Intel Corporation INTC and Silicon Motion Technology Corporation SIMO are two premier semiconductor firms focusing on AI (artificial intelligence), advanced chip technologies and the data center semiconductor ecosystem. Intel is currently focusing on AI chips for data centers and PCs, which marks one of the largest architectural shifts for the company in 40 years. The decision is primarily aimed at gaining a firmer footing in the expansive AI sector, spanning cloud and enterprise servers to networks, volume clients and ubiquitous edge environments, in tune with the evolving market dynamics. The foundry operating model is a key component of the company’s strategy and is designed to reshape operational dynamics and drive greater transparency, accountability and focus on costs and efficiency.

Silicon Motion is a leading developer of microcontroller ICs for NAND flash storage devices. The semiconductor company also designs, develops and markets high-performance, low-power semiconductor solutions for original equipment manufacturers (OEMs) and other customers.

Let us try to analyze some of the competitive strengths and weaknesses of the companies to understand who is in a better position to maximize gains from the emerging market trends.

The Case for Intel

Intel is witnessing healthy traction in AI PCs that have taken the market by storm. The company has launched Intel Core Ultra series 3 processor (code-named Panther Lake) in January this year and Xeon 6+ (code-named Clearwater Forest) in June. Manufactured in a new, state-of-the-art factory in Chandler, AZ, both products are built on Intel 18A, the most advanced semiconductor process in the United States. Panther Lake is designed to power a broad spectrum of consumer and commercial AI PCs, gaming devices and edge solutions. Clearwater Forest is an E-core server processor that enables business enterprises to scale workloads, reduce energy costs and power more intelligent services.

Intel’s innovative AI solutions are set to benefit the broader semiconductor ecosystem by driving down costs, improving performance and fostering an open, scalable AI environment. It has secured a $5 billion investment from NVIDIA Corporation NVDA to jointly develop cutting-edge solutions that are likely to play an integral role in the evolution of the AI infrastructure ecosystem. Leveraging the core strengths of both firms, namely NVIDIA’s AI and accelerated computing and Intel’s CPU technologies and x86 ecosystem, the collaboration is expected to sow the seeds of innovation through the development of state-of-the-art custom data center and PC products.

In August 2025, Softbank invested $2 billion in Intel to propel AI research and development initiatives that support digital transformation, cloud computing and next-generation infrastructure. The investment enabled Softbank to gain about 2% ownership in Intel, with the former paying $23 per share. This followed $7.86 billion in direct funding from the U.S. Department of Commerce under the U.S. CHIPS and Science Act to advance critical semiconductor manufacturing and advanced packaging projects in Arizona, New Mexico, Ohio and Oregon. The significant capital infusions have enabled Intel to expand its manufacturing capacity to accelerate its IDM 2.0 (Integrated Device Manufacturing) strategy.

However, Intel derives a significant part of its revenues from China. As Washington tightens restrictions on high-tech exports to China, Beijing has intensified its push for self-sufficiency in critical industries. This shift poses a dual challenge for Intel, as it faces potential market restrictions and increased competition from domestic chipmakers. The company is also lagging behind in the GPU and AI front compared to peers, such as NVIDIA and Advanced Micro Devices, Inc. AMD. Leading technology companies are reportedly piling up NVIDIA’s GPUs to build clusters of computers for their AI work, leading to exponential revenue growth.

The Case for SIMO

Silicon Motion has established itself as the leading merchant supplier of client SSD (solid state drive) controllers to module makers, including most market leaders in the United States, Taiwan and China. The company believes that it is well-equipped to adapt to industry changes as it has collaborated with flash vendors for developing proprietary controller technology to overcome the existing weakness of 3D NAND and outshine peers. Silicon Motion has commenced initial sales of 3D SSD controllers to flash partners. It expects this controller to be a significant SSD controller growth driver for the next year, as NAND Flash partners’ 3D capacity expands.

