A good way to help develop your investment prowess is by looking at the actions of acclaimed money managers. Sounds easy, but how exactly can you do that?

Well, luckily, the Securities and Exchange Commission requires institutional investors managing over $100 million to file a form 13F once per quarter. You can think of a 13F as an itemized receipt, breaking down each trade Wall Street’s brightest minds conducted during the quarter.

One investor I enjoy following is Ken Griffin, the billionaire co-founder of the Citadel investment firm. According to its current 13F, Citadel has been steadily reducing its position in Microsoft (NASDAQ: MSFT) while adding shares in chip manufacturing powerhouse Taiwan Semiconductor Manufacturing (NYSE: TSM).

Below, I’ll break down what could be influencing these decisions and whether I agree with Griffin’s calls.

Why sell Microsoft right now?

Microsoft was one of the first companies to really jump-start the artificial intelligence (AI) boom, underscored by a $10 billion investment in ChatGPT developer OpenAI. This move allowed the company to swiftly integrate a host of AI-powered services throughout its ecosystem — like the workplace Office suite, Azure cloud computing infrastructure, social media platform LinkedIn, and more.

Microsoft has undoubtedly emerged at the forefront of the AI marathon, but there are legitimate questions surrounding the company’s leading position. You see, the deal with OpenAI inherently raised the stakes for others in big tech.

In particular, its primary competitors in the cloud computing space, Amazon and Alphabet, followed up the deal with OpenAI by each investing in a competing start-up, Anthropic. On top of that, enterprise software company Salesforce recently announced that it’s launching a competing service to Microsoft’s Copilot AI.

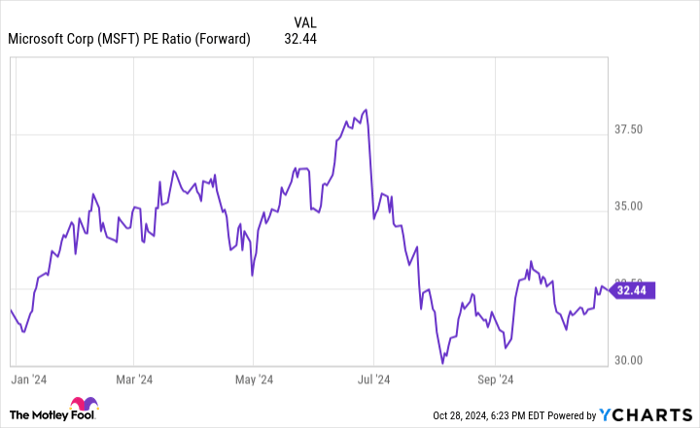

There has been some contraction in the stock’s valuation in recent months, but the company’s forward price-to-earnings multiple (P/E) of 32.4 is still pretty pricey. To add some context, the average forward P/E of the S&P 500 is only 22.7.

MSFT PE ratio (forward), data by YCharts.

Below, investors can see that Citadel has been steadily trimming its position in Microsoft for the last few quarters.

- Q2 2023: 3.4 million shares

- Q3 2023: 5 million

- Q4 2023: 4.2 million

- Q1 2024: 2.9 million

- Q2 2024: 1.2 million

To me, Microsoft remains a compelling opportunity in the AI landscape, but at the same time, I am wary about how the company really stacks up against the competition. I think it’s just too early to say with any certainty one way or the other.

For these reasons, I think Citadel’s decision to take profits in Microsoft while keeping some limited exposure is a savvy call right now amid the current competitive landscape and frothy valuation.

Why buy Taiwan Semiconductor right now?

As I’ve said before, I think Taiwan Semiconductor (or TSMC) is the most compelling long-run opportunity in the chip realm. While Nvidia gets most of the attention in the semiconductor space, the company can credit TSMC for a lot of its success.

TSMC manufactures chips for Nvidia. And a deeper dig into the company indicates that it also manufactures products for Advanced Micro Devices, Amazon Web Services, Broadcom, Qualcomm, and Sony, among others.

Chips are going to be a major source of this investment, which bodes well for TSMC. Its diverse customer roster and unique expertise in the semiconductor arena also help make the case that the company’s services should remain in demand for quite some time.

Image Source: Getty Images

The bottom line

Picking which cloud computing platform or AI agent will emerge as the most successful in the long run is nearly impossible at this stage. By contrast, it’s reasonable to suggest that big tech is going to continue spending heavily on AI infrastructure for the foreseeable future.

The way I look at it is that investing in Microsoft requires a high conviction that the company will outpace Amazon, Alphabet, Salesforce, and others in competing markets. In other words, there’s a degree of specificity with Microsoft that can’t really be measured or accurately forecast right now.

On the other hand, an investment in TSMC is one that is rooted in a broader theme fueling the AI narrative, namely steady demand for chips. For these reasons, I think swapping Microsoft stock for Taiwan Semiconductor makes a lot of sense at the moment.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $20,993!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,736!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,720!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Microsoft, Nvidia, Qualcomm, Salesforce, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.