The wind is shifting around AI—and we’re getting set to ride the next wave with dividends up to 12.3%.

Today we’re going to discuss what I see as the “intersection” between AI’s growth and the 8%+ income streams we’re drawing from the portfolio of our CEF Insider service.

Then we’re going to spotlight three CEFs in the sweet spot: They’re profiting indirectly from AI’s growth, while giving us exposure to sectors beyond tech.

Here’s why I see that as a strong move now.

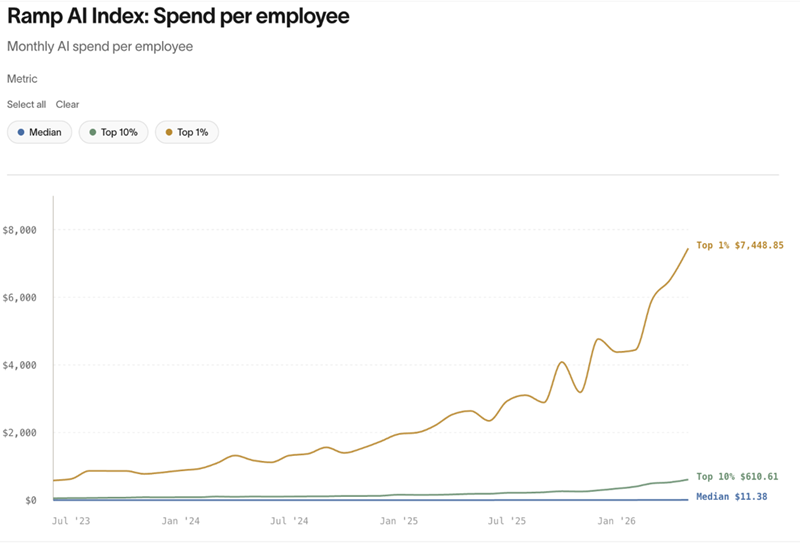

On the one hand, AI is helping companies find new efficiencies. And I know I don’t have to tell you that tech is driving big investments across the economy. But even though it feels like companies are spending to the limit on AI, they have plenty of room to spend more. Look at this:

Source: Ramp.com

In the chart above, we see that the top 1% of firms spending on AI are indeed putting a lot into the tech: around 10% of what they pay their average employee per year. But look at the blue line at the bottom: The median AI spend per employee is $11.38. So yes, there’s a lot of room for that number to grow, and it will over time.

Here’s the catch, though: As I write this, the index is on the pricey side, trading at a trailing-12-month price-to-earnings (P/E) ratio of 25, according to The Wall Street Journal.

Where does that leave us? With a market that still has plenty of long-term upside, but likely more choppiness as we move through the back half of 2026.

Before I go further, let me be clear on one thing: I see any pullback as a buying opportunity, in light of the long-run growth AI is likely to deliver. While we wait for that, it’s time to put money to work in other corners of the market. Which brings me back to those three “sweet spot” CEFs I mentioned off the top. Let’s get into them now.

A Top Bond Fund Yielding 7.7% (Trading for 89 Cents on the Dollar)

One of the strengths of our diversified CEF Insider portfolio is that it lets us pivot to where the mainstream crowd is likely to go when the market’s mood changes. One place mainstream investors will look if they feel stocks are getting risky? Bonds. And funds like the PIMCO Dynamic Income Strategy Fund (NYSE:).

Let’s start with PDX’s 7.7% yield, which means we’re getting a considerable amount of our upfront investment back every year in the form of payouts.

And that dividend is steady: After cutting it in the wake of the 2022 interest-rate spike, management has kept it steady as rates fell and leveled off. They even dropped a big special dividend at the end of last year, plus a smaller one the year before that. Those went a long way toward making up for the earlier reduction in the regular payout:

Source: Income Calendar

This is the kind of “dividend control” we want to see from management. And even though rates may tick higher in the next few months, we’re nowhere close to the situation we saw in ’22. And on the other side, of course, we have the deflationary effects of AI.

It’s no surprise, then, that PDX, with a portfolio of corporate bonds and asset-backed securities, has seen a strong total return in its net asset value (NAV, or the value of its underlying portfolio—shown in purple below) so far this year.

More important, PDX’s market price–based return (a more sentiment-driven measure, shown in orange) has risen to meet that NAV gain.

PDX Gains—Inside and Out

These are both bullish signs. Yet PDX still trades at a 10.6% discount to NAV, meaning we’re basically paying 89 cents on the dollar for its assets.

That’s despite the fact that this fund is run by California-based PIMCO, which has a legendary reputation among CEF investors. As such, the company’s funds tend to trade at premiums—often big ones.

That’s another reason why I don’t see PDX’s discount lasting long, especially as more investors go looking for alternatives to AI stocks in the short run, and for higher income as rates move lower in the longer term.

An AI-Exposed REIT Fund Yielding 12.3%

Let’s move on to REIT funds, which have gained this year, in part because investors are finally starting to come around to the fact that REITs, too, benefit from the AI boom.

That’s set up a nice entry point on the Neuberger Berman Real Estate Securities Income Fund (NYSE:), a “one-stop shop” for real estate exposure. The fund’s biggest holdings are REITs operating in areas that are hard for competitors to gain a meaningful foothold in.

Senior-care REIT Welltower (NYSE:) is the top holding, followed by Prologis (NYSE:), the biggest warehouse REIT, and data-center giant Equinix (NASDAQ:). Cell-tower landlord American Tower (NYSE:) clocks in at No. 4.

Let’s get right to the dividend, because NRO’s 12.3% yield is nothing if not eye-catching. But that payout is steady. It even saw a hike early last year:

Source: Income Calendar

What’s more, the payout looks safe, due in large part to the performance of NRO’s NAV, as well as the market price’s discount to that NAV, over the past year:

NRO’s NAV Has Covered Its 2026 Payout

Going by NRO’s 12.7% total NAV return (in purple above) in the past year, we can see that that run has cleared the fund’s 12.3% current yield. That’s one reason why its payout looks sustainable.

Then there’s the discount to NAV, currently at 8.4%. That makes NRO’s payouts safer because when you calculate the yield based on NAV, not the discounted market price, you get an even lower bar for management to clear: 11.3%.

Finally, you can see in the orange line above (NRO’s market-price movements in the last year) that investors have been underbidding the fund’s strong NAV performance. Buying today lets us get in now—and enjoy price gains as they correct that mistake.

An Unloved 6.7% Dividend Set to Grow

Finally, there’s the John Hancock Financial Opportunities Fund (NYSE:), with a 6.6% yield, a 3.1% discount to NAV and a focus on regional banks. For starters, the fund’s relatively low yield makes the payout both sustainable and set to grow, building on a payout history of doing just that:

Source: Income Calendar

Meantime, we can buy BTO at a 3.6% discount—which is rare for a fund that usually commands a premium:

BTO Is Cheaper Than It’s Been in Years …

BTO tended to trade at a premium because it’s a reliable way to access regional banks. Old National Bancorp (NASDAQ:), Popular (NASDAQ:) and Citizens Financial Group (NYSE:) are top positions, and all have helped BTO see strong gains over the long haul.

… Despite a Stellar Performance

Such a track record deserves a premium, and BTO is highly likely to command one again—even though I do expect the fund’s discount to widen slightly before that happens. The fund trades right around my buy-up-to-price of $39 now. I recommend snagging more shares on any moves below that level.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.