just reminded Wall Street why it’s the undisputed king of aircraft engines.

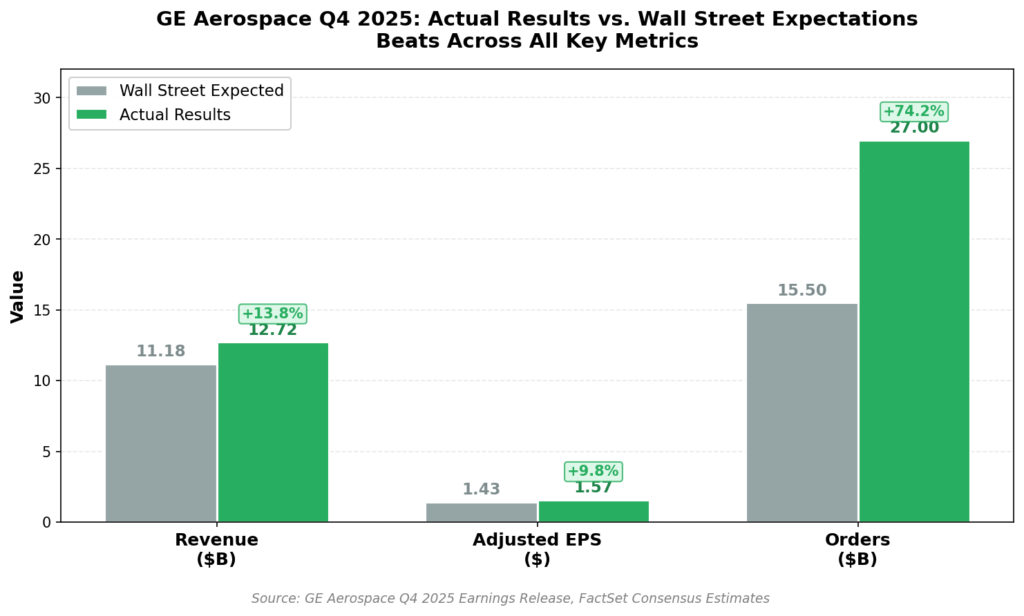

The aviation giant reported Q4 results Thursday morning that blew past expectations on virtually every metric. Revenue hit $12.72 billion, crushing the $11.18 billion consensus by nearly 14%. Adjusted earnings came in at $1.57 per share versus the $1.43 analysts expected. Orders exploded 74% to $27 billion in a single quarter.

“With a strong fourth quarter, GE Aerospace delivered an outstanding year as revenue grew 21%, EPS was up 38%, and free cash flow conversion exceeded 100%,” said Chairman and CEO Larry Culp. “We enter 2026 with solid momentum.”

The stock rose 4.1% in premarket trading to $332.14, pushing toward all-time highs. For investors who missed the 74% rally over the past year, the question now is whether there’s still runway left—or whether perfection is already priced in.

The Numbers That Matter

GE Aerospace’s Q4 print was exceptional across the board. Here’s how it stacks up:

Q4 2025 Results vs. Expectations:

- Revenue: $12.72B actual vs. $11.18B expected (+13.8% beat)

- Adjusted EPS: $1.57 actual vs. $1.43 expected (+9.8% beat)

- Orders: $27B (+74% YoY)

- Operating Margin: 17.9%

- Free Cash Flow Margin: 13.8%

") Full Year 2025:

Full Year 2025:

- Revenue: $42.3B (+21% YoY)

- Adjusted EPS: $6.37 (+38% YoY)

- Free Cash Flow: $7.7B (+24% YoY)

- FCF Conversion: >100%

- Backlog: ~$190B

The backlog number deserves special attention. At $190 billion, GE Aerospace has nearly five years of revenue visibility at current run rates. That’s the kind of buffer that makes recession fears largely irrelevant for this business.

")

What’s Driving the Surge

Three engines are powering GE’s profit machine right now.

Commercial aviation dominance. The LEAP engine—GE’s joint venture with Safran that powers the Boeing 737 MAX and Airbus A320neo—delivered record shipments in 2025, up 28% year-over-year. Airlines are replacing aging fleets faster than expected, and GE’s installed base of approximately 50,000 commercial engines generates a recurring stream of high-margin service revenue. Commercial engine deliveries rose 25% for the full year.

