One of the best ways to gain insight into the investment strategies of top-tier financiers is to delve into their 13F filings. These documents, mandated by the distinguished Securities and Exchange Commission (SEC), lay bare the trading activities of major institutional investors.

Recently, I delved into the 13F of Third Point, a hedge fund launched by billionaire investor Dan Loeb. Judging by his recent acquisitions, it’s clear that Loeb is placing a bullish bet on artificial intelligence (AI). However, what caught my eye were the specific companies he’s been adding to his portfolio.

Up until now, the artificial intelligence narrative has revolved around tech giants like Microsoft and Nvidia. Despite this, Loeb has made substantial moves by investing in two other members of the “Magnificent Seven,” recently acquiring 900,000 shares of Amazon (NASDAQ: AMZN) and 3 million shares of Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL).

I find these investment decisions quite compelling. Let’s delve into why Amazon and Alphabet are quietly asserting themselves as frontrunners in the AI sector and why now might be an opportune time to consider these stocks.

Amazon: The Trailblazing Cash-Flow Titan

Amazon has carved a reputation primarily as a dominant force in e-commerce and the cloud computing sector through Amazon Web Services (AWS).

Over time, Amazon has stealthily ventured into various growth avenues such as streaming services, advertising, grocery delivery, and more. This diversification has presented Amazon with a unique opportunity.

The crux of the matter is that Amazon can seamlessly integrate AI-driven services into its ecosystem, thereby expanding its consumer outreach and facilitating cross-selling opportunities.

One of Amazon’s crucial recent moves was a substantial $4 billion investment in an AI startup named Anthropic. The objective was to catalyze growth within AWS, leveraging AWS as the primary cloud provider and harnessing Amazon’s infrastructure to train its generative AI models.

This move carries significance as Anthropic serves as a source of lead generation for AWS, fueling transactions for new products like Amazon Bedrock. Another strategic maneuver by Amazon involves hefty investments in data centers, with the company having earmarked $11 billion to construct new data facilities in Indiana.

Presently, Nvidia holds sway over the AI semiconductor market. Nonetheless, Amazon is charting its own path by developing a line of chips termed Trainium and Inferentia. The venture into data center construction is designed to enhance Amazon’s chip autonomy in the long haul and reduce reliance on third-party providers for its AI ambitions.

Image source: Getty Images.

Although we are merely in the nascent stages of the AI revolution, Amazon has generated a staggering $50 billion in free cash flow over the past 12 months, indicative of burgeoning growth across all its business segments.

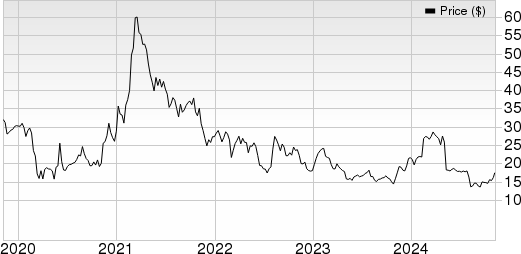

I foresee a rosy future for AWS in particular. As AI becomes more deeply entrenched across Amazon’s spectrum, the ongoing investments bear a mark of astuteness and indicate promising long-term returns. Amazon’s price-to-sales (P/S) ratio stands at 3.3, mirroring its 10-year average.

This suggests that many investors may be overlooking Amazon’s AI prowess and underestimating the potential uptick the company could witness in the future. In my view, the stock is undervalued, and I am in alignment with Loeb’s move to scoop up shares.

Alphabet: The Ascendant Cloud Luminary

Alphabet serves as the parent entity of Google and YouTube. Given the widespread influence of both platforms on the internet, it comes as no surprise that Alphabet’s primary revenue stream stems from advertising.

While Alphabet boasts leadership in online advertising, it faces considerable competition from various tech behemoths. Nonetheless, the company has embarked on a calculation that is likely to redefine its future.

Alphabet’s Data Advantage Holds the Key to Future Growth Despite Cyclical Market Trends

Alphabet’s Strategic Data Advantage Amid a Cyclical Advertising Industry

Despite the cyclical and often unpredictable nature of the advertising industry, tech giant Alphabet, parent company of Google, is paving its path to continued growth through a strategic advantage – data. Alphabet’s treasure trove of consumer search trends is a goldmine that fuels its large language model, Gemini, giving the company a powerful tool for innovation and product development.

Google Cloud Platform and the Rise of Alphabet

Google Cloud Platform, a segment within Alphabet, is emerging as a significant player in the cloud computing sector. Rapidly becoming the fastest growing business under the Alphabet umbrella, Google Cloud Platform is already showing promising signs of generating substantial operating profits. This growth trajectory positions Alphabet favorably for long-term success in the evolving tech landscape.

Alphabet’s Pursuit of AI Dominance and Market Potential

Alphabet’s ambitions in the realm of artificial intelligence (AI) are not to be underestimated. As the company diversifies its AI offerings across various sectors including workplace productivity tools, cloud computing, e-commerce, and consumer search, it is on track to establish a comprehensive and lucrative AI business. With a keen eye on the future, Alphabet is strategically positioning itself to harness the potential of AI and drive further growth.

Investment Outlook and Market Valuation

Trading at a price-to-earnings (P/E) ratio of 27.3, Alphabet’s stock appears attractively valued compared to its industry peers. The company’s robust data capabilities, coupled with its strategic focus on AI innovation, make it a compelling investment opportunity for long-term investors seeking market-beating returns in the tech sector.

The Motley Fool’s Investment Insights

While the investment landscape may seem daunting, experts at The Motley Fool emphasize the importance of thorough research and strategic decision-making. As industry dynamics evolve and market trends fluctuate, staying informed and assessing investment opportunities with a discerning eye is crucial for long-term financial success.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.