Strategy’s (NASDAQ:) survival depend on liquidity coverage, while MSTR’s premium likely depends on reclaiming the company’s cost basis. The bear market can end for BTC before it ends for MSTR

Strategy, in the broad sense, is a company built to provide leveraged exposure to Bitcoin. It raises dollar capital through a mix of common equity, converible debt, and prefererd securities, then uses those proceeds to accquire Bitcoin. The model works extremely well when Bitcoin is rising and MSTR trades at a meaningful premium to its underlying Bitcoin net asset value. It becomes more difficult when Bitcoin enters a bear market, the common-stock premium compresses, and the fixed obligations attached to the captial stack keep accruing.

That is the context for the company’s new Digital Cedit Capital Framework. It marks a more explicit shift from accmulation-only thinking toward active balance-sheet management. The framework has five main pieces.

- First, Strategy now has a board-approved USD Reserve policy that sets a 12-month minimum reserve against preferred dividends and debt interest, with board approval required to go below that level.

- Second, the company revised the dividend policy for STRC, its variable-rate preferred security, raising the rate to 12.00%. While the company stated objective is to for STRC to trade over time in a range of appromixately $99 to $100, it also stated clearly the company will not necessarily increase the STRC dividend rate solely because STRC trades below that range.

- Third, it authorized up to $1.0 billion of repurchases for preferred securities, with STRC as the priority.

- Fourth, it authorized up to $1.0 billion of common-stock repurchases.

- Fifth, it authorized up to $1.25 billion of Bitcoin monetization to fund or replenish the USD Reserve.

Bitcoin monetization is the most important change. Strategy’s earlier investor narrative was built around accumulating Bitcoin and avoiding sales. The new policy allows management to sell Bitcoin deliberately when doing so protects the broader capital structure.

The first visible use of the framework came quickly. On July 6, Strategy disclosed that it had sold 3,588 Bitcoin for about $216 million between June 29 and July 5. The proceeds were used to pay preferred dividends and rebuild the cash reserve.

For a company whose brand has been built around Bitcoin accumulation, the pivot itself naturally created concern. The actual sale, however, was small relative to Bitcoin’s daily trading volume of around $200 to $300 billion, and the market absorbed it without much visible impact on BTC price.

We would therefore view this less as the beginning of a disorderly unwind and more as a constructive first step toward active balance-sheet management.

Does Strategy Have Runway for the Rest of the Winter?

June was brutal for Strategy. Bitcoin slid toward $58K, MSTR common briefly dropped below $82, and STRC, the preferred Strategy tries to hold near $100, de-pegged below $75.

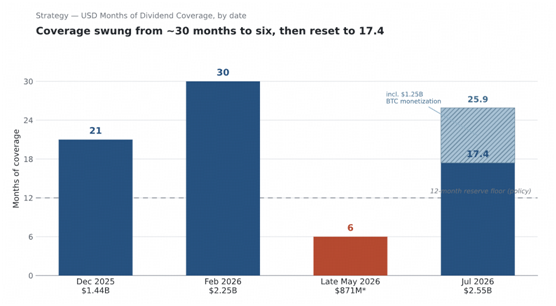

The fear is, in a large part, due to the USD Months of Dividend Coverage, the dollar reserve divided by the monthly bill for preferred shares dividends. It changed quite dramatically in recent months, from 21.0 months and a $1.44B reserve on December 1, 2025, to roughly 30 months and $2.25B by February 1, 2026, then to about only 5.9 months near a $871M reserve by late May.

As of early July, 2026, the reserve stands at $2.55B against $1.763B in annual obligations, the Months of Dividend coverage go back to 17.4 months of cash-only coverage. Add the $1.25B of authorized Bitcoin monetization and committed liquidity reaches roughly $3.8B, or 25.9 months.

Runway matters against the length of the current Bitcoin winter. The last three Bitcoin bear markets cluster tightly: about 14 months and –85% in 2013–2015, about 12 months and –84% in 2017–2018, and 12 months and –77% in 2021–2022. The current cycle peaked near $126K in October 2025 and trades around $63K as of July 7, 2026, a drawdown near 50%, roughly 9 months in.

If this cycle rhymes with those three, the bottom lands three-to-five months out, in Q4 2026. Our base case is a low in the low-$50Ks, around Bitcoin’s realized price, the aggregate on-chain cost basis of every coin, and the zone prior cycles have bottomed in. That level sits well below Strategy’s $75,476 average purchase price, so the bottom leaves the company deep underwater on its Bitcoin.

So, on the narrow dividend coverage metric, Strategy appears to have enough runway for a historically normal remaining crypto winter. A 3–5 month remaining bear market is comfortably covered.

Reclaiming Cost Basis in 1H 2027 Revives the MSTR Premium

Bitcoin’s bottom is not MSTR’s bottom. At a low in the low-$50Ks, Strategy is deeply underwater on Bitcoin bought at around $75K. The stock’s low tends to form later than Bitcoin’s, as the market needs evidence that the recovery is durable enough, thus restoring the MSTR premium, stablize STRC, and reopen the capital-raising flywheel.

For that to turn, Bitcoin has to climb back above Strategy’s $75.5K average cost. Below it, every Bitcoin sale to fund dividends prints a loss, STRC stays sensitive to coverage headlines, and common shares issued near 1x mNAV would be much less attractive for shareholders because it provides limited accretion to BTC per share. Above it, Strategy is in profit on its stack and MSTR premium could start to become more meaningful again. That matters because Strategy’s historic engine depends on issuing common share at a premium, buying more Bitcoin, and increasing BTC per share. A sustained move above cost basis would help restart that mechanism.

Reclaiming $75.5K takes about +37% from $55K, +45% from $52K, or +51% from $50K. The prior two bottoms cleared moves of that size in roughly 60–69 days (November 2022), and 108 days (December 2018), which puts a first reclaim of cost basis between late Q4 2026 and Q2 2027, the first half of 2027.

The takeaway is that Strategy’s survival depend on liquidity coverage, while MSTR’s premium likely depends on Bitcoin reclaiming the company’s cost basis. The bear market can end for BTC before it ends for MSTR. For the stock to bottom decisively, investors likely need to see Bitcoin back above Strategy’s average purchase price and finding a durable floor.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.