESNT trades at 1.04X trailing 12-month book value per share, below the Zacks sub-industry multiple of 1.5X. The multiple is near its five-year median of 1.08X, within a range of 0.87X to 1.33X.

Image Source: Zacks Investment Research

The $68 price target reflects 1.1X trailing 12-month book value. Book value matters for a mortgage insurer because capital, reserves and risk transfer sit at the center of the model. Essent’s book value per share rose to $61.20 as of March 31, 2026. MGIC Investment Corporation MTG and Radian Group Inc. RDN sit in the mortgage insurance peer set, where investors often compare capital strength and price-to-book valuation.

Where the ESNT Bull Case Gets Checked

The housing backdrop keeps the bull case from becoming more aggressive. Affordability and higher rates continue to constrain purchase and refinance activity, limiting mortgage insurance and title volumes. Enact Holdings, Inc. ACT, another mortgage insurance peer, faces the same industry debate over whether stable credit can offset slower originations.

Credit trends also require monitoring. The default rate rose from 2.12% in the second quarter of 2025 to 2.54% in first-quarter 2026 as books seasoned. Loss reserves climbed to $486 million from $447 million in the prior quarter. Property and casualty reinsurance is not yet a major 2026 earnings driver.

Essent’s Shareholder Return Story Matters

Capital return is a key part of the ESNT setup. The company has raised dividends in each of the past six years, with an average five-year annual growth rate of 14%. The board approved a 35 cents per share dividend for the second quarter of 2026.

Buybacks add another support. From the start of 2026 through April 30, Essent repurchased about 3.5 million shares for more than $214 million. Liquidity gives management room to stay patient, with about $1.1 billion at the holding company and an undrawn $500 million revolver.

What Would Make ESNT More Compelling

The clearest trigger would be better mortgage industry volume. A healthier purchase market would support new insurance written and could lift title-related operating leverage. Reserve stabilization would also help if defaults rise mainly from seasoning and paid-loss severity stays low.

Diversification needs more evidence. Essent Re’s property and casualty expansion could become a longer-term earnings leg, while title services could benefit when originations improve. The stronger case would be earnings compounding that does not rely too heavily on buybacks and investment income.

How ESNT’s Ratings Shape the Call

The bottom line is that ESNT looks more like a value-and-capital-return story than a clean growth or momentum idea. The balance sheet is well protected and earnings remain solid, but the housing cycle keeps the upside case measured. ESNT currently carries a Zacks Rank #2 (Buy), a constructive short-term signal tied to estimate revisions. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are more mixed. ESNT has a Value Score of A, a Growth Score of F, a Momentum Score of D and a VGM Score of D. That mix supports a valuation-driven bull case but argues against treating ESNT as a broad-based style winner.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Essent Group Ltd. (ESNT) : Free Stock Analysis Report

MGIC Investment Corporation (MTG) : Free Stock Analysis Report

Radian Group Inc. (RDN) : Free Stock Analysis Report

Enact Holdings, Inc. (ACT) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.