Shares of moved higher in Thursday’s after-hours session following its fiscal Q2 earnings report, setting the stock up for a potential move back towards last December’s highs. Apple has delivered strong quarters before, but this one lands differently.

Not because it was wildly unexpected; Apple, after all, has one of the better track records out there for beating expectations. However, this report reinforced a growing sense that the stock has a ton of room to run. At around $270, Apple is still trading well below where many analysts believe it should be, and this latest report helps explain exactly what’s been holding the stock back and why that may be about to change.

A Record Quarter That Reinforces the Bull Case

Right off the bat, there was a lot to like in Apple’s report. The company beat expectations on both revenue and earnings, while delivering what it described as its best March quarter ever. That kind of performance, at Apple’s scale, is not easy to achieve and speaks to the strength of its underlying business.

Its iPhone segment once again did much of the heavy lifting, with revenue holding up well despite a challenging macro backdrop. At the same time, Services continued to shine, hitting another all-time high and reinforcing its role as one of the most important drivers of Apple’s long-term growth.

This is the key point. Apple isn’t relying on single-product cycles or one-off tailwinds, as it has at times in the past. Like , it’s now generating consistent growth across multiple areas of its ecosystem, and doing so with a level of predictability that few companies can match. All things considered, this was a textbook Apple quarter, further strengthening the argument that the company remains one of the highest-quality businesses in the market.

Management Is Signaling Confidence Loud and Clear

For any investors still unsure if this is a stock worth getting involved in, there were reasons to be impressed beyond the results alone. For example, Apple’s management announced a fresh $100 billion share buyback, while also boosting its dividend, continuing a long-standing track record of returning capital to shareholders.

While these kinds of updates aren’t exactly new, the scale and consistency of the moves are what matter. They reflect a level of confidence in the company’s cash flow generation and future outlook from the management that is difficult to ignore. And given that before the report, the stock was trading at the same levels it was last October, you get a sense of how undervalued it could be.

Strong Guidance Adds to the Momentum

Looking ahead, Apple’s guidance provided another reason for optimism. Not only did the company report solid growth last quarter, but it’s also expecting solid revenue growth in the coming quarters, with projections comfortably ahead of what many investors had been anticipating.

Overall, demand remains healthy, the ecosystem continues to perform, and there’s no immediate sign of a slowdown that would derail the story. At the same time, additional tailwinds are starting to take shape that are also working in Apple’s favor. Excitement around new product cycles and broader leadership developments, not least the well-received news that John Ternus is replacing Tim Cook as CEO, are helping to support sentiment, adding another layer of potential upside to the stock.

Apple has reminded investors exactly why it deserves to command such a premium. It combines scale, profitability, and consistency in a way that few others can match. Put it all together, and the outlook becomes quite rosy. Apple isn’t just delivering strong results; it’s setting itself up for what could be a bumper year.

The Upside Potential Is Real

In terms of how good it could get, there’s a sense that recent price action left upside on the table. Sure, the stock had gained around 6% in the month before earnings, but it’s important to remember that that return lagged the over the same period. Maybe it was a case of investors waiting to see how this report landed before they went all-in, but don’t be surprised if the stock moves quickly into catch-up mode.

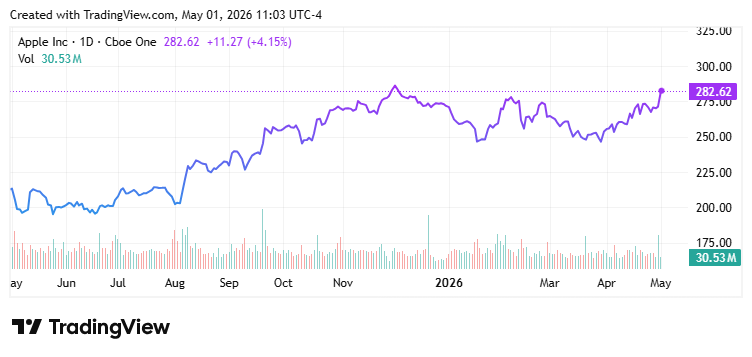

Price Chart")

This is supported by the fact that the broader market is in full risk-on mode, with the S&P 500 posting its best April since 2020. And given that the likes of Wedbush have recently set a $350 price target for Apple, a return to $300 in the coming weeks should be quite achievable.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.