It’s July, which means we’re in the heart of dance competition season. As a result, I’ll once again be traveling with my family to another obscure location for Nationals. While I’m incredibly proud of everything my daughter has accomplished, I’ve also come to appreciate that competitive dance may be one of the better money-making businesses around.

With that annual family tradition underway, there will be no free evening market commentaries until I return on Monday, July 13.

Paid members should continue to receive updates during that time, though the timing may vary based on our travel schedule and performance times.

Markets return to a full week of trading after the long holiday weekend. It will be a quiet week from a news standpoint, with the Fed minutes the biggest item on the calendar. The minutes will give the market a firsthand look at the June led by Kevin Warsh. Based on the press conference he gave and the follow-up session at the ECB forum, my guess is they will come across as hawkish, because, at least for now, he is sending the message that he will be tough on inflation — and the jobs report gives him cover to do so, even though the number came in surprisingly low.

While the headline number missed estimates, I don’t think that portion of the report was a disaster, and it certainly didn’t create a sense of urgency to change direction at this point.

The fell sharply on Thursday as semiconductor stocks were hit, but futures traded higher on Friday as South Korea’s rebounded. Tonight, the KOSPI reopens, so we will see how the semis trade, which will ultimately set the tone for Monday’s session in the US. The and the KOSPI have traded in lockstep since April 2025, and I wouldn’t expect that relationship to change at this point.

Remember, SK Hynix will list in the US on July 10, and the listing is expected to be worth $29 billion. So it is possible that there could be some reshuffling in semis this week.

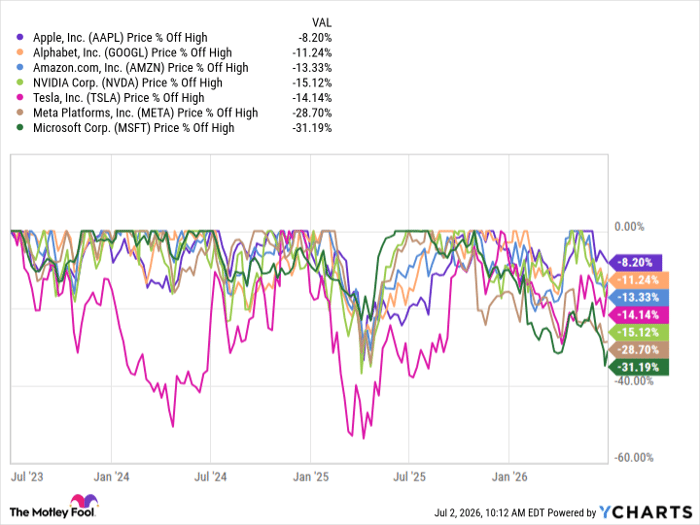

Which leaves the market in an interesting spot, as its makeup appears to have shifted over the past 21 days. The technology sector is now the laggard, underperforming the by more than 7 percentage points—a significant reversal from what we saw not long ago—while health care has emerged as the leader.

Over this period, at least based on the 11 sector ETFs, realized dispersion in the S&P 500 has risen, with implied dispersion repricing higher as well. So if it feels like individual stocks are no longer moving in line with the indexes, you aren’t imagining it. Only four sectors—, , , and materials—are still closely tracking the broader market. Beyond those, the sectors begin to diverge from the index.

The point is that if technology—and semiconductors in particular—begin to struggle, it is entirely possible for the index to move lower while some of the other sectors continue to trade independently of the broader market. That could persist until the market decides everything should begin trading more in unison again. When that happens, implied and realized correlation can start to rise, but we haven’t seen that yet.

The challenge is that there isn’t much room for implied correlation to fall further. The index is sitting at 8, near its 2024 low.

So this trade is likely closer to its end than its beginning. Given how tightly it appears to be tied to the , and perhaps even the won, if these Asian markets start to become choppy, the AI trade could unwind very quickly. Again, the wild card is the SK Hynix deal and how that listing will affect the balance between the markets.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.