We should avoid REITs right now because the Fed talks tough about raising rates.

Or we should buy REITs right now because the Fed’s worries are overblown.

Which is true? Well, it depends.

Let’s talk about our beloved real estate investment trusts, or REITs, which we favor as retirement-focused investors. REITs must dish most of their profits to us as dividends. A congressional act created them decades ago, and it requires them to send us at least 90% of their taxable income as payouts, in exchange for tax advantages.

Now the lazy Wall Street maxim holds that REITs trade opposite interest rates. As rates rise, REITs lose their shine because there’s more competition for income. As rates fall, money pours in.

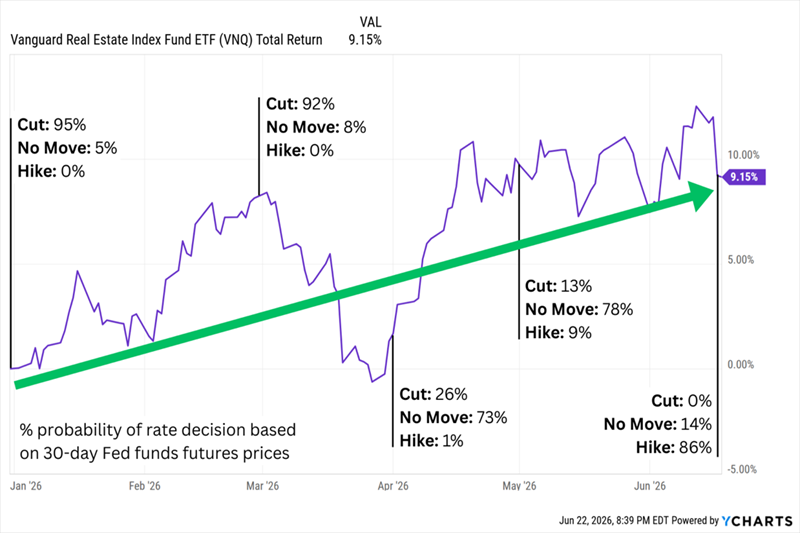

REITs Are Swimming Upstream Against Rate-Hike Expectations

Source: FedWatch

But here’s a catch for the Wall Street suits. Money pours into the REIT sector despite rising-rate fears. REITs have climbed 9% year-to-date even as the odds of a hike shot up to 86%. What’s this telling us? That new Fed Chair Warsh can set the overnight rate, but he doesn’t set the rent.

Today we see a split in the REIT sector. Some climb despite the threat of rate hikes, while others take a beating in the old sell-REITs-on-rate-worries trade. So which ones do we buy? Both. We don’t worry about what the vanilla investors do. We trust the rent checks, because these rent checks power our payouts.

CTO Realty Growth (NYSE:) (CTO, 7.3% dividend yield) is a retail REIT focused on open-air shopping centers predominantly located in fast-growing metro areas across the Southeast and Southwest.

Roughly half of its annualized base rent comes from “power centers” (outdoor malls anchored by Best Buy (NYSE:), Dick’s Sporting Goods (NYSE:), and other large-format retailers); another quarter from “lifestyle” properties anchored by restaurants, banks, and traditional retailers; and another 20% from grocery-anchored retail. The rest is split among mixed-use, single-tenant and office properties. It also generates income from managing Alpine Income Property Trust (NYSE:).

If the Fed does , it’ll likely be in response to still-high inflation and, more importantly, a healthy economy—something that clearly benefits CTO’s tenants. So it shouldn’t be surprising that the CTO is outperforming REITs this year and has picked up more momentum of late.

Despite its 2026 gains, CTO trades at a decent 10 times estimates for this year’s funds from operations (FFO). The dividend accounts for just 73% of those FFO projections, so it’s well-covered.

If Only It Weren’t So Stagnant, Too

Nexpoint Residential Trust (NYSE:) (NXRT, 7.8% dividend yield) is another southern operator, this one specializing in residential real estate. It owns 36 properties with 13,305 units in 10 markets in the Sun Belt, with a focus on Class B multifamily properties leased out to “workforce” and middle-income residents.

One of its most notable qualities is focusing on “value adds,” upgrading properties to induce higher rents. The company says it has added smart-home tech to more than 11,000 of its units, completed interior rehabs on over 10,000 of its units, and upgraded appliances in around 5,000—improvements that generate real rent premiums over time.

Unlike CTO, NexPoint has been raising its dividend for the past few years. That’s not the issue.

The problem with NXRT is a history of underperformance in both rising- and declining-rate environments.

The Fed Just Can’t Please NXRT

NXRT’s issues in 2022-23 weren’t limited to higher interest rates—operating expenses grew, and the REIT slammed against a record national multifamily supply cycle. The same supply issues weighed on the REIT in 2025 and into this year, as did a weakening job market, countering any help lower rates might have offered.

