If you are wondering how all those data centers will be powered, look no further than Bloom Energy (NYSE:). It holds the key to unlocking the bottleneck limiting datacenter expansion today: power supply.

Hyperscalers unable to connect to the power grid are turning to Bloom Energy because its fuel cells are easy to deploy and require no connection to traditional infrastructure. They are inherently co-locatable, scale to size, and are easy to operate, providing steady, reliable power as needed.

The recent announcement by Oracle (NYSE:) underscores the company’s position. Oracle is the fastest-growing hyperscaler, planning to more than double its footprint in the near term and then continue growing, and it is leaning hard into Bloom Energy technology. Details include up to 2.8GW of power supply, sufficient to cover about half of Oracle’s planned expansion. The likely outcome is that Oracle and others continue to lean into this technology in future quarters.

Bloom Electrifies Market With Stunning Report

Bloom Energy investors were expecting a solid Q1 report, but got blown away by the reality. The company reported more than $752 million in net revenue, up 130% year-over-year, and approximately 3,900 basis points (bps) better than expected. The strength was driven by product sales, up more than 200%, and is expected to continue in the upcoming quarters. The guidance was equally impressive, with the full-year revenue expected to be $3.6 billion at the mid-point, 1250 bps above the consensus forecast.

Margin news was also electrifying, with gross and operating margins improving due to sales leverage. Adjusted earnings increased by a quadruple-digit amount and outperformed the top line by an accelerated 23,800 bps, compared to the 3,900 bps in top-line growth. Other critical details include a positive inflection in GAAP operating income and cash flow, and the impact they had on shareholder value.

The balance sheet reflects the strength of Bloom’s business trends. Q1 highlights include increases in cash, current, and total assets, only partially offset by increases in liabilities. Within liabilities, recourse debt fell, improving leverage to about 2.82X the equity, and the equity increased. Equity increased by nearly 20% and is on track to continue increasing in fiscal 2026. There is some risk of dilution, as share sales in 2025 helped lift the cash balance, but the risk diminishes with each quarter. With demand surging and cash flow improving, the likely scenario is that Bloom’s financial condition will also improve.

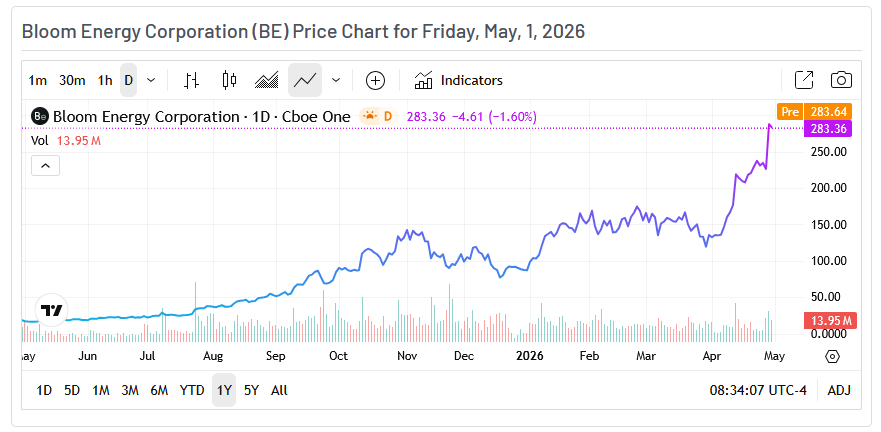

Bloom Energy Has Market Support But Overextended in April

Analysts are responding favorably. The news triggered more than half a dozen price target increases, with the bulk leading to above-consensus levels and the high end of the range. The only bad news is that BE’s market is still well above the consensus and set up for a correction. The possible outcome is that BE’s stock price reverts to the consensus level, near $195 as of late April, where it confirms support before rebounding. The $195 level coincides with a critical support target and is likely to trigger buying when touched, assuming no change in the fundamental story.

Institutional trends are mixed, suggesting volatility in this market. The group owns a substantial 77% of the stock and has an outsized influence on the price action. They accumulated in late 2025, setting the stage for the 2026 price surge, but reverted to profit-taking in early 2026. If this trend continues in Q2, the odds of a major correction increase.

Set Up for Consolidation, But Correction Is Possible

The chart price action reflects a potential correction. The stock price surged 27% in one day following the Q1 release, gapping up at the open and then continuing higher through to the close. The subsequent candle formed an Outside Day or Bearish Engulfing Pattern, a sign that this uptrend may be ending. The caveat is that Outside Days occur frequently and are not a definitive signal; reduced trading volume suggests this one is simple profit-taking rather than a major market top.

Bloom Energy’s biggest risk is its valuation. The stock trades at approximately 135X its 2026 earnings midpoint, pricing in a very robust growth trajectory. The valuation comes down over time, but not sufficiently to present value unless you consider the potential for consensus figures to be light. As it stands, analysts forecast significant slowing in the coming years and a revenue contraction before the decade’s end, a scenario not yet reflected in the results. The likely outcome is that BE’s forward outlook blossoms over time, helping support the uptrend in stock prices.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.