- Credo Technology (CRDO) is evolving into a vertically integrated leader, moving away from a focus on copper interconnects toward the integration of new silicon photonics technologies.

- Explosive growth in revenue and operating profit confirms that CRDO shares are not overvalued. Using the traditional P/E ratio, the company is trading at a 47.1% discount relative to its key competitors.

- The AI supercycle continues, and with it, strong demand from hyperscalers, allowing for projections of over $600 million in sales from the optical portfolio for fiscal year 2027.

Investment Thesis

In spite of the headwinds facing the copper and optical sectors, Credo Technology Group Holding Ltd () shares have risen by more than 71% since the start of the year. Meanwhile, its market capitalization has soared by 165% over the past year.

Despite the explosive growth, CRDO shares are not overvalued, since the company remains the leader in the AI infrastructure connectivity segment. The company’s financial profile, featuring steady growth in revenue and gross margin, proves the effectiveness of its chosen business strategy.

Now the company is entering a new phase of development, shaping a vertically integrated strategy in which optical connectivity technologies are playing an increasingly important role alongside copper cables. Integrating DustPhotonics’ technologies has the potential to expand the company’s portfolio, diversifying its sales mix by 2027. The timing of this decision is opportune, since, aside from operating at high speeds (1.6T and 3.2T), CRDO is strengthening its competitive moat.

CRDO’s “Defensive Moat”

The company’s strategy is built on creating the “connective tissue” of data centers, and with the ongoing AI supercycle, this is driving growing demand for its products. CRDO’s main solution is copper cables, which are effective over short distances but are outperformed by fiber optics over long distances. But this does not mean copper connections will disappear, because they provide better integrity at a lower cost.

CRDO’s “economic moat” may seem limited, although this is not the case. It is made possible by management’s strategic decisions aimed at expanding the portfolio and developing technological leadership in other highly specialized niches. These include diversifying the revenue structure to reduce dependence on electrical interconnects. The acquisition of DustPhotonics, which allows the company to enter the silicon optics market, was the most prudent decision.

CRDO’s Potential in Optics Following the Acquisition of DustPhotonics

The company completed the acquisition of DustPhotonics in May 2026. DustPhotonics is a developer of silicon photonic integrated circuits integrated into 1.6T and 3.2T optical transceivers. It’s a forward-thinking move that positions CRDO to adapt to new challenges. With DustPhotonics having been a potential acquisition target for Nvidia (NVDA) and Intel (INTC), their technology is both attractive and in high demand. I think this deal will deliver benefits in three key areas.

Firstly, there will be a transformation of the company, reorienting it from a copper interconnect player to a vertically integrated player. Secondly, the portfolio will be expanded to include solutions for the silicon photonics market, in particular for the 3.2T segment. Thirdly, this deal is expected to yield additional short-term benefits. An increase in revenue and profits from new technologies is anticipated as early as the next 12 months. Moreover, Credo’s management projects sales of its optical portfolio to exceed $600 million in fiscal year 2027.

Competition from optical solutions remains the main risk

Competition from manufacturers of optical solutions, on the other hand, is not going away and remains the main risk. As optical solutions advance more rapidly in terms of performance and versatility, the faster individual customers will move away from copper connections. The optics market is divided between two categories of competitors. The first consists of system players, which include Marvell (MRVL) and Broadcom (AVGO). These companies offer efficient solutions for manufacturing DSPs for optical modules, known for their high speed. The second category consists of specialized players, including (LITE) and (COHR). These companies offer a broad range of products in the optical components and transceiver segments, building simple and convenient product integration for any optical solution.

The risks posed by competition from optical solutions will likely only increase, given that technology is constantly improving. Competitors are focused on reducing production costs and increasing the energy efficiency of optical transceivers. This is precisely why the acquisition of DustPhotonics is a very timely and important decision in terms of minimizing the threat posed by the aforementioned competitors.

CRDO’s Valuation Is Far From Being Overvalued

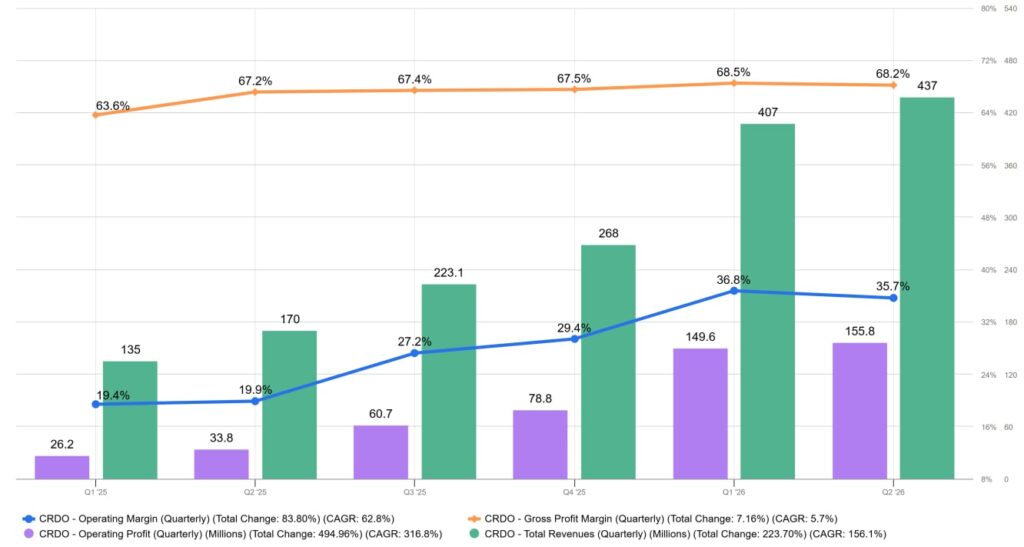

Over the past year, CRDO’s revenue increased from $170 million to $437 million, whereas its operating profit rose from $33.8 million to $155.8 million. The consensus forecast among analysts suggests that revenue will total $511.2 million in the next quarter, while operating profit will be $250.4 million.

If we compare CRDO’s valuation to that of its competitors using the PE ratio, we can see that its PE ratio remains high at 95.3x, but lower than that of others. For example, LITE’s PE ratio is 131.5x, and COHR’s is 157.8x. The other competitor, (ALAB), has a price-to-earnings ratio of 251.6x. Consequently, CRDO shares are trading at a 47.1% discount relative to its competitors.

CRDO’s valuation and the potential of its optical portfolio support a “Buy” rating

My valuation of CRDO anticipates further growth driven by both the short-term impact and long-term potential of the DustPhotonics integration. Its upcoming quarterly earnings report (September 9) could be decisive in confirming market optimism. It is linked to the expansion of the optical portfolio, which is accounting for an increasingly larger share of revenue.

I believe management’s forecasts are realistic, given that the AI supercycle continues, increasing the demand from hyperscalers for optical components used in data center interconnects. In addition, the company’s sales mix will become more diversified next year, reducing its reliance on the AEC segment.

Meanwhile, business margins remain at record highs, with future support coming from lower production costs as the company phases out optical components from third-party suppliers.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.