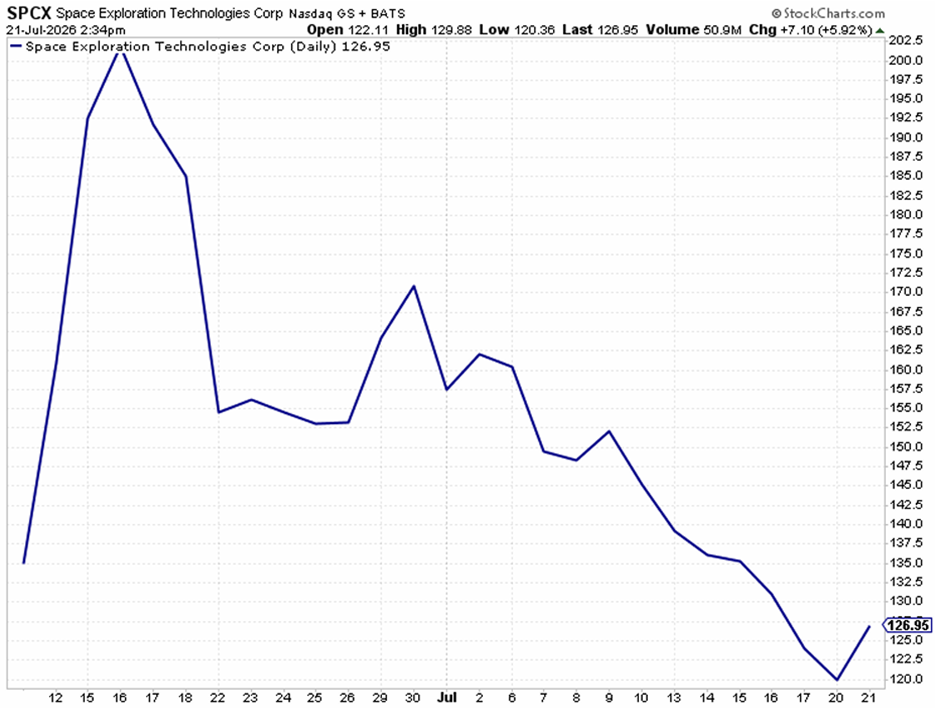

As of last Friday, after five full trading days, Space Exploration Technologies () began to trade inside the range of its first trading day. To recap, the stock opened at $150 on its IPO day (IPO at $135), rising to $225.64 by mid-week (last week), before trading all the way down to $172.11 last Friday.

I don’t know how many G’s it takes to blast off Earth and go into orbit, or come back to Earth, but if there is a clear equivalent of a space round trip in stock trading, the first week’s action in SPCX resembles it.

If anyone could become successful in building cities on the Moon and Mars, Elon Musk and SpaceX would be the ones to make it happen. They are light-years (pun intended) ahead of the competition. But stocks with huge $2.4 trillion market caps (as of the close on Friday) don’t typically trade like yo-yos.

The reason for this erratic price action is that no more than 4.3% of the shares are available for trading.

As per Google’s Gemini, the detailed tiered lock-up expiration schedule is as follows:

- August 11, 2026 (Post-Q2 Earnings): Up to 20% of eligible locked shares become free to trade.

- August 25 – October 25, 2026: Rolling tranches of 7% unlock at predetermined intervals (70, 90, 105, 120, and 135 days post-IPO).

- November 9, 2026 (Post-Q3 Earnings): The largest single tranche unlocks, freeing an additional 28% of eligible shares.

- December 9, 2026: The 180-day cliff expires, unlocking all remaining eligible Class A shares.

- June 2027: Elon Musk and certain significant core insiders are subject to a longer 366-day lockup, holding their shares in restriction for the first full year. (Note: An additional 10% bonus tranche could unlock earlier if SPCX trades 30% above its IPO price for a minimum of 5 out of 10 days post-earnings).

Until August 11, when more shares become available for trading, the present price is not real. If you get a lot of people chasing 4.3% of the float of a giant company, the stock will go up. If those people decide to sell, it will go down quite a bit. We have witnessed both events in the last few trading days. I am sure Elon Musk has all kinds of tricks up his sleeve for when more stock gets released from lock-ups, like multiple satellite and Starship launches, but this is a very different situation than Musk’s Tesla ().

Tesla went public with $1.7 billion in market cap, while SpaceX is coming in at $1.75 trillion at the time of the IPO. Tesla now has a market cap of $1.5 trillion, as the company grew well after the IPO. I am sure SpaceX will grow, too, but it won’t be linear. I expect we’ll see many fits and starts. I think the next time we hit turbulence in the stock market, or one of its rockets explodes (which happens occasionally), SpaceX may break below its $135 IPO price. This should come between now and the end of the year, perhaps during the next stock market correction, but given the overpriced IPO level, it could happen a lot sooner.

The New Warsh-Led Fed Could Play a Role in Space-X (and Market) Gyrations

If the Iran war does not reignite, it may very well turn out that the new Fed Chair, Kevin Warsh, will be the culprit for the next big swing in the stock market. Jerome Powell became Fed Chairman on February 5, 2018, and in the fourth quarter of 2018, he helped fuel a near-20% drop in the because of his quantitative over-tightening. Kevin Warsh has not done anything yet – other than announce multiple task forces to review the way the Fed conducts policy, and a rather shortened , like a breath of fresh air, given the convoluted language of previous FOMC statements, even predating Powell.

I like the fact that the vote was 12-0, and I like the firm tone of the conclusion – namely, the “will deliver price stability.” Some rate-hiking odds shot up in the futures markets, but it is way too early to speculate on whether or not the Fed will hike rates, which the recently did in reaction to the price of crude oil and fertilizer, which were acutely affected by the closure of the Strait of Hormuz.

Kevin Warsh wants to shrink the Fed’s (charted below) and lower the Fed funds rate due to the view that a bigger balance sheet helps more financial market prices while a lower Fed funds rate helps the real economy more. This will take time. He has not gotten the FOMC to do any big market operations regarding those views, and his task forces will take some time to produce the necessary recommendations.

I can’t imagine the Fed instituting any new revival of crazy QE or QT operations before the mid-term elections in November, but stranger things have happened. I think the referral in the FOMC statement to maintaining ample reserves in the banking system is to calm down worries stemming from the fact that any time reserves in the banking system tend to shrink, the stock market tends to dive, and the volatility in the bond market tends to increase. This is what happened to Jerome Powell’s Fed in late 2018.

If the new Fed Chair messes around with the balance sheet, I think both stocks and bonds will notice. In the meantime, we’ll keep our fingers crossed that the ceasefire will hold and the global economy will develop according to the time-limited disruption scenario from OECD (above), because the other option is that many countries in Europe and Asia without domestic energy resources may go into recession.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.