When diving into the realm of Chinese e-commerce, the competition is fierce. Alibaba and PDD Holdings stand out as two key players vying for dominance in this lucrative market. A thorough analysis using TipRanks’ Comparison Tool reveals intriguing insights, shedding light on which of these giants may hold the edge.

Comparing Business Models

Alibaba, a juggernaut with a global footprint, boasts a diverse portfolio of platforms such as Tmall and Taobao, catering to both Chinese and international consumers. On the other hand, PDD is renowned for its Pinduoduo discount e-commerce platform and its international expansion through Temu.

Financial Performance Snapshot

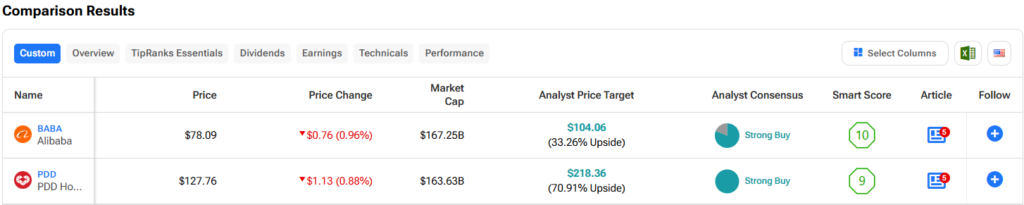

Alibaba’s stock has seen a 5% rise year-to-date but a troubling 18% decline over the last year. Meanwhile, PDD’s shares have experienced a 12% dip in 2024 but have surged by an impressive 43% over the past 12 months.

Despite their divergent stock trajectories, the valuation gap between Alibaba and PDD remains narrow. Comparing their price-to-earnings (P/E) ratios offers valuable insights into their relative valuations within the industry context.

While most players in the Chinese e-commerce sector struggle with profitability, Alibaba and PDD emerge as outliers. Examining their price-to-sales (P/S) ratios against the industry backdrop reveals interesting dynamics, with the Chinese e-commerce sector trading at a P/S ratio of 1.2x, slightly below the three-year average of 1.4x.

Alibaba (NYSE:BABA): An In-depth Analysis

With a P/E ratio of 18.4x and a P/S ratio of 1.3x, Alibaba presents an intriguing investment opportunity, particularly given its anticipated earnings growth reflected in a forward P/E of 8.8x. These metrics hint at an undervalued stock with significant potential upside.

Often dubbed the Amazon of China, Alibaba’s transformation from a growth stock to a more mature player parallels Amazon’s trajectory. Significant growth prospects lie ahead, with Alibaba’s Cloud segment poised for double-digit revenue increases following strategic enhancements.

Although Alibaba’s recent revenue growth of 8% year-over-year marked a departure from its high-growth origins, the company’s cloud initiatives and market positioning offer a glimpse of a possible resurgence in growth trajectory.

Investors may find Alibaba’s current stock price attractive, trading within historical P/E ranges and primed for potential valuation expansion. While challenges loom, including a notable drop in net income, Alibaba’s growth potential in China’s booming market remains a compelling narrative.

The Future Outlook for BABA Stock

Analysts’ consensus on Alibaba points to a Strong Buy rating based on recent assessments, with an enticing average price target forecasting a 33.5% upside potential from the current levels.

PDD Holdings (NASDAQ:PDD): An Insightful Evaluation

PDD finds itself in a similar valuation range as Alibaba, with a P/E of 17x indicating relative alignment. However, the elevated P/S ratio of 4.4x hints at potential overvaluation, underscoring the differences in market perception between Alibaba and PDD.

Despite the robust 90% revenue growth recorded by PDD in 2023, concerns loom over its regulatory risks, particularly surrounding its Temu platform focused on North America. Scrutiny from U.S. authorities on Chinese tech firms, including PDD, poses challenges that warrant investor attention.

Transparency concerns also arise, notably around PDD’s reporting of Temu’s financial performance and compliance issues, raising the stakes for investors assessing the company.

In conclusion, the Chinese e-commerce landscape showcases a dynamic interplay between industry giants Alibaba and PDD, each offering distinct opportunities and risks for investors navigating this thriving market.

