Earnings are strong, but the market setup is deteriorating as AI capex is pressuring free cash flow, Mag 7 leadership is no longer one-way, equity supply is rising, and midterm seasonality creates a window for a sentiment reset.

- Earnings support the index. S&P 500 profits grew about 28% in the latest reporting season, the strongest since 2021, with AI-infrastructure names supplying roughly half of that growth.

- Fundamentals remain sound, but Mag 7 leadership has reversed, AI trade has turned two-way, and more than $200 billion of new equity supply is competing for the capital pool.

- Midterm years are usually the weakest of the four-year election cycle. A pullback into the autumn would fit the historical pattern and cool elevated sentiment without breaking the earnings story.

The is supported by strong corporate earnings. Q1 2026 earnings grew roughly 28% year over year, more than double the 13% growth analysts expected at the end of the quarter, while 85% of companies beat earnings estimates and index-level net margins reached a record 14.8%.

However, investors should also keep in mind that AI capex creates a favorable near-term earnings loop. The hyperscalers spend heavily on GPUs, servers, networking, power, cooling, and data centers. That spending is revenue for semiconductor and infrastructure suppliers, so companies on the selling side can show very strong earnings. At the same time, the buyers do not expense most of the capex immediately under GAAP accounting rule; they capitalize it and depreciate it over time. That creates a “golden window” for index-level earnings: suppliers recognize revenue and profit now, while buyers recognize the cost gradually.

This is not an argument that reported earnings are low quality or that the earnings story is unsustainable. Rather, the point is that strong earnings and near-term correction risk are not mutually exclusive. When price momentum starts to weaken, the market could start to question earnings. With mega-cap leadership weakening, AI capex raising questions about future free cash flow, record level equity issuance compete for capital, and the market entering a historically weaker pre-midterm election window, the index can undergo a sentiment reset even if the earnings backdrop remains intact.

Mag 7 Leadership Reversed

The first signal is the reversal of the largest index weights. The Magnificent 7 fell about 9% from May 1 to late June, while the remaining S&P 493 names rose about 7%. This is not a risk-off move, the broader market remained resilient, but the prior leadership cohort is de-rated.

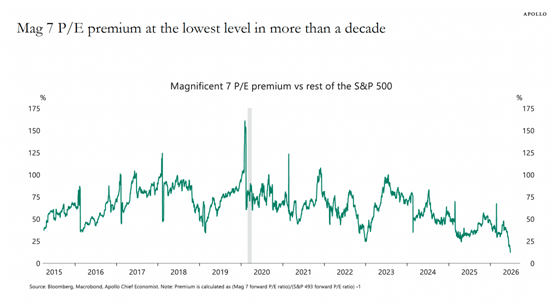

The valuation signal is equally important. The P/E premium investors pay for the group has compressed to its lowest level in more than a decade, according to Apollo’s data.

Source: Apollo

The fundamental driver of this de-rating is the deteriorating cash-flow situation. With the heavy AI-related capex spending, weaker free cash flow, investors are no longer paying the same multiples for these companies as high-margin, asset-light software/platform monopolies. The AI buildout makes parts of the group look more like capital-intensive infrastructure operators. That means a lower valuation multiple unless returns on invested capital are proven.

This also means the Mag 7 label is becoming less useful. Investors no longer treat the seven as one trade. They now separate the names that can monetize AI spending from those funding the capex cycle. Hyperscaler (, , , ) free cash flow will fall sharply this year and next, with the payoff from current capex expected only after 2028, when it could generate more than $700 billion in free cash flow for the group. However, the rapidly changing AI landscape makes projections that far out unreliable. The market will no longer pay a premium for the group without a visible path from spending to free cash flow.

Source: BCa Research

Record Equity Issuance Associated With Cycle Top

Equity supply is becoming a meaningful pressure for U.S. equities, although the risk is more subtle than the headline issuance amount suggests.

The driver is a combination of cyclical reopening and AI captial demand. After four years of muted net issuance following the 2021 boom and the Fed’s aggressive hiking cycle, companies are returning to market for both IPO and secondary offering. Alphabet announced an $80 billion equity raise to fund AI infrastructure, and completed the largest IPO on record at about $85.7 billion in proceeds. OpenAI was reported to be weighing a delay of its listing into 2027, with Anthropic’s filing pointed at the autumn.

At the market level, the number is still small in 2026 of around $200 billion estimated by JP Morgan, But will jump over 500% in 2027, these include IPOs, secondary offerings, and other share sales, as hyperscalers are expected to raise hundreds of billions in secondary share offerings to fund their AI spending plans.

The issue is not simply the aggregate dollar amount of issuance, but timing, concentration, and motive. Public investors are being asked to finance a capital-intensive AI infrastructure cycle at the same time mega-cap valuation are repriced lower. Recent history of this kind of equity supply also suggest concerning signals as historically increased deal activity associated with peak stock prices.

Midterm Years Are the Weakest of the Cycle

The calendar adds a sensonal headwind. Midterm years have historically been the weakest part of the election cycle, with the two most recent midterm years, 2022 (-18%) and 2018 (-4.4%),which were the S&P 500’s two weakest calendar years since the 2008 financial crisis.

S&P 500 Total Returns

Source: https://www.slickcharts.com/sp500/returns#google_vignette

The more important signal is not a negative yearly return, but the market path around uncertainty. Since 1970, the S&P 500 has historically showed weakness before the midterm election, but began to rally roughly 22 trading days before midterm, according to data from BlackRock. After the vote, the average six-month return was 14.1%.

Source: BlackRock

This makes midterm seasonality a timing risk. The market has typically struggled most when policy uncertainty was unresolved, then recovered once investors could better price potential regulation changes. This supports a correction-and-reset for the market into November, followed by a recovery if earnings remain intact and election uncertainty clear.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.