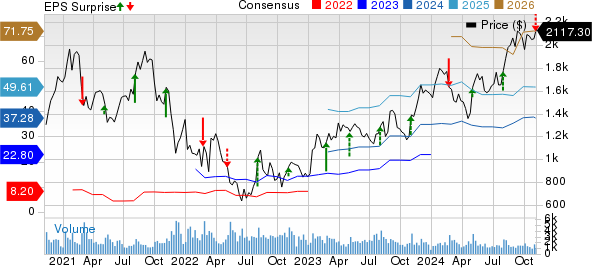

Alphabet’s GOOGL third-quarter 2024 earnings of $2.12 per share beat the Zacks Consensus Estimate by 15.85%. The figure grew 37% year over year.

GOOGL’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 11.84%.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Revenues of $88.3 billion increased 15% year over year (16% at constant currency).

Net revenues, excluding total traffic acquisition costs (“TAC”) (the portion of revenues shared with Google’s partners and the amount paid to distribution partners and others who direct traffic to Google’s website), were $74.549 billion, which surpassed the consensus mark by 2.34%. The figure rose 16.4% year over year.

Alphabet Inc. Price, Consensus and EPS Surprise

Alphabet Inc. price-consensus-eps-surprise-chart | Alphabet Inc. Quote

TAC of $13.719 billion rose 8.5% year over year.

GOOGL shares were up more than 6% in pre-market trading on Wednesday. Alphabet has gained 21.5% year to date, outperforming the Zacks Internet-Services industry’s return of 20% but lagging the Zacks Computer & Technology sector’s 27.6%.

GOOGL Lags Sector YTD

Image Source: Zacks Investment Research

Before diving into GOOGL’s investment prospects, let’s take a glance at its quarterly numbers.

GOOGL’s Top Line Rides on Search, YouTube & Cloud Growth

Google Services revenues increased 12.5% year over year to $76.51 billion and accounted for 86.7% of the total revenues. The figure beat the Zacks Consensus Estimate by 2.1%.

Search and other revenues increased 12.2% year over year to $49.385 billion, surpassing the Zacks Consensus Estimate by 1.12%.

YouTube’s advertising revenues improved 12% year over year to $8.921 billion, beating the consensus mark by 0.71%.

Google Network revenues decreased 1.6% year over year to $7.548 billion but beat the consensus mark by 1.58%.

Google advertising revenues rose 10.4% year over year to $65.854 billion and accounted for 74.6% of the total revenues. The figure beat the consensus mark of by 0.97%.

Google subscriptions, platforms and devices revenues, formerly known as Google Other revenues, were $10.656 billion in the third quarter, up 27.8% year over year. The figure beat the consensus mark by 9.4%.

Google Cloud revenues surged 28.8% year over year to $11.35 billion and accounted for 12.9% of the quarter’s total revenues. The figure surpassed the Zacks Consensus Estimate by 4.02%.

Other Bets’ revenues were $388 million, up 30.6% year over year and accounted for 0.4% of the third-quarter revenues. The figure missed the consensus mark by 1.82%.

GOOGL’s Operating Margin Expands Y/Y

Costs and operating expenses were $59.747 billion, up 7.9% year over year. As a percentage of revenues, the figure declined 450 basis points (bps) on a year-over-year basis.

The operating margin was 32.3%, which expanded 450 bps year over year.

Segment-wise, Google Services’ operating margin of 40.3% expanded 510 bps year over year.

Google Cloud’s operating income was $1.947 billion compared with $266 million reported in the year-ago quarter.

Other Bets reported a loss of $1.116 billion compared with a loss of $1.194 billion in the year-ago quarter.

Alphabet’s Balance Sheet Remains Strong

As of Sept. 30, 2024, cash, cash equivalents and marketable securities were $93.23 billion, down from $100.7 billion as of June 30, 2024.

Long-term debt was $12.297 billion as of Sept. 30, 2024 compared with $13.24 billion as of June 30, 2024.

Alphabet generated $30.698 billion of cash from operations in third-quarter 2024 compared with $26.6 billion in second-quarter 2024. GOOGL spent $13.061 billion on capital expenditure, netting a free cash flow of $17.637 billion in the reported quarter.

Solid liquidity is helping Alphabet maintain its dividend payout. In third-quarter 2024, GOOGL paid $2.5 billion in dividends and bought back shares worth $15.3 billion. Over the trailing 12 months, Alphabet has returned $70 billion to shareholders.

Growing Cloud Business: A Key Catalyst for GOOGL

Google Cloud’s Robust third-quarter 2024 results benefited from reflecting accelerated growth across AI infrastructure, enterprise AI platform Vertex, generative AI (Gen AI) solutions and core Google Cloud Platform products.

GOOGL’s strong AI portfolio is helping it attract new customers, win larger deals, and deepen product adoption among existing customers.

Gemini API calls have grown roughly 40 times in a six-month period. Enterprises like Snap SNAP is leveraging Gemini’s strong multimodal capabilities to drive engagement within its My AI chatbot in the United States.

Enterprises are combining Alphabet’s AI platform with data platform, BigQuery, to make accurate real-time decisions. BigQuery machine learning operation saw 80% growth over the past six months, driven by this strong demand.

Strong adoption of cybersecurity solutions, Google Threat Intelligence and Security operations, has been a key catalyst. Over the past six quarters, customer adoption of Mandiant-powered threat detection increased four times.

Alphabet has been rapidly growing in the booming cloud-computing market. Google Cloud has solidified its position as the third-largest provider in the highly competitive cloud infrastructure market against Amazon’s AMZN cloud arm Amazon Web Services and Microsoft’s MSFT Azure.

Alphabet’s growing investments in infrastructure, security, data management, analytics and AI are expected to drive Google Cloud revenues in the long run. Its strengthening Gen AI-backed cloud offerings are expected to drive Google Cloud’s momentum among cloud customers.

Google Workspace is seeing rapid adoption. Alphabet saw growth in Google Workspace in the third quarter, driven by an increase in average revenue per seat.

GOOGL Shares Trade at a Premium

Alphabet’s Value Score of C suggests a stretched valuation at the moment.

Currently, GOOGL is trading at a premium, with a forward 12-month Price/Sales of 6.43X compared with the industry’s 6.02X.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

Here’s Why GOOGL Shares Are a Buy Post Q3 Earnings

Alphabet’s growing Cloud business and expanding GenAI capabilities present a potential catalyst for future growth. Its dominant position in the search engine market is a strong growth driver.

Despite a stretched valuation and stiff competition in the cloud space, these factors are expected to drive GOOGL shares higher.

Alphabet currently has a Zacks Rank #2 (Buy), which implies investors should start accumulating the stock right now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

It’s only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it’s positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Snap Inc. (SNAP) : Free Stock Analysis Report