Silicon Motion operates a fabless business model, focusing on chip design while outsourcing manufacturing to foundries like TSMC. Consequently, the company has a low capital investment requirement as it does not require expensive fabrication plants, enabling it to adopt advanced manufacturing nodes quickly, leading to higher margins compared to integrated manufacturers. This, in turn, enables the company to focus on innovation and product development rather than manufacturing complexity. The key growth drivers for SIMO include AI and high-performance computing, cloud data centers, automotive storage, smartphones and mobile devices. Each of these end markets is growing fast and offers lucrative growth potential. Over the past 10 years, the company has shipped more than 5 billion controllers cumulatively – more than any other company in the world. Silicon Motion ships more than 750 million NAND controllers on average every year.

However, sluggishness in the global economy is likely to weigh on the company’s wireless and broader semiconductor market. The demand for PCs and smartphones in the end market continues to be soft as numerous suppliers are focusing on reducing their inventory levels. The near-term price fluctuation in the PC market remains a concern. Silicon Motion continues to acquire a large number of companies. While this improves revenue opportunities, business mix and profitability, it adds to integration risks. Moreover, the semiconductor industry is highly dynamic as it is prone to swift technological changes, stiff competition from evolving industry standards and declining average selling prices.

How Do Zacks Estimates Compare for INTC & SIMO?

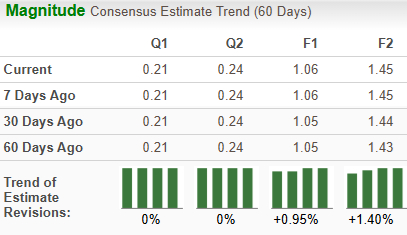

The Zacks Consensus Estimate for Intel’s 2026 sales implies year-over-year growth of 9.9%, while that for EPS indicates a surge of 152.4%. The EPS estimates have trended up 0.9% over the past 60 days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Silicon Motion’s 2026 sales indicates a year-over-year rise of 77.7%, while that for EPS suggests growth of 149.9%. The EPS estimates have trended up 1.5% over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of INTC & SIMO

Over the past year, Intel has surged a stellar 371% compared with the industry’s growth of 30.3%. Silicon Motion has gained 294.7% over the same period.

Image Source: Zacks Investment Research

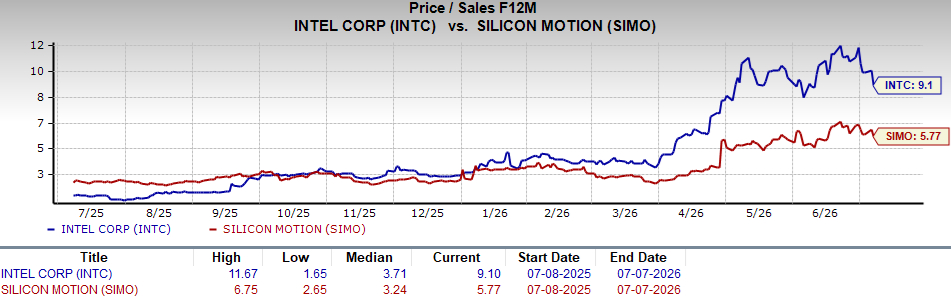

Silicon Motion looks more attractive than Intel from a valuation standpoint. Going by the price/sales ratio, Intel’s shares currently trade at 9.1 forward sales, higher than 5.77 for Silicon Motion.

Image Source: Zacks Investment Research

INTC or SIMO: Which is a Better Pick?

Both Intel and Silicon Motion currently sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Both companies expect their revenues and earnings to improve. In terms of price performance, Intel has outperformed Silicon Motion. However, SIMO is trading cheaply compared to INTC. With a similar Zacks rank, solid fundamentals and healthy growth potential, there is very little to choose between the two firms. Nonetheless, Silicon Motion’s cheaper valuation metrics make it a better investment option at the moment.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

Intel Corporation (INTC) : Free Stock Analysis Report

Silicon Motion Technology Corporation (SIMO) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.