But multifamily starts are slowing, and leasing activity is showing signs of progress. That has NexPoint optimistic about 2027. I’d like to see continued strength in the job market, and a lower price than its 11x P/FFO, before getting too excited.

Global Net Lease (NYSE:) (GNL, 8.3% dividend yield) is on the high end of the yield range for traditional equity REITs. It’s a commercial net-lease operator, which means its leases are “net” of taxes, insurance and maintenance costs. GNL just collects rent checks.

Global Net Lease is somewhat insulated from the Fed because it’s a multinational operator. It owns 809 properties across the U.S. and Canada, which combine to make up roughly three-quarters of straight-line rent (SLR). The U.K., Finland and a handful of other European countries account for the rest. Its properties are diverse, too—industrial and distribution real estate makes up almost half of SLR, while retail and office split the remainder nearly evenly.

That balance likely will shift soon. GNL is trying to reduce that office exposure, and it will add to its industrial holdings with a $535 million, all-stock acquisition of Modiv Industrial announced in May.

GNL shares lost roughly half their value between 2021 and 2024. But the turnaround has been real: a $1.8 billion multitenant portfolio sale, $1.3 billion in debt shed, occupancy up from 95% to 97%, investment-grade tenants up from 60% to 64%, and G&A expenses down from $65 million to $49 million. Shares have bounced nearly 70% off the 2024 bottom.

We’re still staring down a pair of problems.

For one, GNL’s turnaround story isn’t a secret—shares now trade at a plump 15 times FFO estimates.

And Then There’s the Potential for Dividend History to Repeat

And even after all those cuts, GNL’s 19-cent quarterly dividend is currently pacing at 125% of 2026 FFO estimates and 119% of 2027’s. So it’s difficult to have much confidence that 8% yield will last at current levels.

We can find significantly higher levels of yield in the mortgage REIT (mREIT) space. But they’re not taking the Fed’s hawkish shift as well, listing lower at the same time their equity REIT cousins are on the rise.

Mortgage REITs borrow at short-term rates to buy mortgages paying long-term rates, pocketing the spread. Short-term rates are usually lower than long-term rates, and ideally, short-term rates are declining while long-term rates hold steady or also decline. In that scenario, mREITs’ existing mortgages, which were issued when rates were higher, will yield more than newly issued ones (and thus be worth more).

Rising rates, then, aren’t great for their mortgages, but certain classes of mREITs might still hold up.

ARMOUR Residential REIT (NYSE:) (ARR, 17.1% dividend yield), for instance, deals in fixed-rate agency residential mortgage-backed securities (MBSes) issued by government-sponsored enterprises such as Freddie Mac, Fannie Mae and Ginnie Mae.

Yes, rate hikes aren’t great for the worth of their mortgages either, but agency guarantees mean these MBSes have virtually no default risk. Plus, rising interest rates also lessen prepayment risks, primarily because mortgage holders are less likely to refinance.

But the lower risk profile also means lower rates, so agency mREITs use a ton of leverage to produce more income. ARR, for instance, has a debt-to-equity ratio of nearly 8. Back in April, the company delivered a slight earnings miss, and its book value declined thanks to tightening spreads. Still, Wall Street currently expects profits to cover the monthly dividend. And while shares have delivered a modest, positive total return YTD, they still trade at a small (4%) discount to Armour’s book value.

But we have to be cautious: mREITs often readjust their dividends during shifting rate environments. So if rate hikes flatten earnings, it’s an open question as to whether ARR’s dividend will remain unscathed.

And Given Armour’s Dividend History, That’s a Fair Question

Then there’s Redwood Trust (NYSE:) (RWT, 14.9% dividend yield), a deeply discounted mREIT trading at less than five times earnings estimates and 68% of book value.

Redwood is an originator of jumbo residential mortgages and single-family rental loans. In recent years, it has leaned more heavily on its Sequoia correspondent jumbo loan platform; its Aspire home equity investment options (HEI) and expanded loans platform; its CoreVest residential investment property origination platform; and its Redwood Investments portfolio of residential housing investments, which are sourced from the aforementioned platforms.

RWT shareholders have hardly been immune from rate cuts—it has made a pair of deep hacks since COVID.

However, Redwood Is Quicker to Hit the Gas When It Can

For now, dividends are well covered at 72% of 2026 earnings estimates. But this isn’t an agency mREIT, so Redwood actually faces added default risk as rates rise—a main driver of its steady stock descent since mid-April.

Disclosure: Brett Owens and Michael Foster are contrarian income investors who look for undervalued stocks/funds across the U.S. markets. Click here to learn how to profit from their strategies in the latest report, “7 Great Dividend Growth Stocks for a Secure Retirement.”

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.