Well, after being away for just over a week, I am officially back. I’m sure everyone missed me.

Magically, not much has changed since we last touched base. Even after falling by around 0.8% on Monday, the is still roughly where it was on July 2.

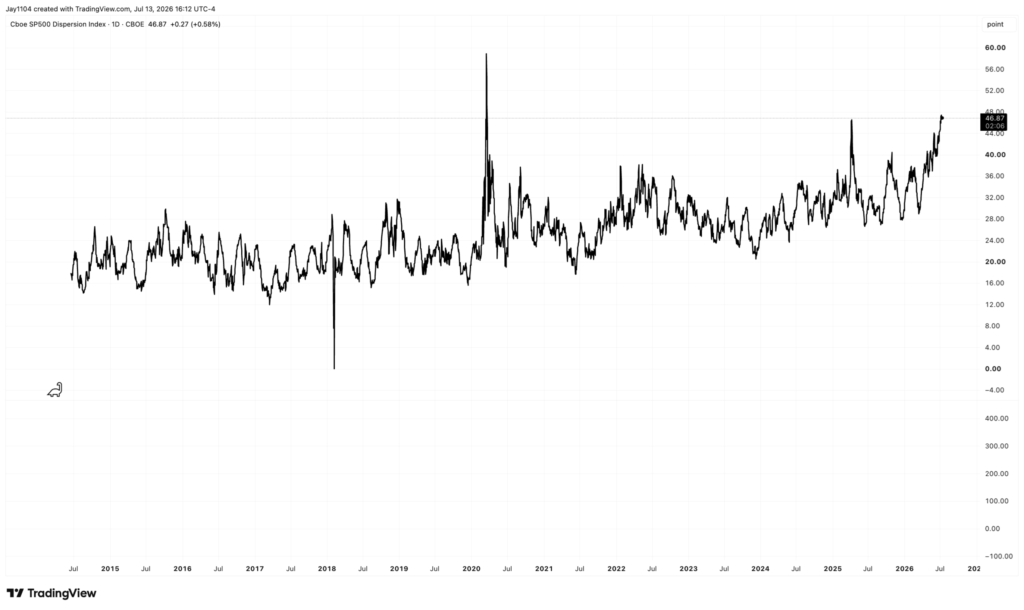

However, dispersion remains high, implied correlations remain low, and the market is still out of balance when comparing single-stock volatility with index-level volatility. As far as I can tell, the only time the dispersion index has been higher was in 2020. That means it is now even higher than it was during the April 2025 tariff tantrum.

This is being driven by the wide wedge that still exists between single-stock and index-level implied volatility. The spread between VIXEQ and the remains near the highs reached just days ago and is still well above 30.

What is particularly interesting is that, of the 142 S&P 500 stocks I track in my sector breakdowns, 52% have implied volatility near their 52-week highs, while none are near their lows.

Typically, when implied volatility is this elevated across so many stocks, the S&P 500 is falling—not rising. That suggests IV is not necessarily increasing because the market fears individual stocks or views them as particularly risky. Instead, the market’s behavior appears consistent with a gamma-squeeze-like feedback loop.

In essence, VXSMH is at 64 not necessarily because the market is deeply concerned about semiconductor stocks or because investors are putting on massive hedges. Rather, realized volatility in is already at 62.4. The large price movements in the underlying stocks are helping to drive implied volatility higher, creating dispersion and distortions across the market.

Semiconductor stocks appear to be caught in a gamma squeeze, much like Micron (NASDAQ:) was. With these stocks moving 3% to 4% a day, realized volatility will remain high, and implied volatility will likely remain elevated as a result.

The problem is that stocks do not move 3% to 4% every day forever. Eventually, realized volatility will begin to fall, likely pulling implied volatility lower with it. Call positioning heavily outweighs put positioning in many of these names, including Micron. As IV falls and call premiums decay, the associated delta exposure may also begin to unwind.

Ultimately, this trade will end. How it ends—and what that unwind looks like—are the real questions. If it has been driven largely by options-related mania, there is a meaningful risk that the ending will not be orderly.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.