The Cooper Companies, Inc. COO sits at the intersection of two durable healthcare trends: premium vision care and fertility demand. Its CooperVision business benefits from contact lens upgrades, while CooperSurgical gives it exposure to IVF and women’s health.

The issue is execution. Long-term demand remains attractive, but Asia-Pacific softness, portfolio transitions, cost pressure and litigation payouts are still shaping the near-term investment case.

Why Cooper Fits Premium Lens Trends

CooperVision is aligned with the shift toward daily disposable silicone hydrogel lenses, a premium category that supports better mix and recurring demand. In the fiscal second quarter, daily silicone hydrogel lenses grew 8%, with MyDay delivering double-digit growth.

The company is also positioned in torics and multifocals, where revenue rose 7% organically to $364.9 million. MyDay Energys and multifocal products remain important as Cooper expands into new markets and upgrades wearers from legacy hydrogel products.

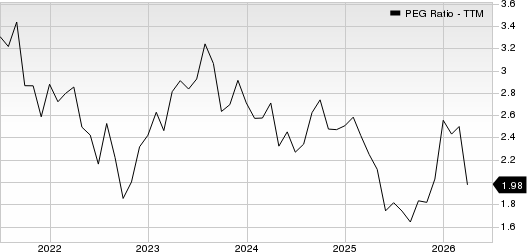

The Cooper Companies, Inc. PEG Ratio (TTM)

The Cooper Companies, Inc. peg-ratio-ttm | The Cooper Companies, Inc. Quote

Alcon ALC is a relevant peer because it also competes in premium contact lens categories. Johnson & Johnson JNJ, through Acuvue, adds further competitive intensity across eye-care practitioner channels.

How MiSight Taps a Secular Need

Childhood myopia is one of CooperVision’s clearest long-duration growth themes. MiSight gives Cooper a differentiated position in pediatric myopia control, combining recurring lens use with a clinical need that extends beyond routine vision correction.

MiSight revenue grew 24% to $32 million in the fiscal second quarter. Momentum was supported by Japan, the MyDay MiSight launch in Europe, practitioner education and consumer-awareness campaigns around the back-to-school period.

Why Fertility Keeps Cooper Diversified

CooperSurgical broadens COO beyond vision care through fertility and women’s health. The business benefits from delayed childbirth, improving IVF cycles, expanding access to care and clinic investment in technology and workflow tools.

Fertility revenues rose 10% organically to $143.8 million in the fiscal second quarter. Growth came from genomics, capital equipment and consumables, giving Cooper exposure to recurring demand as well as clinic expansion spending.

Where Trend Exposure Meets Friction

Good industry exposure has not eliminated regional pressure. Asia-Pacific revenue declined 6% organically in the fiscal second quarter, reflecting softness in Japan and China, economic pressure in Korea and the continued rationalization of legacy hydrogel products.

The private-label transition can also create timing noise, while hydrogel exits may weigh into 2027. Larger rivals in contact lenses keep competitive intensity high, especially as practitioners and retailers evaluate premium lens alternatives.

Can COO Convert Trends Into Cash

Cooper’s cash-flow profile remains a support. Management raised its fiscal 2026 free cash flow outlook to roughly $650 million, excluding litigation payouts, and reaffirmed its objective of more than $2.2 billion in free cash flow from fiscal 2026 through fiscal 2028.

5-Yr Free Cash Flow vs Price Chart

Image Source: Zacks Investment Research

Still, conversion is not clean. Tariffs, freight, foreign exchange, lower production at CooperVision and litigation payouts can blunt the near-term earnings benefit from attractive product trends.

How COO’s Rating Signals Frame the Trend Story

The bottom line is balanced. COO has credible exposure to premium lenses, myopia control and fertility, but its Zacks Rank #3 (Hold) fits a story where execution, regional recovery and margin discipline still matter as much as the long-term healthcare themes. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock’s Style Scores are more constructive, with a VGM Score of B, Value Score of B and Growth Score of B. These scores suggest a reasonable mix of valuation and growth characteristics. However, the Momentum Score of D points to weaker timing support, reinforcing the need for investors to watch Asia-Pacific trends, cash conversion and cost pressures before taking a more aggressive view.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

The Cooper Companies, Inc. (COO) : Free Stock Analysis Report

Johnson & Johnson (JNJ) : Free Stock Analysis Report

Alcon (ALC) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.