Defense momentum. With global military spending at record levels and the U.S. Air Force expanding its F110 and F135 engine programs, GE’s Defense & Propulsion Technologies segment is firing on all cylinders. Defense deliveries jumped 30% in 2025, and Q4 defense orders surged 61%. The company has transitioned over 750 engineers to next-generation military programs.

Pricing power. GE’s LEAP engine has effectively “won” the current narrowbody cycle on reliability, giving the company premium pricing power. Analysts at Gabelli Funds expect “at least a double-digit server CPU price hike” on engine service contracts in 2026. That translates directly to margin expansion.

")

The 2026 Outlook

Management guided to adjusted EPS of $7.10-$7.40 for 2026, with the midpoint of $7.25 above the $7.12 Street consensus. Revenue growth is expected in the “low double digits.”

The guidance implies 14% EPS growth at the midpoint—not bad for a stock trading near all-time highs. But the real catalyst will be execution on several key initiatives:

LEAP engine ramp. GE and Safran are targeting 2,000 LEAP engine deliveries in 2026, which would be a record for the joint venture. New production lines in Morocco and North Carolina are coming online to support the ramp.

GE9X resolution. A technical issue during November 2025 testing forced Boeing to suspend 777X flight tests, pushing entry into service from 2026 to early 2027. GE needs to resolve whether the temperature alerts stemmed from a manufacturing defect or design flaw. Swift resolution would clear the path to widebody revenue dominance.

Service revenue growth. Engine shop visits are expected to climb to 6,700 by the end of the decade, up from current levels. Each shop visit generates high-margin parts and labor revenue.

Competitive Positioning

GE’s results highlight the widening gap with rivals.

’s Pratt & Whitney division has spent the past two years addressing GTF engine durability recalls from 2023-2024. While Pratt has made progress, GE’s LEAP engine has captured roughly 60% of widebody engine competitions throughout 2025 based on superior time-on-wing performance.

Boeing remains a critical partner but also a source of uncertainty. The 777X delay hurts GE’s widebody revenue timeline, though the company’s massive narrowbody service business provides substantial cushion.

Safran, GE’s joint venture partner on the LEAP program, benefits directly from GE’s commercial success. The partnership targets record LEAP deliveries in 2026.

How to Play It

GE Aerospace presents a classic quality-at-a-premium setup. The business is exceptional—record backlog, pricing power, diversified revenue streams, and a management team executing at a high level. But the stock has already priced in much of that excellence.

For bulls: The $190 billion backlog provides multi-year visibility. Commercial aviation is in a “super-cycle” driven by fleet replacements and emerging market demand. Defense spending remains elevated globally. Any upside to the 2026 guidance could push shares toward $350-375.

For value investors: The average analyst price target sits around $330, roughly in line with current levels. At 46x forward earnings, the stock isn’t cheap. A pullback to the $280-300 range would offer a better entry point.

Related plays: The and offer diversified exposure to the sector. reports January 27 and could benefit from positive read-through on commercial aviation demand. is a direct play on LEAP engine success.

What to Watch

January 27: Boeing Q4 earnings. GE’s strong commercial orders suggest healthy demand for new aircraft. Boeing’s 737 MAX and 777X commentary will inform GE’s 2026 equipment revenue trajectory.

LEAP production updates: Any supply chain bottlenecks or production delays could impact the 2,000-engine delivery target.

GE9X technical resolution: Watch for updates on the November testing issue. Quick resolution bullish; extended investigation bearish.

Service contract pricing: Analyst commentary on 2026 pricing trends will help calibrate margin expectations.

The Bottom Line

GE Aerospace delivered an outstanding quarter that validates its position as the premier pure-play aviation investment. The combination of a record backlog, pricing power, and execution excellence is rare in any industry.

The risk is that at $330+ per share, the market has already capitalized much of that excellence. The stock trades at 46x forward earnings, which requires continued flawless execution to justify. A miss on LEAP deliveries, GE9X delays, or any crack in commercial demand could trigger a meaningful correction.

For long-term investors, GE Aerospace remains a core aerospace holding. The backlog provides years of visibility, and the FLIGHT DECK operating model is delivering results. For traders, the setup argues for patience—waiting for a pullback rather than chasing an already-extended move.

The aviation super-cycle is real. GE is its biggest beneficiary. The only question is how much of that is already in the price.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.