J.B. Hunt Transport Services, Inc. JBHT has rallied sharply, putting investors in a familiar spot. The stock has momentum, but that does not automatically make it cheap.

The better question is whether earnings power, improving freight conditions and estimate revisions can support the premium investors are now paying. For JBHT, the answer is constructive, but not without valuation discipline.

Why JBHT’s Earnings Setup Looks Better

JBHT’s latest earnings backdrop gives bulls something concrete to work with. Second-quarter 2026 earnings rose 45.8% year over year to $1.91 per share and topped the Zacks Consensus Estimate by 11.7%.

Revenue increased 19.4% to $3.50 billion and beat the consensus mark by 9.5%. The setup also looks better beyond one quarter, with 2026 earnings expected at $7.56 per share and 2027 earnings expected at $9.88 per share.

The trucking company has an impressive earnings surprise record, having outpaced the Zacks Consensus Estimate in each of the past four quarters. The average beat is 9.8%.

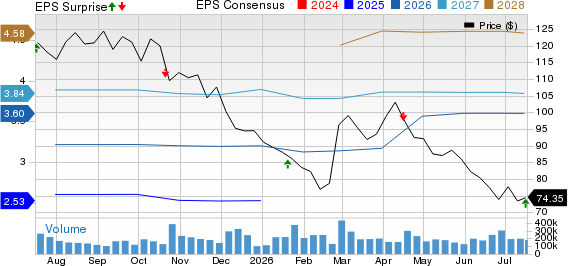

J.B. Hunt Transport Services Price and EPS Surprise

J.B. Hunt Transport Services price-eps-surprise | J.B. Hunt Transport Services Quote

The estimate trend is moving in the right direction as well. The forward earnings estimate has risen 3.7% over the past four weeks, a positive signal after a freight downturn that pressured pricing and margins.

Why J.B. Hunt’s Valuation Invites Debate

The pushback is valuation. JBHT trades around 36 times forward 12-month earnings, above the Zacks sub-industry, sector and S&P 500 comparisons.

That leaves less room for disappointment. The stock has already gained 53.6% year to date, and its trailing 12-month move reflects investors’ growing confidence in a freight recovery.

Schneider National SNDR also gives investors exposure to truckload, intermodal and logistics markets. Hub Group HUBG, with its intermodal and supply-chain focus, offers another comparison point for investors watching road-to-rail conversion trends.

How JBHT Supports the Bull Case

The premium is not without support. Intermodal volume increased 10% in the second quarter, including 16% growth in the eastern network, as higher fuel costs and constrained highway capacity strengthened the road-to-rail value proposition.

Segment operating income rose 58%, helped by better network efficiency, productivity gains, fewer empty container moves and lower storage expense. These are the kinds of operating improvements that can matter if freight demand continues to recover.

JBHT also strengthened its balance sheet. Debt declined to about $1.15 billion at June 30, 2026, from $1.72 billion a year earlier.

Capital returns remain part of the story. The company raised its quarterly dividend to 45 cents per share in January 2026, marking its 22nd consecutive annual dividend increase, and had about $791 million left under its share repurchase authorization at June 30.

What Keeps J.B. Hunt From Looking Cheap

The caution case starts with liquidity. Cash and cash equivalents were only about $4.2 million at June 30, 2026, far below outstanding debt.

Purchased transportation costs also remain a drag. Integrated Capacity Solutions saw purchased transportation expense rise 54% in the second quarter, while Truckload posted an operating loss as higher third-party capacity costs pressured gross profit.

Driver needs are another constraint. Management has cited rising driver demand as freight improves and customer wins increase, which could add cost pressure or slow onboarding if labor availability tightens further.

How JBHT’s Ratings Shape the Decision

The bottom line is that JBHT looks fundamentally better, but not inexpensive. Earnings growth, estimate revisions and intermodal momentum support the rally, while the valuation asks investors to pay up for continued execution.

JBHT currently carries a Zacks Rank #1 (Strong Buy). That rank points to a favorable near-term earnings-estimate backdrop, which fits the improving profit setup. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Style Scores add nuance. JBHT has a Momentum Score of A and Growth Score of B, supporting the view that price action and earnings prospects remain constructive. Its Value Score of D, however, reinforces the main risk: the business may be improving faster than before, but the stock is already priced for a good portion of that recovery.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

J.B. Hunt Transport Services, Inc. (JBHT) : Free Stock Analysis Report

Hub Group, Inc. (HUBG) : Free Stock Analysis Report

Schneider National, Inc. (SNDR) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.