Berkshire Hathaway ($BRK.B) recently posted its Q3 results, shocking investors with its record cash position of $325 billion. This cash hoard is the result of Berkshire’s ongoing stock sales, likely due to Warren Buffett’s cautious stance on market valuations.

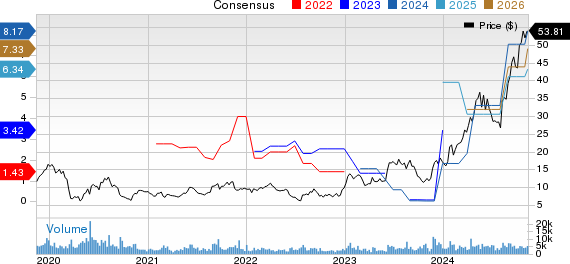

With stocks continuing to rally and President Trump’s re-election further boosting investor optimism, I think the Omaha-based conglomerate is an attractive choice for people who want to remain long in the market with a margin of safety. For these reasons, I am bullish on BRK.B stock, which has risen 35% this year as indicated in the chart below.

Berkshire’s Massive Cash Position

Berkshire’s massive cash reserves is one reason to be bullish on the stock. One can’t help but wonder how the cash piled got so high, especially given the notable jump from last year’s level of $187 billion. I think we can break it down into four main reasons.

The first major contributor has been the sale of its Apple (AAPL) shares, which Berkshire disclosed in its August 13F filing, slashing its stake in the tech giant in half. There’s also the steady sale of Berkshire’s Bank of America (BAC) holdings. Since the summer, Mr. Buffett has offloaded around 258 million shares of Bank of America.

The company’s cash pile has been further supported by strong operating profits. Despite this figure declining by 6.2% to about $10.1 billion in Q3, it still continued to provide Berkshire with notable cash, with its core businesses such as the railways it owns, performing well. Finally, the growing cash position benefits from increased interest income.

Why Is Berkshire Holding So Much Cash?

While I am personally bullish on BRK.B stock, Berkshire’s decision to accumulate such a huge cash pile has been criticized by some investors. For one, the cash position now exceeds the value of Berkshire’s equity holdings and makes up around 32% of its total market cap. With markets reaching new highs, many have argued that the company is essentially leaving money on the table by holding cash rather than investing it.

Berkshire’s strategy seems reasonable though when considered in context, particularly in light of rising interest income. In fact, Berkshire’s latest report revealed that its interest, dividend, and other investment income surged to $5.9 billion, a significant increase from $3.5 billion in the same period of 2023. This increase was primarily fueled by higher interest rates and a substantial investment in short-term U.S. Treasuries. By the end of Q3, Berkshire held roughly $288 billion in T-Bills. Assuming an average yield of around 4.4%, this equates to about $12.7 billion in annual interest income, or about $3.2 billion per quarter.

This suggests that a substantial share of Berkshire’s Q3 investment income is directly tied to yields, showing the impressive cash flow generated from its reserves. With elevated risk-free rates, Berkshire’s strategy appears prudent in the current environment. By stashing cash and investing in T-Bills, Berkshire can secure relatively attractive returns at virtually no risk while also maintaining the flexibility to seize new investment opportunities as they arise.

Why Berkshire Stock Makes Sense

Considering current market conditions, I believe that holding Berkshire Hathaway stock offers a compelling balance between market exposure and a margin of safety, even as some investors seem dissatisfied by Mr. Buffet’s continuous cash accumulation.

This is because holding Berkshire Hathaway allows people to stay invested in the U.S. market thanks to its exposure to several high-quality public and private businesses. At the same time, you benefit from the safety of Berkshire’s massive cash reserves, which offer significant flexibility.

If the market performs well, Berkshire’s stock is likely to follow suit. On the other hand, if the market experiences a downturn or a major correction, Buffett and his team undoubtedly have all the resources needed to capitalize on it at significant scale, creating a solid risk-reward investment opportunity.

Is Berkshire Stock a Buy?

Wall Street sentiment towards Berkshire Hathaway’s more affordable Class B stock remains bullish. There’s now a Moderate Buy consensus rating on BRK.B stock according to one Buy and one Hold recommendation assigned in the past three months. At $531.00, the average Berkshire stock forecast implies 13.24% upside potential.

If you’re wondering which analyst to follow concerning Berkshire stock, consider Brian Meredith from UBS (UBS). He is both the most accurate and most profitable analyst (on a one-year timeframe), boasting an average return of 11.19% per rating and a 90% success rate.

Conclusion

Berkshire Hathaway’s record cash position highlights Warren Buffett’s cautious approach at a time when we see elevated market valuations. By holding cash and investing in U.S. Treasuries, Berkshire is capitalizing on rising interest rates, securing significant low-risk returns while remaining poised for future investments.

This setup offers both stability and flexibility. It also forms a compelling investment case for long-term investors. Berkshire is well-positioned to generate substantial gains if markets continue to rise, while its cash reserves provide it with an opportunity to take advantage of any potential market downturns.