Alibaba (BABA) has taken a toll over the past year, witnessing a 7.2% decline in its stock price. This downturn stands in stark contrast to the impressive growth of 22.5%, 19.6%, and 26.1% in the Zacks Internet-Commerce industry, the broader retail sector, and the S&P 500 index, respectively. With uncertainty looming, investors are grappling with the decision of whether to retain their positions or let go of their shares in the Chinese e-commerce giant.

The dip in Alibaba’s stock price comes amidst a backdrop of market volatility and economic headwinds in China. The diminishing export volumes in the country are proving to be a significant drag on the performance of China’s e-commerce companies.

Investors are faced with a balancing act – weighing Alibaba’s growth trajectory against the challenges it faces. Factors such as sluggish consumer spending, escalating operational costs, and the substantial capital investments required to stay competitive in the e-commerce and cloud markets are essential considerations.

Examining One-Year Price Performance

Image Source: Zacks Investment Research

However, Alibaba’s resilient international commerce arm shines through the gloom. The company’s strategic investments and utilization of Artificial Intelligence (AI) for product innovation provide a ray of hope. Its expanding footprint in the thriving cloud computing sector serves as an additional catalyst.

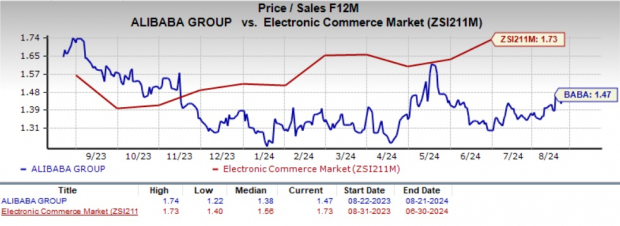

Notably, Alibaba boasts an attractive valuation, trading at a discount with a forward 12-month P/S of 1.47X compared to the industry average of 1.73X.

Image Source: Zacks Investment Research

Unpacking the Strength of Alibaba’s International Commerce Business

The Alibaba International Digital Commerce Group (AIDC) business, encompassing Lazada, AliExpress, Trendyol, Alibaba.com, and other ventures in the global retail and wholesale landscape, remains pivotal in driving the company’s growth.

In the first quarter of fiscal 2025, the AIDC segment raked in RMB 29.29 billion ($4.03 billion) in revenues, marking a robust 32% growth from the comparable period and contributing 12% to the total revenues.

The growth in international commerce retail revenues to RMB 23.7 billion ($3.3 billion) represented a 38% surge year-over-year, while international commerce wholesale revenues of RMB 5.6 billion ($771 million) grew by 12% on an annual basis.

Alibaba’s retail business benefits from the upsurge in AliExpress’ Choice and its enhanced monetization efforts. The company has expanded its supplier base on the AliExpress platform, broadening its product offerings to meet diverse consumer demands seamlessly.

Furthermore, collaborations with entities like Magazine Luiza in Brazil underscore Alibaba’s commitment to enhancing its global footprint. Strategic investments in platforms like Trendyol aim to bolster market presence in select regions.

Alibaba’s focus on delivering tailored user experiences worldwide, coupled with its adept use of AI and cutting-edge technologies, positions the company for sustained growth. The surge in SMEs leveraging Alibaba’s AI services and the success of Alibaba Guaranteed bode well for its future.

The Zacks Consensus Estimate for fiscal 2025 anticipates revenues of $139.8 billion, reflecting a 7.1% upsurge year-over-year.

Headwinds in the Face of Macro Challenges and Rising Expenses

Macroeconomic headwinds, notably high interest rates and inflationary pressures, pose substantial challenges for Alibaba.

Weakening market conditions and declining export volumes in China are exerting pressure on Alibaba’s domestic retail operations.

Geopolitical tensions between the United States and China add another layer of uncertainty. Though not directly related to the e-commerce realm, the ripple effects of this tech-cold war cast shadows on the prospects of Alibaba and its peers.

Furthermore, the escalating expenses are encroaching on Alibaba’s margin expansion. In the first quarter of fiscal 2025, sales, marketing, administrative, and product development costs inflated by 180 basis points (bps), 240 bps, and 100 bps, respectively, year-over-year.

Consequently, the operating income witnessed a 15% decline from the previous year, with the operating margin contracting by 300 bps.

Alibaba’s robust investments and cost pressures aimed at preserving competitiveness are expected to keep margins under strain, thereby impacting its bottom line adversely.

The Zacks Consensus Estimate for fiscal 2025 projects earnings of $8.20 per share, signaling a 4.9% drop from the previous year with no revisions in the past month.

Image Source: Zacks Investment Research

The Shadow of Competition Looms Large

Despite holding sway in the Chinese e-commerce domain, Alibaba faces stiff competition on the global stage, notably from giants like Amazon (AMZN) and eBay (EBAY).

Their foray into the global cloud market is riddled with challenges as they encounter formidable competition from major players such as Amazon, Microsoft, and Alphabet’s Google (GOOGL).

Final Thoughts on Alibaba’s Prospects

Considering the uncertainties surrounding Alibaba, coupled with escalating expenses, margin erosion, and intensifying competition in the e-commerce and cloud sectors, parting ways with BABA shares seems judicious at this juncture.

It is noteworthy that Alibaba currently bears a Zacks Rank #4 (Sell).

You can see…

Unearthing Hidden Champions in the Stock Market

The world of finance is akin to an intricate dance, with investors treading carefully to find the perfect rhythm that leads them to profit. Amidst the ebb and flow of the markets, whispers of upcoming gems often go unnoticed, much like hidden treasure awaiting discovery by a keen eye.

Discover 5 Stocks Poised for Meteoric Growth

Enter the arena of stocks set to double – each meticulously selected by experts at Zacks, who forecast a remarkable surge of over 100% by the year 2024. While not every prediction can be a winner, historical data showcases previous recommendations reaching heights of +143.0%, +175.9%, +498.3%, and a staggering +673.0%.

These stocks bask in the shadows away from the mainstream Wall Street spotlight, offering intrepid investors a chance to delve into untapped potential at its inception.

Today, See These 5 Potential Home Runs >>

Curious about the latest investment insights from Zacks Investment Research? Not to worry, a potpourri of information awaits you with the “7 Best Stocks for the Next 30 Days,” available for download today.

Click here to access this free report!

Revealing Untapped Potential in Prominent Stocks

For seasoned investors, well-known stocks stand as pillars of familiarity in the volatile realm of finance. Companies like Amazon.com, Inc., eBay Inc., Alphabet Inc., and Alibaba Group Holding Limited have etched their names in the annals of stock market history.

Uncover a treasure trove of free stock analysis and delve deeper into these market giants to make informed investment decisions.

Free Stock Analysis Report for Amazon.com, Inc. (AMZN)

Free Stock Analysis Report for eBay Inc. (EBAY)

Free Stock Analysis Report for Alphabet Inc. (GOOGL)

Free Stock Analysis Report for Alibaba Group Holding Limited (BABA)

Delve deeper into the realm of stock analysis and make informed decisions that could shape your financial future.

To uncover further insights on Alibaba Group Holding Limited’s performance over the past year, click below.

For more intriguing opportunities and expert analysis, explore the realm of Zacks Investment Research.