Bullish Signals for PDD Stock Forecast Amidst Industry Challenges

Amidst industry challenges, PDD Holdings embarks on a mission to enhance its compliance program, signaling a commitment to navigating regulatory complexities. While the specifics of this endeavor remain shrouded in mystery, the company’s proactive stance resonates positively with investors.

The Path to Prosperity: PDD Stock Price Target

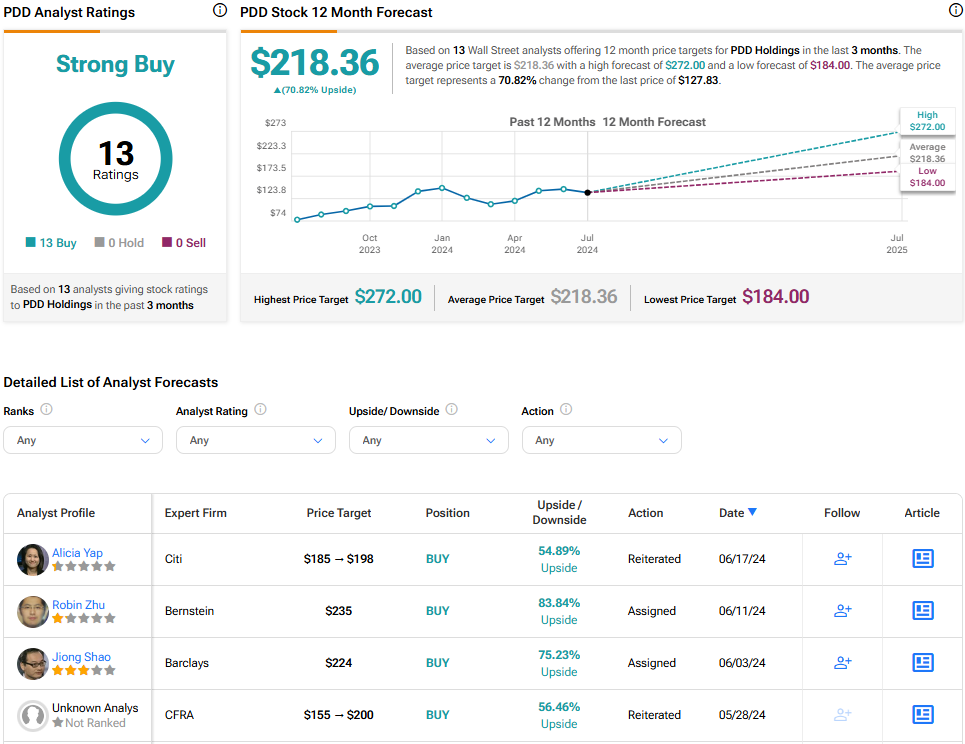

PDD Holdings boasts a Strong Buy consensus rating, garnering 13 Buys and no Holds or Sells in the past three months. With an indicative price target of $218.36, the average forecast reveals a promising upside potential of 70.8%. This optimistic outlook paves the way for a buoyant future for PDD stock investors.

Discover more insights on PDD analyst ratings here.

The Verdict: Alibaba and PDD Holdings on the Radar

In the arena of investment opportunities, both Alibaba and PDD Holdings exhibit alluring prospects in the long run. Although both companies face headwinds arising from concerns about Chinese consumer spending, these challenges appear transient. Consequently, seizing the current downturn in these stocks might prove to be a strategic move.

Notably, both entities face the shared vulnerability of being Chinese stocks listed on U.S. exchanges, susceptible to potential delisting. Yet, PDD bears a greater burden of risk, given the looming specter of impending U.S. legislation mandating a segregation from TikTok or the outright prohibition of its operations within the United States. Hence, in light of this terrain fraught with uncertainty, Alibaba emerges as the wiser choice, its status as a resilient cornerstone of the Chinese e-commerce sector rendering it a safer harbor for investment.

Acknowledging these nuanced dynamics, investors are prompted to tread cautiously, balancing the allure of potential returns with the prudence of risk mitigation strategies.